{kind=link}

Here are the latest developments in global markets:

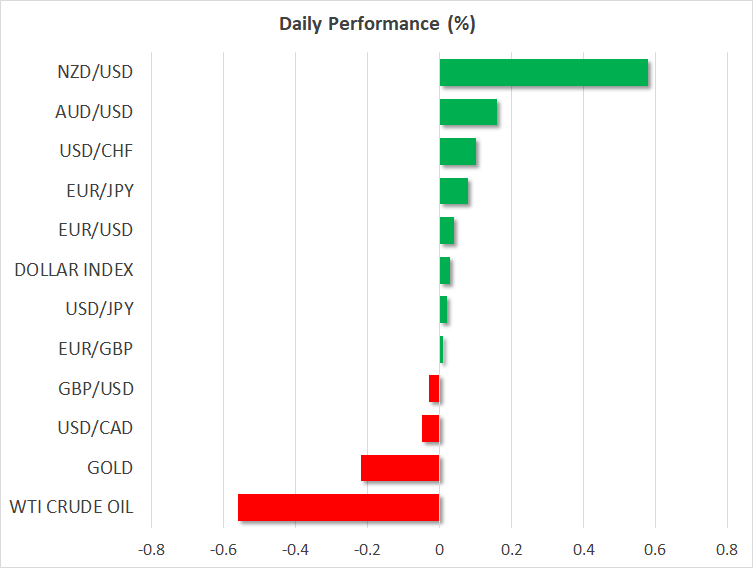

FOREX: The US dollar was flat after giving up earlier gains following Monday’s Asian trading and most major pairs were close to the levels they closed on Friday. The dollar index was trading around 96.15, well off Friday’s high of 96.62. One currency that was managing to significantly gain against the greenback was the kiwi by nearly 0.6%.

STOCKS: Markets were mixed on Monday, following the equity sell-off of the previous week. US index futures were down by about 0.2%. Chinese stocks were facing yet another sizeable sell-off, with the Shanghai Composite down by more than 2% today on fears of a slowdown in the Chinese economy. Other Asian-Pacific markets were faring better however, with the Japanese Nikkei posting minor losses of 0.16% while in Australia the S&P/ ASX 200 was up by more than one percent. European indices were expected to open higher following Friday’s sell-off, demonstrating some resilience to the negative mood.

COMMODITIES: Gold was consolidating above the 1230 dollars an ounce level, following its failure to hold on above 1240 – a fresh three-month high – during Friday’s trading. Oil for its part gave up some of Friday’s gains on renewed worries about a global slowdown, trade tensions and a ramp-up in production by other major oil producers to make up for the shortfall caused by the sanctions on Iran. Oil has been trading negatively recently and WTI Crude futures are still well below the $70 a barrel level at 67.33.

Major movers: Dollar longs emboldened by GDP report; focus still on stocks

The start of the week was relatively quiet but the focus still remained on whether the stock selloff was going to continue. On Friday, not even a stronger-than-expected third quarter US GDP number was enough to support equities, as many probably preferred to see the negative side of things. Mainly, that strong US economic numbers would push the Fed towards more interest rate hikes, which in turn would bring more pain to US stock market investors who have seen stocks more than triple in value from their lows during the last 9 years. However, the prospect of higher US interest rates as well as more turbulence in the stock market, could help the US dollar move higher; both on safe haven grounds as the world’s reserve currency and as the currency’s yield would compare favorably with other major currencies.

Both the euro and the pound have managed to rebound strongly from their lows on Friday against the US dollar. For the euro, Italy’s budget woes combined with a drop in business optimism have led to selling of the single currency. The one supportive factor was that the ECB said it was still planning to end bond purchases by year-end and start raising interest rates in the fall of 2019. Many investors are worried that the ECB might delay its stimulus withdrawal if the Italian situation worsens and if the Eurozone economy deteriorates further. On a positive note for the euro, Germany’s Angela Merkel received backing from her junior coalition partners for another year, despite negative showings in recent regional polls in the country.

For the pound, there is uncertainty as to the extent of domestic political support that Prime Minister Theresa May can count on even if she does manage to conclude a deal with the EU regarding Brexit. These worries led to a two-and-a-half-month low in cable on Friday, but today there was a bounce from this level. Headline-driven volatility is expected to remain high for sterling, but traders are likely to keep the lows below 1.28 in their sights.

