{kind=link}

Here are the latest developments in global markets:

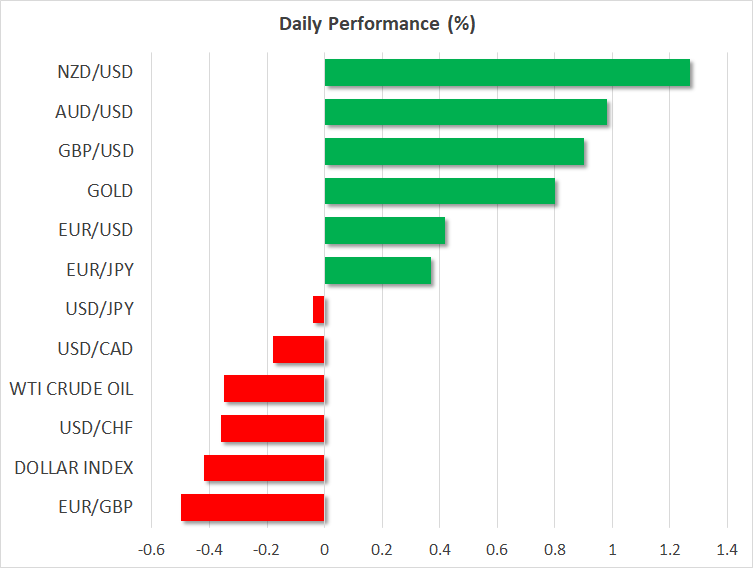

FOREX: The dollar index is down by a little more than 0.4% on Thursday, looking set to post its first daily decline in four sessions. The British pound, and to a lesser extent the euro, benefited from reports that UK financial services firms will continue to have access to EU markets after Brexit. Meanwhile, the antipodeans aussie and kiwi outperformed, likely lifted by the broader improvement in risk sentiment, as well as fresh signals that China’s leadership is considering more stimulus measures.

STOCKS: Wall Street closed higher for a second session on Wednesday, with the tech-heavy Nasdaq Composite (+2.08%) outperforming the S&P 500 (+1.09%) and Dow Jones (+0.97%). The positive sentiment failed to carry over into Asia though, which was mixed on Thursday. Japanese and South Korean indices edged lower, though Chinese and Hong Kong markets climbed, aided by news that China is planning further stimulus measures to cushion its economy. In Europe, most major indices were set to open flat today according to futures. The main exception was the UK FTSE 100, which was due to open lower amid a strengthening pound.

COMMODITIES: Oil was down on Thursday, extending the losses it recorded in the previous session. The losses followed the weekly EIA crude inventory data, which showed stockpiles rising for the sixth consecutive week, lending some credence to recent warnings by Saudi Arabia that the market may see oversupply later this year. In precious metals, dollar-denominated gold is up by an astounding 0.8% today at $1,225 per ounce, capitalizing on the correction lower in the greenback.

Major movers: Sterling soars on Brexit financial services deal; antipodeans skyrocket

The British pound surged overnight, gaining more than 0.9% versus the dollar, following reports that the UK and EU have reached an agreement that would allow UK financial services companies continued access to European markets post Brexit. The pound was already on the front foot on Wednesday, lifted by a letter from Brexit Secretary Raab to the UK Parliament, which noted he expects to finalize a deal with the EU by November 21. The optimistic headlines may have caught markets by surprise given the absence of any encouraging signals lately, leading to a rapid covering of prior short-bets on the pound.

Crucially though, there was no mention to the real sticking point, the Irish border. Until there’s news of progress on that front too, one may be forgiven from being too upbeat. In the words of PM May: “nothing is agreed until everything is agreed”. Separately, striking a deal with the EU is an entirely different beast to passing it through the UK Parliament. Hence, although Brexit optimism is currently riding high, lots of obstacles and twists likely remain before an actual deal is signed, implying that it won’t be all smooth sailing higher for the pound. Today, the currency will get its cue from the BoE rate decision, but overall, monetary policy considerations may play second fiddle to political ones until the Brexit fog has lifted.

Meanwhile, the rising sterling-tide also lifted the euro, helping euro/dollar to gain 0.4% and establish some distance from its 16-month lows at 1.1300, which it tested yesterday. Accordingly, the dollar index is on the retreat today as the euro and sterling are recovering ground, though it still remains at relatively elevated levels.

Strikingly, the antipodeans aussie and kiwi are outperforming even the pound today, having soared by 0.98% and 1.25% respectively against the dollar. The aussie got a modest lift from stronger-than-expected trade data out of Australia overnight. Overall though, the main driver behind this rebound may have been the recovery in risk appetite, as well as fresh hints yesterday from China for further stimulus, amid growing signs the economy is losing momentum.

