{kind=link}

Here are the latest developments in global markets:

FOREX: The dollar is down by 0.21% against a basket of six major currencies on Thursday, giving back some of the gains it posted yesterday, when it capitalized on weakness in the euro. Meanwhile, the defensive yen recovered early losses on Wednesday to finish the session as the second-best performer, as the stock sell-off accelerated. The best performer was the loonie, which soared after the Bank of Canada (BoC) raised rates and appeared more hawkish, dropping some cautious language it had used previously.

STOCKS: The selloff in Wall Street accelerated markedly on Wednesday, with the S&P 500 (-3.09%) and the Dow Jones (-2.41%) both erasing all their gains for 2018, to trade modestly lower year-to-date. Meanwhile, tech underperformed, with the Nasdaq Composite plunging (-4.43%) as disappointing guidance from Advanced Micro Devices (AMD) may have heightened speculation for more poor results by other firms, dampening sentiment. The pessimism rolled over into Asia on Thursday as well, with Japan’s Nikkei 225 (-3.72%) and Topix (-3.10%) feeling most of the heat. In Hong Kong, the Hang Seng lost 1.85%, while South Korea’s Kospi 200 dropped by 1.71%. Futures tracking major European indices were a sea of red, pointing to a lower open today.

COMMODITIES: Oil pared early gains to close the session little changed, as the broad-based risk aversion weighed on energy shares, and also clouded the precious liquid’s demand outlook. Prices are also lower on Thursday, with WTI being down by 0.54% at $66.43 per barrel, while Brent lost 0.75% to trade at $75.60/barrel. In precious metals, gold is up by 0.27% today at $1236 an ounce, having met resistance near the $1240 area earlier. The yellow metal is slowly regaining its shine amid the market turmoil, advancing despite a stronger dollar yesterday, as speculators continued to unwind more of their prior net-short bets.

Major movers: Yen remains bid as stock selloff accelerates; loonie soars after BoC

Risk sentiment remained in negative territory on Wednesday, with US equity markets and most notably the Nasdaq Composite (-4.43%) bearing the brunt of the pain. The S&P 500 (-3.09%) wiped out all its gains year-to-date, and is now actually down by 0.65% in 2018. Asian markets took their cue from Wall Street and closed sharply lower, while the Japanese yen – whose haven qualities have been on full display in recent days – advanced almost across the board as investors sought shelter.

In terms of catalysts, besides the familiar themes (trade, Italy, yields), increasingly downbeat forward guidance by US firms releasing earnings likely contributed as well. The latest was chipmaker AMD (-9.17%), where executives now expect weaker revenue going forward, echoing similarly pessimistic remarks from industrial bellwether Caterpillar (-5.58%), indicating that firms across entirely different sectors are facing headwinds. Hence, softer expectations from corporates may have amplified the narrative that “peak growth” is behind us, leading investors and funds to place more emphasis on protecting any gains they have recorded already this year, as opposed to expanding them. Earnings and guidance from heavyweights including Google-parent Alphabet, Amazon, and Intel, could be crucial in shaping sentiment today.

In Canada, the BoC raised rates – as was widely expected – and appeared more confident on the outlook. Specifically, policymakers dropped a previous reference that rate hikes will be gradual, while they also brushed aside the recent slowdown in wages as being a transitory phenomenon that will dissipate soon. While they did highlight key risks, like the adjustment of highly-indebted households to higher rates and the US-China conflict, markets focused more on the upbeat signals – sending the loonie higher, though the currency later pared some of its gains on weak risk appetite.

Elsewhere, euro/dollar fell to a fresh two-month low near 1.1380, weighed down mainly by disappointing euro area PMIs for October. The soft prints may have been seen as an early hint the bloc’s weakness earlier in the year may have carried over into the final quarter. In light of the ECB meeting today as well, it likely generated some speculation for a more cautious tone by Draghi & Co.