Finally, safe havens such as the Japanese yen and the Swiss franc are also attracting traders’ attention. The Japanese yen is the one currency that seems to be consistently outperforming the US dollar – even by a small margin – when there is a stock sell-off.

Day ahead: Key US data and UK autumn budget due, with “familiar” market themes still in focus

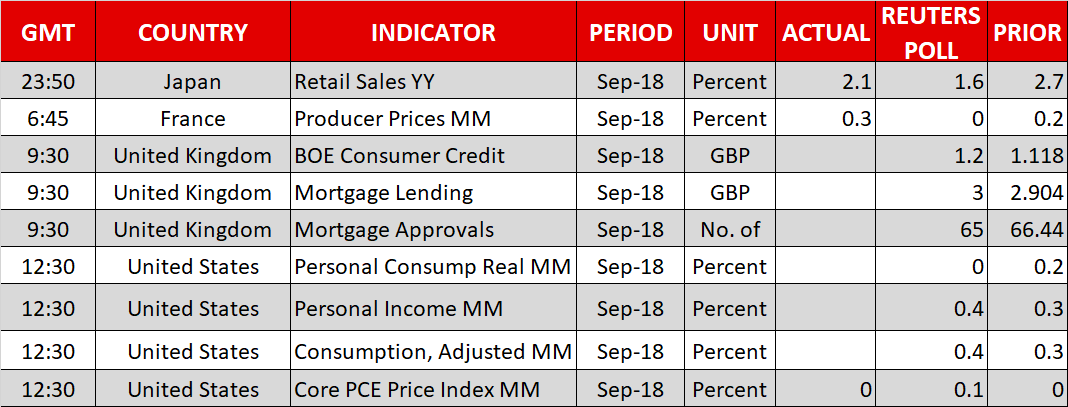

Besides a raft of economic data due out of the US, the economic calendar is relatively light on Monday. Market attention is likely to remain firmly on the themes that have been in the spotlight lately: the fragility in stocks, Italy’s budget, Brexit, and trade issues.

In terms of the data, the US will see the release of its personal income and spending figures for September, as well as the Fed’s preferred inflation gauge, the core PCE price index – all at 1230 GMT. Forecasts point to an acceleration in both income and spending in monthly terms to 0.4%, from 0.3% in August. Meanwhile, the core PCE index is anticipated to have risen by 0.1% on a monthly basis in September, which would keep the yearly rate unchanged at 2.0%; exactly in line with the Fed’s inflation target.

At the time of writing, market-implied odds derived from the Fed funds futures point to a 75% probability for the Fed to raise rates again in December. If indeed these prints come in as expected or stronger, then investors could price in an even greater likelihood for such an action and thereby, bring the dollar under renewed buying interest. Of course, any disappointment is likely to lead to the opposite market reaction, namely a softer dollar.

As for public appearances today, Chicago Fed President Charles Evans (non-voting FOMC member in 2018) will deliver remarks at 1245 GMT. In the UK, all eyes will be on Chancellor Hammond, who is due to deliver the Autumn budget to Parliament. The DUP party – which is currently propping up Theresa May’s government – has previously warned it may vote against this budget if May was to breach any of their red lines over Brexit, and it will be interesting to see their stance today.

The rest of the week promises to be much more entertaining, with policy meetings both by the Bank of Japan and the Bank of England, as well as a US employment report and Eurozone inflation figures, all likely to keep investors on edge.

In equities, some notable names releasing quarterly earnings this week include Facebook, Ebay, and Pfizer on Tuesday, Blackrock and General Motors on Wednesday, as well as Apple on Thursday.

