{kind=link}

The Bank of England’s latest policy decision will be made public at 1200 GMT on Thursday. The central bank is widely anticipated to keep rates unchanged, with the focus falling on monetary policy committee (MPC) members’ communication as expressed in the meeting minutes, as well as on the updated quarterly forecasts for GDP and inflation. Governor Carney’s press conference will also be eyed, as his remarks could prove instrumental for sterling’s direction in the aftermath of the rate decision.

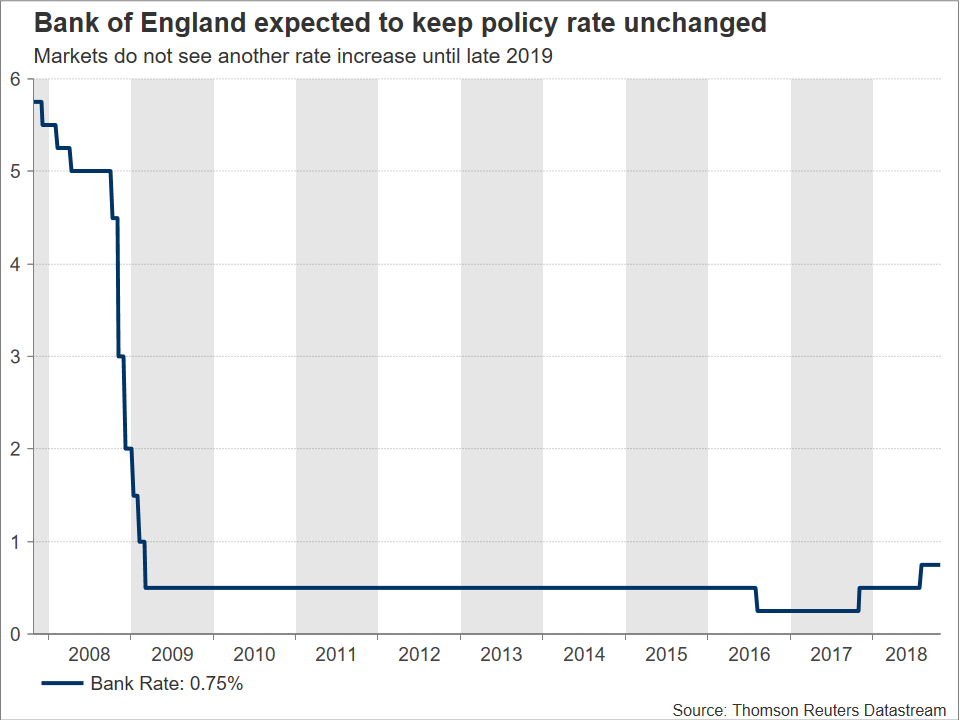

Analysts expect all nine monetary policy committee (MPC) members to vote in favor of maintaining the BoE’s policy rate at 0.75%, the level established in August when the Bank decided to hike rates for only the second time in more than a decade. In fact, swap markets show market participants don’t expect another 25bps rate increase until December 2019 – even that is not completely priced in – which reflects a less steep normalization path compared to just a few weeks ago. Contributing to the scaling back of expectations for a rate hike sooner rather than later were the recent patch of softer-than-projected data, as well as continued Brexit uncertainty.

In light of the fact that a rate rise is practically off the table, the meeting minutes and fresh economic projections also due at 1200 GMT will probably be those fueling positioning on sterling. For example, optimism on behalf of the BoE that portrays a more aggressive tightening cycle compared to the previous guidance for “limited and gradual” rate rises, has the capacity to boost the pound. However, a gloomier outlook that could exert selling pressure on the British currency may be more likely on offer: inflation exceeds the Bank’s annual target of 2%, but it came in weaker than expected during September, while retail sales for the same month also missed forecasts by a relatively large margin. On top of these, Brexit uncertainty remains firmly on the table as the UK’s exit from the EU in late March draws ever closer; will a deal with the EU be struck or will a disorderly Brexit take place?

Overall, worries over a no-deal Brexit, in conjunction with the recent weaker-than-expected data, suggest than a downside revision in GDP forecasts may be more likely by the Bank than an upgrade. On inflation, the risks appear roughly balanced. Softer CPIs may tilt things towards a downgrade, but a declining pound – GBPUSD is trading not far above a more than one-year nadir – poses upside risks to inflation and this is something that may be stressed by policymakers, perhaps by Carney himself during his press conference set to take place at 1230 GMT. Such a comment is likely to prove sterling-positive. Any remarks on Brexit and global trade also rank high in terms of significance, having the potential to move the pound.