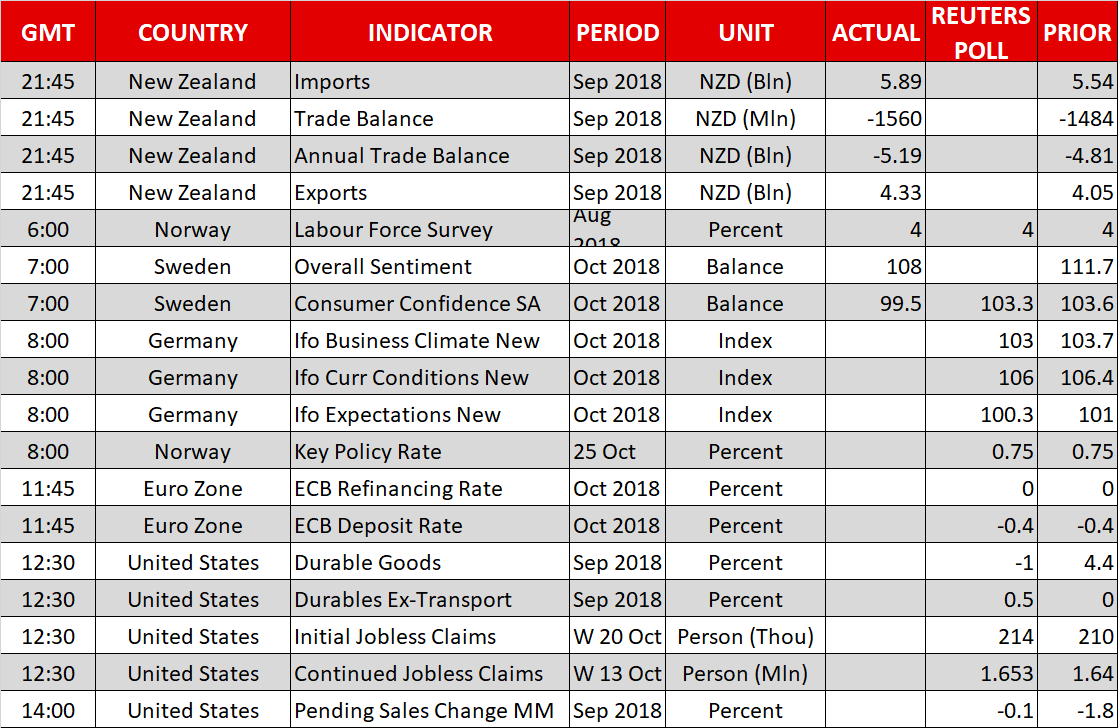

Day ahead: ECB concludes policy meeting; US durable goods orders in focus for growth direction

The European Central Bank concludes its two-day monetary policy meeting at 1145 GMT and policymakers are expected to reiterate the already well-known story that interest rates will remain steady until the end of the 2019 summer, while the 2.5 trillion-euro quantitative easing program will stop at the end of December. Hence the focus will shift to the press conference and to the ECB chief Mario Draghi who will probably try to give an explanation about whether global risks could translate into further growth slowdown in the eurozone, something already hinted by the PMI figures. Specifically, investors would like to hear Draghi’s opinion about the Italian budget and if the central bank is planning to provide any assistance, something Draghi denied earlier, saying that the Bank is not responsible for supporting individual governments. Trade is likely to be another topic in discussion. Recall that in the previous meeting Draghi said that the outlook is “broadly balanced”. Should the ECB chief stand more cautious by changing this wording to a more dovish one, in which case he would probably mention that risks may be tilted to the downside, the euro would probably see a fresh wave of selling. Alternatively, if he remains positive expressing that growth in the eurozone will improve, the common currency could pare yesterday’s losses.

Earlier at 0800 GMT, Norway Central Bank is also expected to keep interest rates unchanged at 0.75%, while at the same time initial estimates on the German Ifo business climate index will be also closely watched.

Turning to the US, at 1230 GMT durable goods orders are projected to contract by 1.0% m/m in September after reaching an expansion of 4.4% in August, the highest in more than a year. The downfall could be a matter of higher oil prices which probably weighed on transport purchases as the core measure which excludes transportation items is anticipated to rise by 0.5% m/m from 0.0% previously. Surprisingly better results could give early signs that GDP growth figures due on Friday will probably trend up, helping the dollar to gain some strength. Pending home sales for the month of September delivered at 1400 GMT will attract significant interest as well after new home sales released on Wednesday declined sharply, bringing some headwinds to Wall Street. Initial jobless claims for the week ending October 20 will come in public at 1230 GMT.

In equities, Twitter will be among companies to report earnings before the US market open, while Google’s parent Alphabet, Amazon and Intel will issue results after US markets close.

As for today’s public appearances, Fed Vice Chairman Richard Clarida will be speaking on “Outlook for the U.S. Economy and Monetary Policy” before a Peterson Institute for International Economics luncheon, in Washington at 1615 GMT. In Canada, trade ministers will hold a two-day meeting to discuss how to reform World Trade Organisation, while the Japanese Prime Minister will be flying to China today at the invitation of Chinese Premier Li Keqiang.