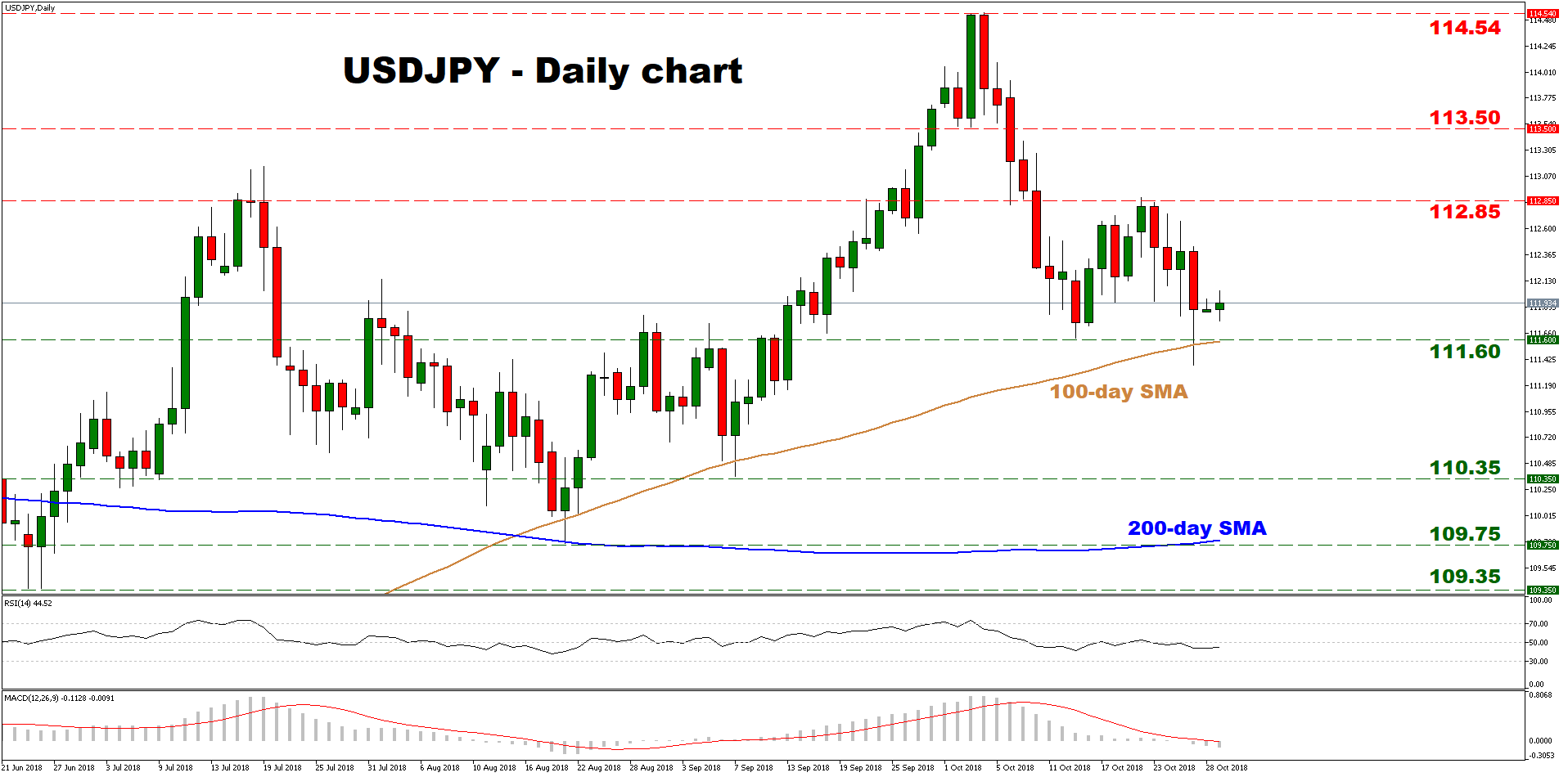

Technical Analysis – USDJPY appears neutral in the short-run

USDJPY touched a one-year high in early October, but subsequently reversed lower and has posted successive lower lows since then. However, the fact that the pair continues to hover above both its 100- and 200-day simple moving averages (SMA) keeps the near-term outlook neutral for now. Short-term momentum oscillators on the daily chart support that the picture is relatively flat. A move below 111.60 and the 100-day SMA is needed to turn the bias to cautiously negative.

If the US data are stronger-than-anticipated today, the bulls could retake the reins and aim for a test of the 112.85 area, defined by the highs of October 22. An upside break could open the way for the 113.50 zone, marked by the inside swings low on October 3, before the one-year high of 114.54 comes into view.

On the flipside, a disappointment in the data may bring the pair under renewed selling pressure. Immediate support to declines may be found near the crossroads of the 111.60 hurdle and the 100-day SMA. Even lower, the September 7 low of 110.35 would increasingly attract attention, ahead of the August 21 trough at 109.75.

Beyond US data, any change in investors’ risk appetite can also affect the pair, given the yen’s safe-haven status.