{kind=link}

American markets added on Wednesday, finishing the last trading session of October by a growth of 1.1% on S&P500 and 1.0% of DJI. However, October became the worst in the last 10 years, causing a decline of major U.S. indices by more than 7%.

On Thursday morning, the markets show mixed dynamics. Futures on S&P500 develop their rebound, while Asian bourses have turned to a decline after a strong start of the day.

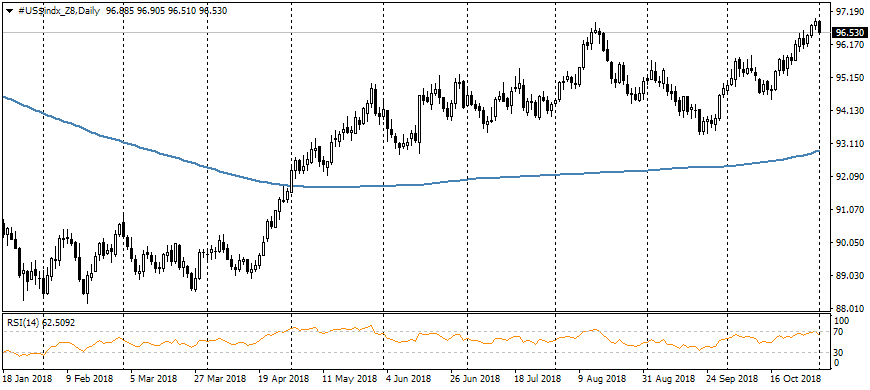

Since morning the dollar in the global market has been rolling back from 16-month highs, reflecting a timid growth of optimism at the beginning of a new month. The dollar returned to growth in October following the downward decline in stock indices. The future prospects of the US currency are largely related to the dynamics of economic performance, where an employment report is the closest major event.

Maintaining strong growth rates will reduce fears that the Fed is excessively rigid, raising rates roughly once a quarter if the economy experiences a noticeable slowdown. In this regard, the markets focus on tomorrow’s payrolls report. Preliminary data show the persistence of a tight labour market.

Often strong American statistics support the dollar, but this time it can weaken it. There is a pretty simple explanation for that. Markets take a constant plan to raise the rates of the Fed policy, and the dynamics of the economy as a variable, and fluctuations in economic data increase or reduce the attractiveness of investments in shares in comparison to the bonds.

The dollar in October showed itself as a decent barometer of the demand for risks, adding after the sale in the markets. In short-term, it seems, the pendulum swung towards the risky assets, which promulgated growth on the inflow of new money at the beginning of the month. However, it is worth remembering that all the key problems that were pressing on the markets last month remain valid: the fears of excessive austerity of the Fed policy, global slowdown, intensified trade wars, and geopolitical tensions on The Middle East.

All these factors can return focus to the market in the coming days, resuming pressure on global indices and returning the dollar to growth.