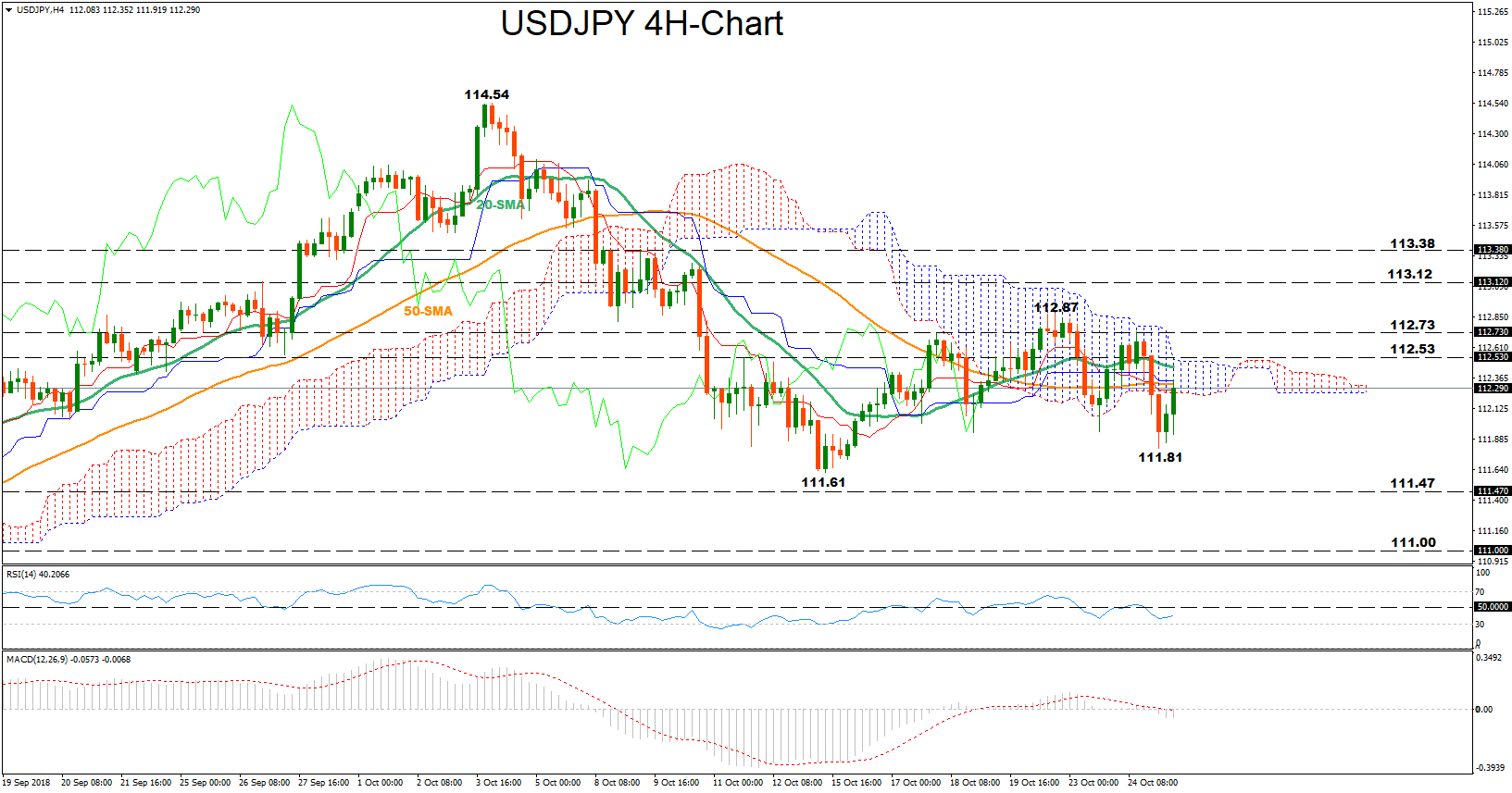

Technical Analysis – USDJPY recoups losses after touching new lows; neutral to bearish in short term

USDJPY slipped to a more than a week low of 111.81 early on Thursday before reversing back above the 112 handle. The RSI in the four-hour chart crossed below its 50 neutral mark but now looks to be changing direction to meet that threshold again, a signal that the market might stretch sideways in the short-term. The MACD though seems to be strengthening to the downside below zero and its red signal line – marginally so – indicating that negative corrections are still possible. In trend signals, the recent downward move from 112.87 may remain in place as the 20-period moving average is heading south to meet the 50-period MA.

However, if US data beat forecasts today, the market could extend its rebound towards 112.53, the high on October 10 and the current top of the Ichimoku cloud. Steeper increases may retest the recent peaks between 112.73 and 112.87, while if these fail to hold too, traders could look for resistance in the 113.12-113.38 area identified by the highs on September 26 and October 9 respectively.

Otherwise, disappointing readings may push the price down to the 111.81 low before the 111.61 trough on October 15 comes into view. A decisive close beneath that bottom would resume this month’s downtrend from 114.54, turning the market from neutral to bearish again. In this case support could run towards 111.47 – a strong barrier during August. If the price manages to pierce that level too, the next stop could be around the 111.00 psychological mark