{kind=link}

The Bureau of Economic Analysis will update its core Personal Consumption Expenditure (PCE) price index, which the Fed consults to set monetary policy, on Monday at 1230 GMT. The data are expected to show that inflation dropped a shy below the central bank’s price target. However, upside inflationary risks stemming from the US labor market and the restrictive trade environment could be a good reason for the Fed to continue to raise interest rates in the coming years to keep inflation at the target.

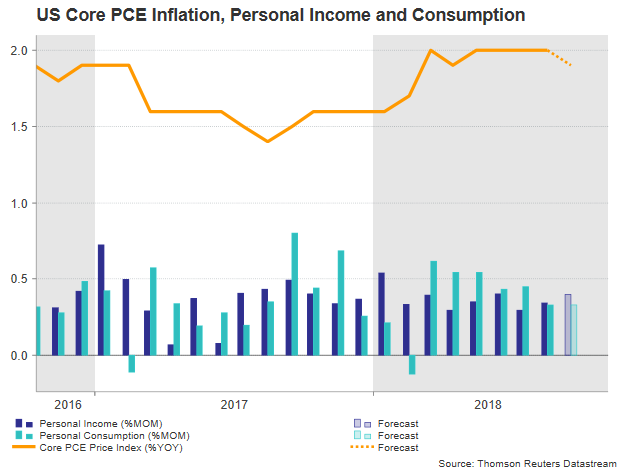

According to forecasts, the core PCE price index which strips out food and energy is said to have inched down to 1.9% year-on-year after holding at 2.0% for the past four months, still remaining the highest in 6 years.

While inflation looks to be holding at the target, the Fed has pledged to keep raising interest rates in the coming years despite the US President’s complaints about fast rising borrowing costs. A tightening labor market seems to be the bigger trigger behind the Fed’s rate plans as wage growth is awaited to return to the nine-year high of 2.9% y/y in October after inching down to 2.8% in September. The unemployment rate is also on the plus side, as it is anticipated to flatten at 3.7% in the same month, at the lowest since 1969, reflecting sustained consumer spending in the future. Note that the new USMCA trade agreement between the US, Canada and Mexico which replaced the previous NAFTA deal has stricter local content and minimum wages requirements, which would translate into higher labor costs in the future once the accord gets approved from legislative bodies in each nation probably by 2020.

Looking at personal consumption and personal income readings published alongside inflation figures, household spending is expected to have improved by 0.3% m/m in September as in August. Recall that on Friday personal consumer expenditures appeared higher by 4.0% in annualized terms in the third quarter compared to 3.8% in Q2, posting the strongest advance since Q4 2014, while consumption’s net contribution to the surprisingly larger 3.5% US GDP growth in the third quarter was the biggest relative to other GDP components, at 2.69%.

Income including wages and other benefits received by consumers is anticipated to have grown by 0.4% m/m in September versus 0.3% seen in August. This is above the anticipated 0.1% monthly increase in the core PCE index and thus consumption-positive.

US import tariffs are another supportive factor for inflation as higher costs to buy from abroad especially from China, which faces restrictions to a bigger list of exported products, reduce profit margins for US businesses. This in return forces companies to raise prices. Yet the dollar’s appreciation in September has probably limited the positive tariff effect on import prices, though this would also have made US products more expensive abroad. Recall that China has taken countermeasures against the US as well, imposing tariffs on US imports and hence turning US goods sold overseas less competitive. It is also worth noting that net exports substracted 1.78% from GDP growth.

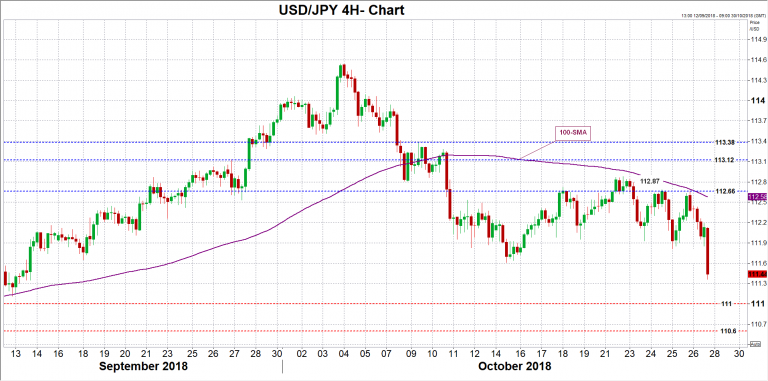

Should inflation or personal consumption/income readings arrive stronger than analysts project, justifying Fed’s decision to deliver further rate hikes in coming years, dollar/yen could bounce back above the 112.00 handle and test the recent peaks between 112.66 and 112.87, while if these fail to hold, traders could look for resistance in the 113.12-113.38 area, identified by the highs on September 26 and October 9 respectively.

In the alternative scenario, a miss in the data would increase worries that inflation has reached its peak at 2.0%, putting investors into doubts about whether the Fed should move with further monetary tightening in the future. The odds for a rate hike in December may decline as well. In the aftermath, dollar/yen could weaken towards the 111.00 psychological mark, while steeper declines could find support around 110.60 before eyes turn to the 110 round level.