Day ahead: Bank of England decides amid Brexit news; ISM manufacturing PMI due; Apple releases earnings

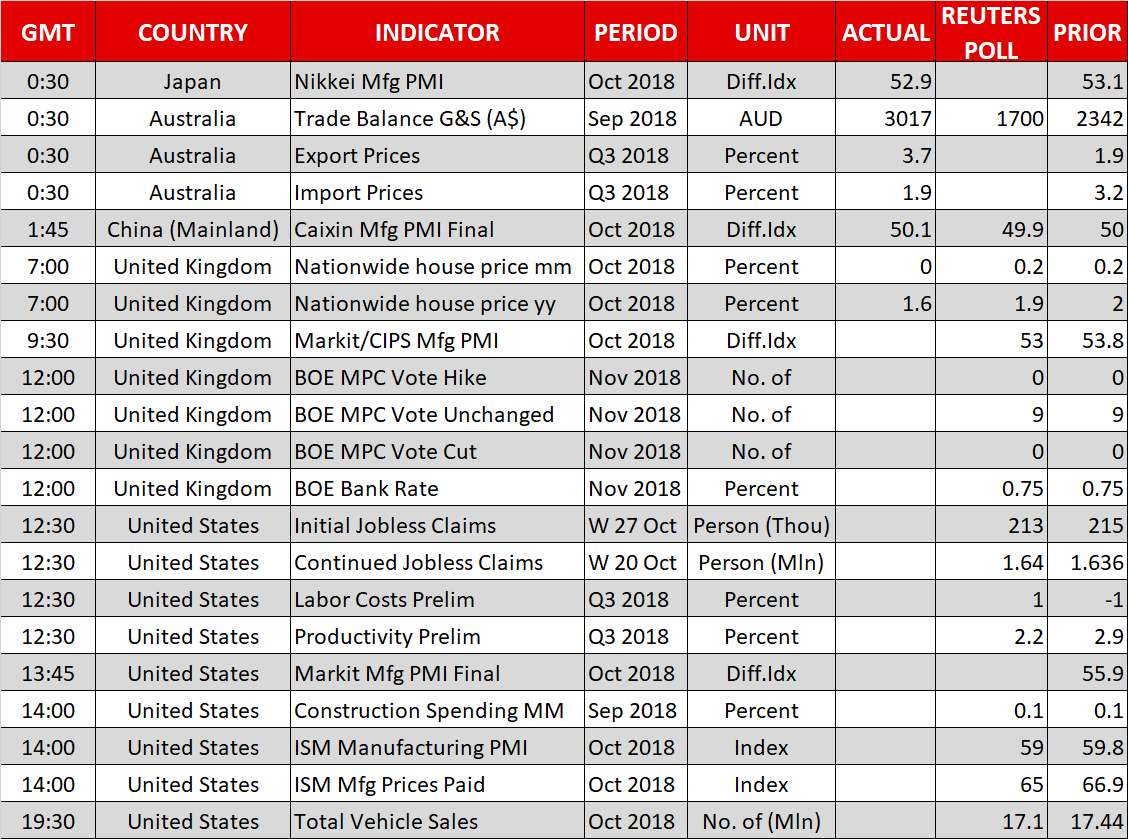

The Bank of England’s (BoE) guidance upon completion of its monetary policy meeting will be in focus during Thursday’s trading. The most important US release is the ISM’s manufacturing PMI.

At 1200 GMT, the BoE’s monetary policy decision will be made public. The Bank’s members are expected to unanimously vote in favor of keeping rates on hold. Given that no rate change is anticipated, the focus will fall on the central bank’s communication – what conditions are needed for further policy tightening (?) –, as well as on updated inflation and GDP forecasts. Governor Carney will be holding a press conference at 1230 GMT, with his comments closely watched for positioning on sterling.

Any remarks on Brexit by the Bank – by Carney himself during the press conference – will also be generating attention, especially in the aftermath of reports that PM May has arrived at a deal with Brussels that would give UK financial services companies access to EU markets after Brexit. It remains to be seen whether the British currency will maintain the positive momentum spurred by those news.

Ahead of the BoE decision, at 0930 GMT, the UK will be on the receiving end of Markit’s manufacturing PMI for October. That’s expected to ease to 53.0 from 53.8 in September.

The ISM’s manufacturing PMI for October scheduled for release at 1400 GMT is projected to fall to 59.0, from September’s 59.8. Nevertheless, this would still constitute a robust figure that is comfortably above the 50 threshold that separates sectoral expansion from contraction. Markit’s corresponding PMI print for the US will be hitting the markets a little earlier (1345 GMT).

Other US data are on the agenda as well, such as weekly jobless claims due at 1230 GMT, though these tend not to act as market movers. Total vehicle sales out at 1930 GMT are also typically not market-moving for FX markets, but they have their own interest amid the rising rate environment in the US which is generally negative for automobile sales.

Bank of Canada Senior Deputy Governor Wilkins will be giving a speech at 1700 GMT.

Apple, the world’s largest company by market cap, will be releasing quarterly results after the closing bell on Wall Street.

