{kind=link}

Here are the latest developments in global markets:

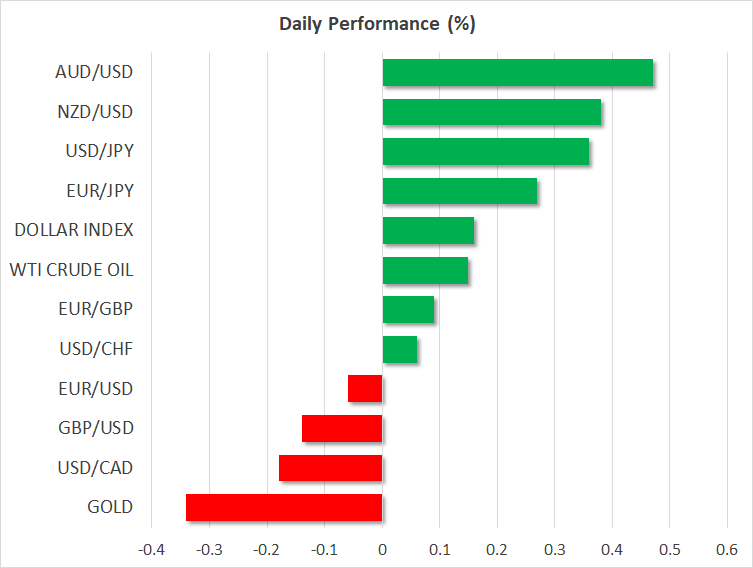

FOREX: The dollar is higher by 0.17% against a basket of six major currencies on Tuesday, building on the gains it posted yesterday as risk appetite deteriorated and investors sought the safety of the world’s reserve currency. The defensive yen surprisingly underperformed despite the general risk-off mood on Monday. Meanwhile, the aussie and kiwi are both notably higher on Tuesday as risk sentiment seems to have reversed, following hints from President Trump that he is still seeking a trade deal with China.

STOCKS: Wall Street had a turbulent session, with the major indices wiping out early gains to close lower after reports that the US may announce tariffs on all remaining Chinese imports by next month. The tech-heavy Nasdaq Composite underperformed (-1.63%), as separate news that the UK is aiming to tax the sales of major technology firms weighed. The Dow Jones (-0.99%) and S&P 500 (-0.66%) followed in its tracks. That said, futures tracking the Dow, S&P, and Nasdaq 100 are pointing to a higher open today, aided by remarks by President Trump that he anticipates a ‘great deal’ with China. Indeed, the optimism carried over into Asia on Tuesday, with Japan’s Nikkei 225 (+1.45%) and Topix (+1.38%) advancing alongside South Korea’s Kospi 200 (+0.88%). In Europe, all the major indices are expected to open modestly higher today, futures suggest.

COMMODITIES: Oil prices were marginally higher on Tuesday, for the most part consolidating losses recorded on Monday, which came on the back of sustained weakness in risk sentiment. In precious metals, dollar-denominated gold is down by 0.34% today at $1,223 per ounce, extending losses from yesterday and suffering at the hands of a stronger greenback, despite the ongoing rout in equity markets. The inability of the yellow metal to attract safe-haven flows yesterday despite the market jitters is notable, though the fact that prices continue to trade above the 100-day simple moving average may provide some comfort to the bulls.

Major movers: Stocks whipsaw as risk sentiment remains fragile

US markets had a rather volatile session, with major indices like the S&P 500 erasing early gains to trade lower, after media reports suggested the US will announce tariffs on all remaining Chinese imports if the Trump-Xi talks fail next month. Tech stocks and the Nasdaq in particular were already under pressure, after UK Chancellor Hammond announced plans for tech giants to pay tax on the sales they generate in Britain.

Coming on top of concerns that earnings growth may have peaked already, and with markets still adjusting to the prospect of higher interest rates, the renewed focus on tariffs likely added one more dimension to the risks equity investors have to wrestle with. That said, the mood seems to have recovered as Asian markets closed mostly in the green on Tuesday and US equity futures are pointing to a higher open, likely buoyed by President Trump saying overnight he expects a ‘great deal’ with China. Hence, business as usual on the trade front, with his ‘carrot and stick’ approach remaining the weapon of choice for now.

