{kind=link}

Here are the latest developments in global markets:

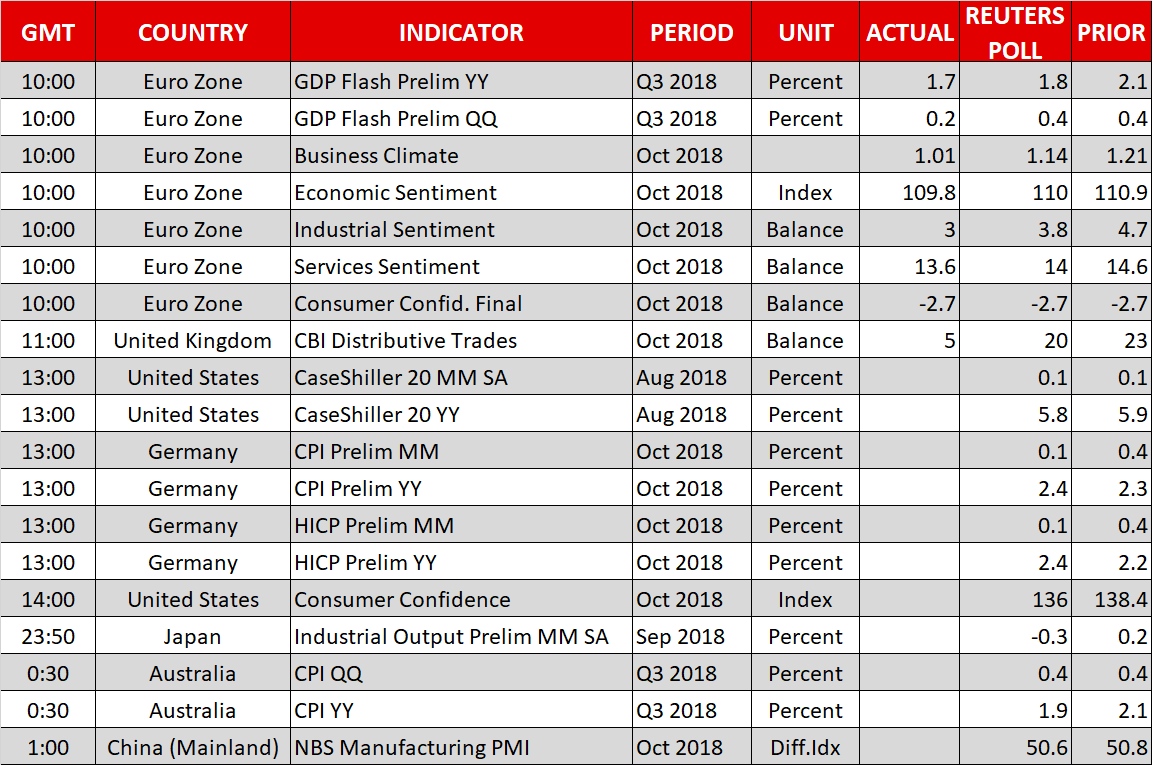

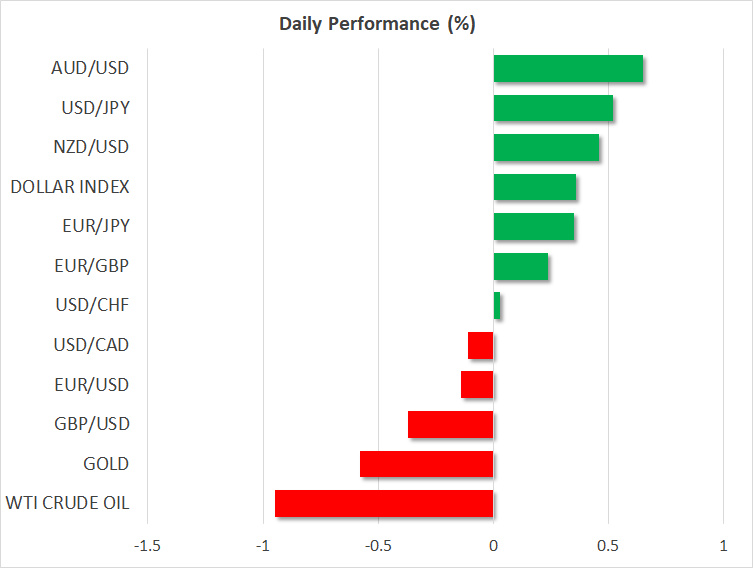

- FOREX: Eurozone’s initial GDP growth estimate for the third quarter was rather disappointing, clocking in at 1.7% y/y, the lowest since Q4 2017. On a quarterly basis, expansion unexpectedly slowed to 0.2%, from 0.4% previously. Consumer confidence was confirmed at -2.7 in October, not far above the 1 ½ -year low of -2.9 reached in September. Yet investors’ mood didn’t deteriorate significantly in the wake of the data, even under rising political noises in Italy and Germany, sending euro/dollar slightly down to 1.1349 (-0.15%). Pound/dollar eased to a fresh two-month low of 1.2753 as the dollar continued to gain ground after the US President said that the government will make a great trade deal with China, a few days before US midterm elections take place. That said, headlines stating that the US still considers unleashing tariffs on all Chinese imports kept sentiment somewhat subdued. Speaking in Oslo, the UK PM argued that the government is not planning another general election. Dollar/yen moved up to 112.82 (+0.40%), while the dollar index crawled up to 96.86 (+0.29%). In antipodean currencies, aussie/dollar fully recovered yesterday’s downfall, rising to 0.7089 (+0.49%) before Q3 CPI figures come out of Australia. Kiwi/dollar was also on the upside for a second day, at 0.6542 (+0.34%). Dollar/loonie softened to 1.3120 (-0.08%). In emerging currencies, onshore yuan dropped to a fresh decade-low against the greenback

- STOCKS: European stocks were mostly on the downside at 1200 GMT. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 were almost flat. The German DAX 30 declined by 0.34% as the German Lufthansa air carrier reported disappointing profits for the third quarter and said that the number of flights will rise more modestly this year compared to other airlines. General Electric’s earnings came in weaker than expected, while Volkswagen’s and Coca Cola’s results beat forecasts. The French CAC 40 dipped by 0.29% and the Italian FTSE MIB dropped by 0.33%. On the other hand, the British FTSE 100 was marginally up by 0.14% due to a positive budget update. In Asia, stock indices closed mixed, while in the US, futures tracking the S&P 500, Dow Jones and Nasdaq 100 were flashing green, pointing to a higher open of around 0.5% for these indices today.

- COMMODITIES: Oil reversed earlier losses and turned negative on the day as investors feared that additional import tariffs on China would harm demand for crude at a time when US crude inventories are still on the rise and US sanctions on Iran are just about to take full effect. WTI crude and Brent were weaker by 0.95% and 1.16% respectively. In metals, copper tumbled by 1.15% and gold extended south to $1221.8 (-0.61%).