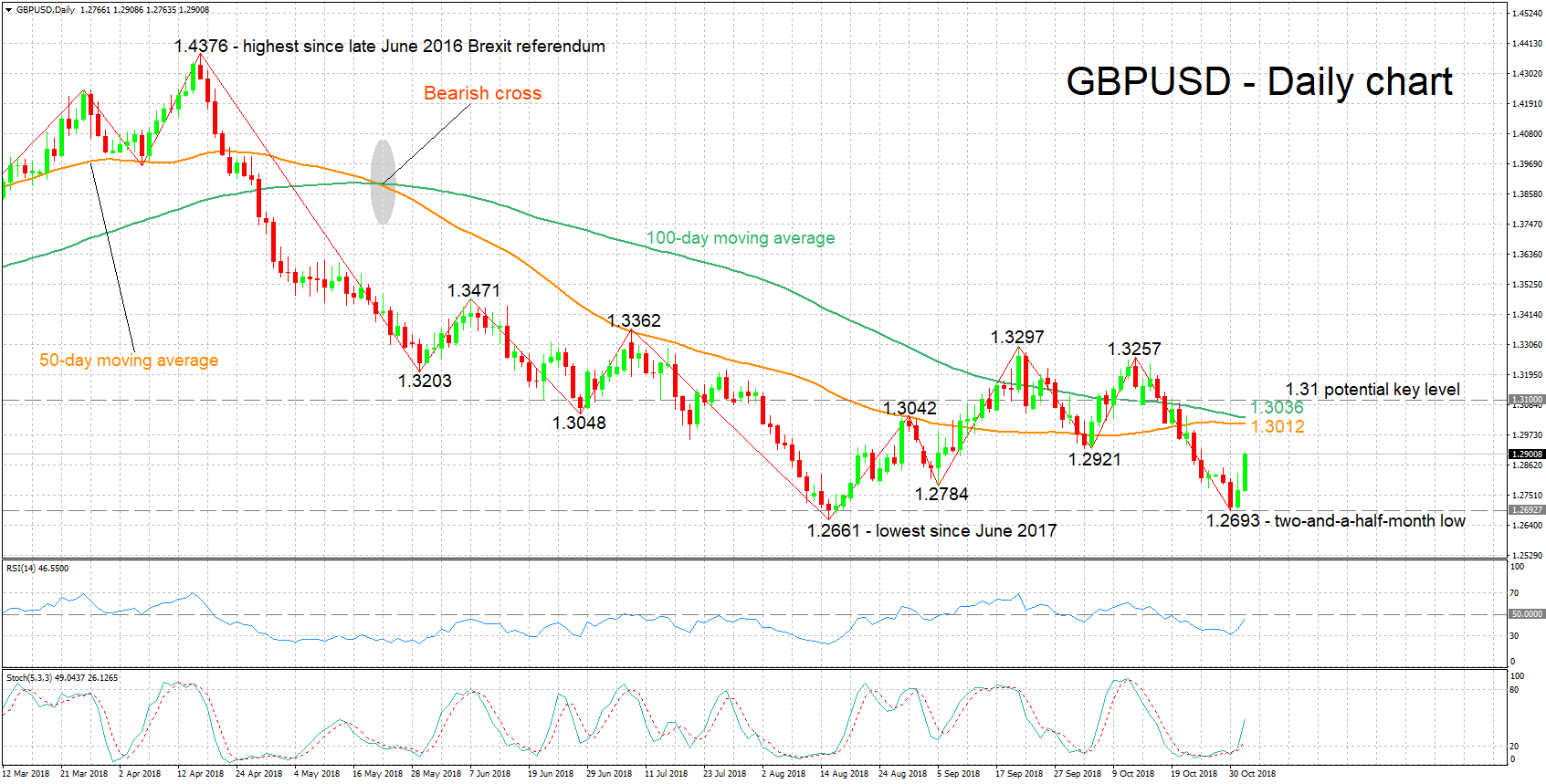

Technical Analysis: GBPUSD possible bullish tilt in the short-term

GBPUSD has posted considerable gains after touching a two-and-a-half-month low of 1.2693 on Tuesday. The RSI is in bearish territory below 50 though it has moved sharply higher after coming close to oversold levels; this signals a possible change of short-term momentum towards a bullish direction. The stochastics are also giving a bullish signal in the very short-term: the %K line has moved above the slow %D one and both lines are heading higher.

A relatively upbeat Bank of England is expected to allow the pair to build on gains. A move above a previous low at 1.2921 may see the pair meeting resistance around the current levels of the 50- and 100-day moving average lines at 1.3012 and 1.3036 respectively; the zone around these includes the 1.30 round figure, as well as a bottom (1.3048) and a top (1.3042) from previous months. Further above, the 1.31 handle would come within scope.

On the downside and in case of a cautious (dovish) BoE, support could come around a previous bottom at 1.2784, while lower still, Tuesday’s trough of 1.2693 would be eyed.

Brexit news can move the pair as well.