Most noteworthy was the fact that the typical correlations between currencies and stocks decoupled. Namely, although stocks were on the back foot on Monday, the safe-haven Japanese yen also fell across the board alongside gold, instead of attracting defensive inflows. Moreover, risk-sensitive commodity currencies like the aussie curiously outperformed; one would have expected it to be hit the hardest in the midst of risk aversion.

In euro land, the single currency was caught between two narratives. On the one hand, Italy avoided a credit downgrade by the S&P and the nation’s politicians are showing signs they may be willing to compromise on their 2019 deficit. On the other, news that German Chancellor Merkel won’t run for re-election as leader of her CDU party kept a lid on the cheerfulness.

In the UK, Chancellor Philip Hammond delivered the Autumn Budget, which signaled a gradual move away from austerity, and importantly also contained a digital services tax aimed at companies like Amazon and Facebook. The caveat was that everything is liable to change depending on how the Brexit talks play out. Understandably, the pound was little changed on the news.

Day ahead: Eurozone GDP, German inflation, US consumer confidence on the agenda; trade developments closely watched

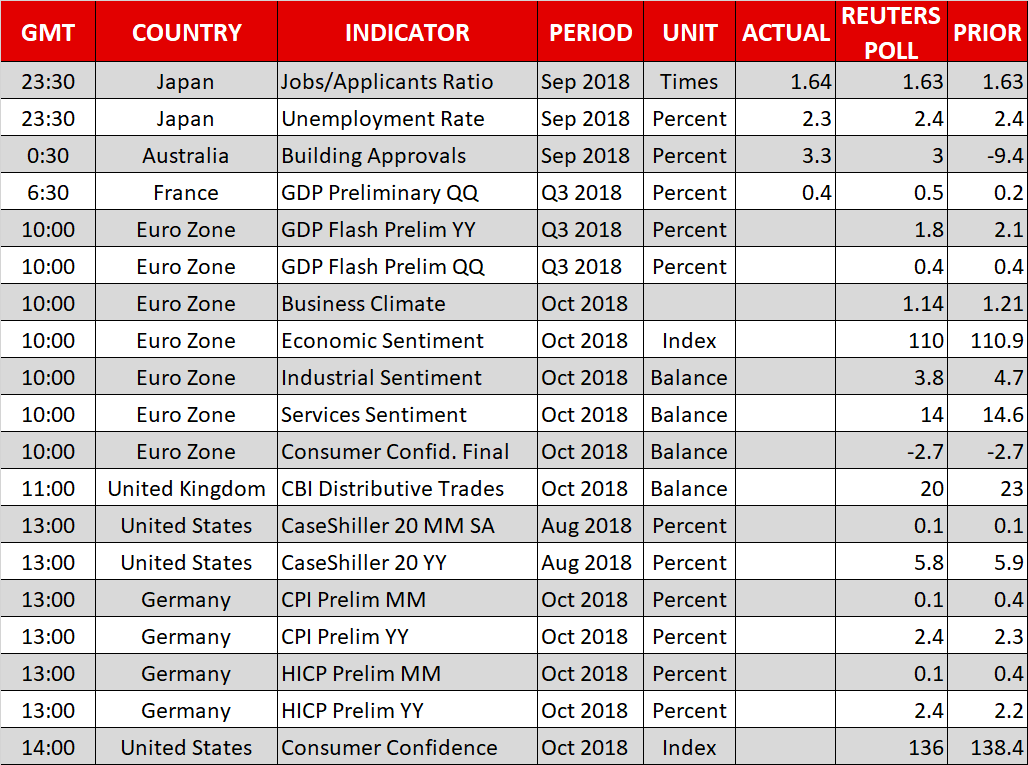

Tuesday’s a busy data day with eurozone GDP, German flash inflation figures and US consumer confidence being among the releases attracting interest. Any developments on global trade – the Sino-US standoff – also rank high on the agenda, having the potential to lead to heightened volatility in the markets.