Day ahead: German inflation numbers due ahead of Australia’s; BoJ rate decision eyed

The economic calendar is not particularly packed over the remainder of Tuesday’s session, with German inflation figures being the highlight. The Asian session on Wednesday promises to be much more entertaining, with Australia’s own inflation numbers and a rate decision by the Bank of Japan (BoJ) being high on the agenda. As always, any updates on the trade and political fronts could well impact currency, bond, and stock markets.

In Germany, preliminary inflation data for October will hit the markets at 1300 GMT. Forecasts point to an uptick in the EU-harmonized yearly rate to 2.4%, from 2.2% previously. Germany’s numbers come out one day ahead of the Eurozone-wide release and hence, may be seen as a gauge of what is in store for the entire bloc. That said, considering that the regional German CPIs have already been released and were broadly in line with the nationwide forecast, any major surprise and hence reaction in the euro seems unlikely.

In the US, the Conference Board consumer confidence index for October is due out at 1400 GMT and expectations are for a pullback, though from an elevated two-decade high level. The S&P/Case-Shiller house price index for August will also be released earlier at 1300 GMT.

On the equity front, Facebook will publicize its own earnings results after Wall Street’s closing bell.

In energy markets, the weekly private API crude inventory data are due at 2030 GMT.

As for public appearances, ECB Executive Board members Praet and Lautenschlager will deliver remarks at 1330 GMT and 1410 GMT respectively, while Bank of Canada Governor Poloz will speak before lawmakers at 1930 GMT.

Later during the Asian session on Wednesday, the focus will shift to Australia’s CPI prints for Q3, due at 0030 GMT. Projections suggest inflationary pressures cooled a little, with the headline CPI rate expected to dip to 1.9% in yearly terms, from 2.1% previously. That said, measures of underlying inflation (trimmed & weighted mean) are anticipated to have held steady at 1.9% as well, so the pullback in the headline rate may not be particularly worrisome for the RBA – which meets next week.

In China, the official manufacturing and non-manufacturing PMIs for October are due for release at 0100 GMT.

Finally, the BoJ will announce its rate decision. No change in policy is expected, with the reaction in the yen instead likely to depend on any updates in the Bank’s assessment of the economy and forecasts – if any. Although Japan’s inflation picture remains tepid, growth-related indicators have picked up some steam lately, which may lead the BoJ to appear a tad more optimistic on the outlook. While that may prove slightly positive for the yen, the currency’s broader direction will likely be decided by how risk appetite develops in financial markets, given its safe-haven status.