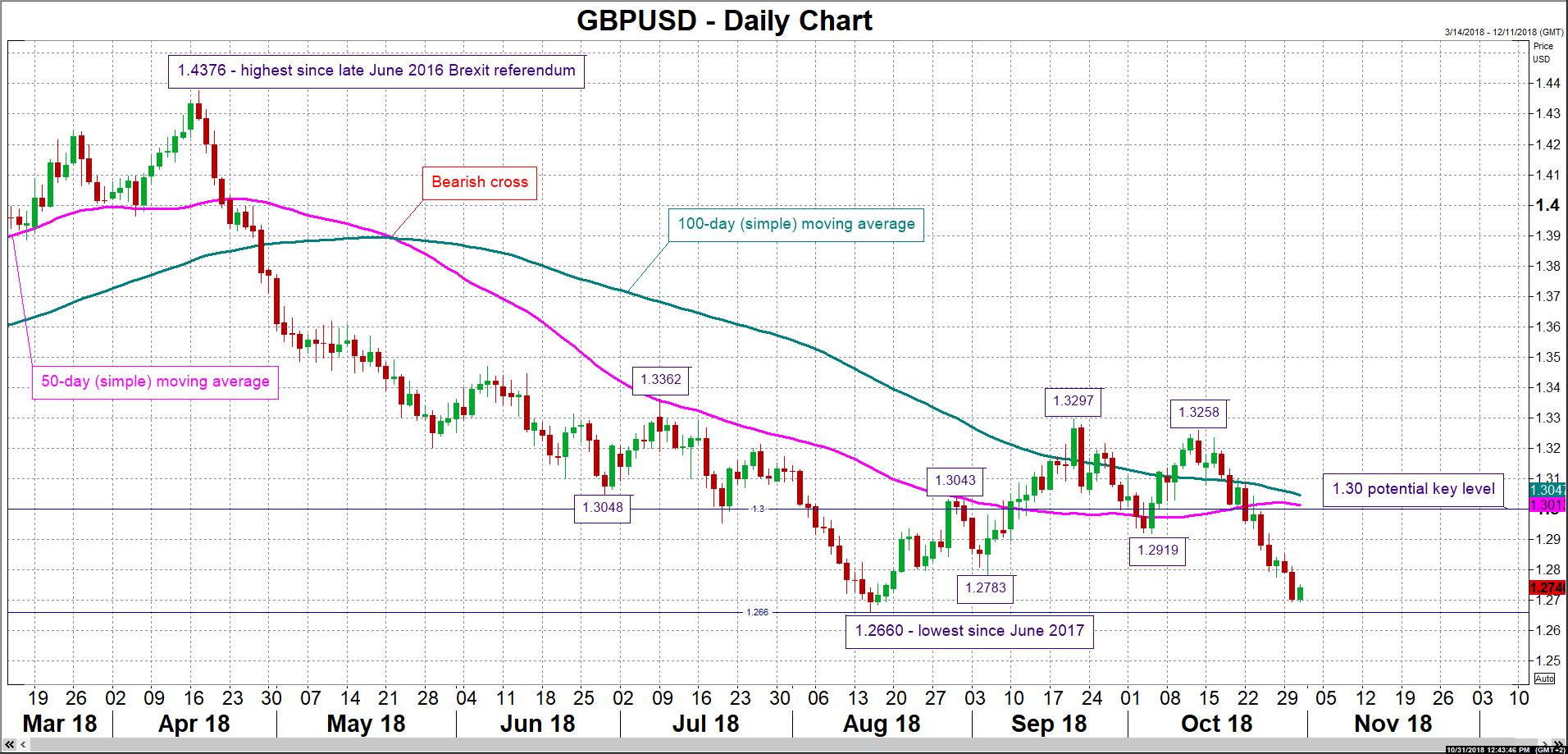

In FX markets, a relatively upbeat BoE is expected to lead to long sterling positions. Given a move above a previous low at 1.2783, the attention would turn to the zone around early October’s bottom of 1.2919 as a possible resistance area. Further above, the 1.30 handle which may hold psychological importance could prove an important barrier in the event of stronger gains; the 50- and 100-day moving average lines lie not far above this mark. On the downside and in case of a pessimistic tone by the Bank, the region around August’s more-than-one-year low of 1.2660 could provide support. After that, the June 2017 trough at 1.2587 would come into view. Lower still, the April 2017 bottom of 1.2362 would increasingly come into scope. Notice that there’s negative momentum currently in place, with the pair roughly trading at its lowest since late August.

Lastly, the figures for October’s UK manufacturing PMI will also be hitting the markets ahead of the rate decision on Thursday, at 0930 GMT; construction PMI will be released on Friday, with the relevant reading on the all-important services sector due on Monday.