At 1000 GMT, preliminary eurozone GDP numbers for Q3 will be made public. Economic activity is anticipated at 0.4% q/q for the third straight quarter, notably below the 0.7% between Q2-Q4 2017; hopes that the economy would pick up steam appear to have not materialized. Year-on-year, the euro area is anticipated to have expanded by 1.8% in Q3, below Q2’s 2.1%.

Numerous surveys gauging business sentiment in the eurozone during October are also due out at 1000 GMT. All are expected to show worsening morale relative to September; rising trade tensions and political uncertainty – Italian budget worries and a relatively fragile German government coalition – are factors that are negative for sentiment.

Elsewhere, eurozone consumer confidence data out at the same time as the readings on GDP are forecast to confirm the preliminary release’s -2.7, this being an improvement compared to September, though still constituting the fifth straight print within negative territory. For comparison, the US Conference Board’s consumer confidence index for October scheduled for release at 1400 GMT is expected to ease a bit, though still remain close to September’s near two-decade high.

Also having potential to drive euro pairs will be October flash inflation readings out of Germany at 1300 GMT. Month-on-month, CPI growth is expected at 0.1% (below September’s 0.4%), which would put the year-on-year pace of expansion at 2.4% (above the previous month’s 2.3%). The harmonised figures (HICP), that use a common methodology across EU countries, will also be monitored. The numbers come one day ahead of the eurozone’s corresponding inflation prints and traders may thus use today’s figures to speculate on tomorrow’s euro-wide release, positioning themselves accordingly. Also out of Germany, October’s unemployment data are due at 0855 GMT.

Besides some data from the Confederation of British Industry, which either way do not tend to be market moving, the UK calendar is empty; sterling will again be most sensitive to any news on Brexit. In the meantime, PM May will be talking at the opening session of the Nordic Council at 1315 GMT.

Other US releases are August’s CaseShiller indices that gauge house prices (1300 GMT).

Trade angst acted as the catalyst behind major Wall Street indices erasing earlier gains to finish Monday’s session lower; this also brought to the fore the greenback’s safe-haven allure. Any headlines building on yesterday’s reports that President Trump plans to ramp up tariff action against China if talks between him and Chinese President Xi at next month’s G20 summit fail to lead to a breakthrough will be closely watched.

ECB chief economist Praet and the Bank’s board member Lautenschlager will be making public appearances at 1330 GMT and 1410 GMT respectively. Bank of Canada Governor Poloz and Deputy Governor Wilkins will be speaking at 1930 GMT.

In equities, Facebook and Coca-Cola are among companies releasing quarterly results today; the latter will be reporting before Wall Street’s opening bell and Facebook after the market close. Meanwhile, Apple will be unveiling new product offerings at an event in New York today.

In energy markets, weekly API data on US crude stocks are due at 2030 GMT.

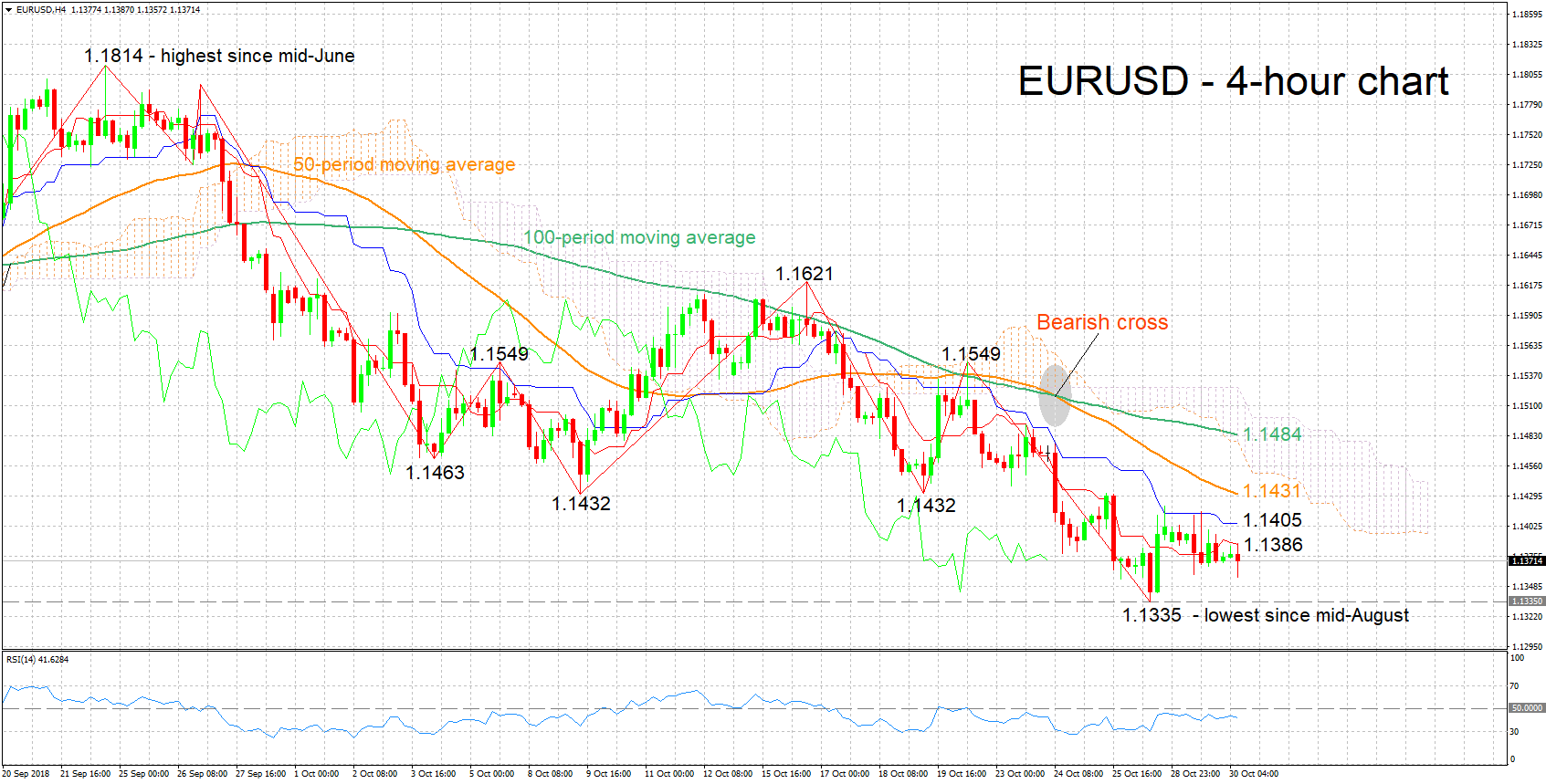

Technical Analysis: EURUSD negative bias may be easing

EURUSD is trading roughly 35 pips above Friday’s lowest since mid-August of 1.1335. The Tenkan- and Kijun-sen lines are negatively aligned in support of a negative short-term bias. The Kijun-sen though has halted its decline, a sign that bearish momentum may be easing. The RSI which is in bearish territory but is largely moving sideways also supports this view.

Upbeat eurozone releases could push the pair higher. Immediate resistance may take place around the Tenkan- and Kijun-sen lines at 1.1386 and 1.1405 respectively. Not far above lies the current level of the 50-period moving average at 1.1431; the zone around this captures the Ichimoku cloud bottom (around 1.1450), as well as numerous bottoms from the recent past. Higher still, the 100-period MA at 1.1484 would come into scope.

Conversely, disappointing numbers are likely to exert selling pressure on EURUSD. Support to losses could occur around Friday’s low of 1.1335. Lower, the 1.13 figure, which roughly coincides with the pair’s lowest since late June 2017 recorded during August, would come into focus. Even lower, the 1.12 handle would be eyed.

Trade developments and US releases can also move the pair.