{kind=link}

Here are the latest developments in global markets:

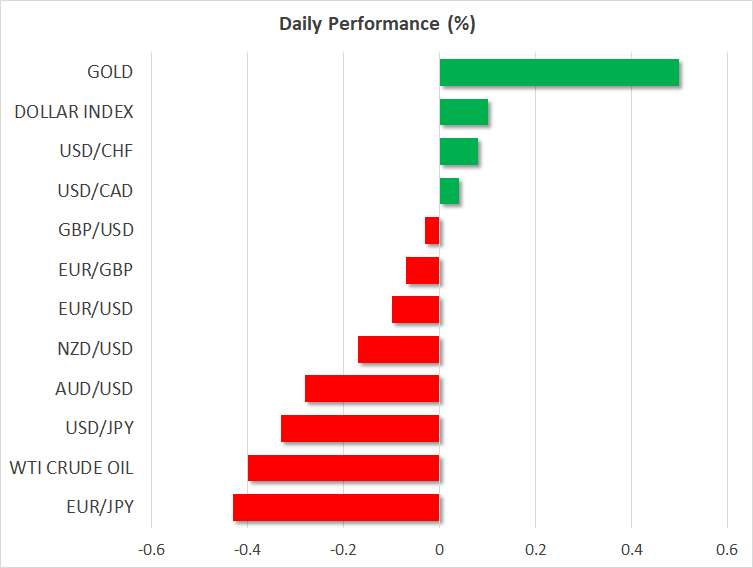

FOREX: The dollar index is higher on Tuesday, albeit by only 0.10%, attempting to extend the gains it recorded yesterday. The yen is reigning supreme among the G10 currencies amid renewed risk aversion, while the antipodeans aussie and kiwi are underperforming. Meanwhile, the pound is consolidating losses from yesterday, and the euro is also retaining a soft undertone amid the poor risk appetite and fading relief in the Italian bond market.

STOCKS: US markets closed mostly in the red on Monday, with the S&P 500 (-0.43%) and Dow Jones (-0.50%) edging lower, but the tech-heavy Nasdaq Composite posting a 0.26% gain. Risk sentiment is not out of the woods yet, and in fact seems to have deteriorated further, as futures tracking the Dow, S&P, and Nasdaq 100 are pointing to a significantly lower open for these indices today, of around -1.0%. Every index in Asia ended lower on Tuesday as well, even though China hinted at further monetary easing. Japan’s Nikkei 225 and Topix dropped by 2.67% and 2.63% respectively, while in Hong Kong, the Hang Seng was down by 2.92%. Europe seems set to follow suit, with all the major indices set to open lower today, futures suggest.

COMMODITIES: Oil edged lower, perhaps pressured by Saudi Arabia’s pledge that it will not reduce its production amid mounting international pressure on the Kingdom over the killing of a journalist. This put to bed, for now at least, speculation that Riyadh may respond to foreign sanctions by “closing the taps”. WTI is down by 0.40% at $68.95 per barrel today, while Brent declined by 0.78% to $79.21/barrel. In precious metals, dollar-denominated gold is up by 0.50% at $1233 per ounce. This is especially encouraging for the bulls considering that the dollar is also higher today, which denotes that safe-haven buying is behind the latest upleg. Technically, a clear break above $1238 could see scope for a test of the $1265 territory.

Major movers: Yen roars back, stocks slump as risk aversion engulfs markets again

Global risk appetite turned sour again on Tuesday, with the safe-haven Japanese yen coming under renewed buying interest and Asian equity indices being a sea of red, in the absence of any major news. In fact, the selloff occurred even though Beijing hinted at a fresh dose of monetary stimulus, on top of the income tax cuts floated earlier. US markets didn’t escape unscathed, with futures tracking major indices like the S&P 500 pointing to a lower open today. Accordingly, risk-sensitive commodity currencies like the aussie and kiwi are both on the back foot, while the dollar has evidently caught a small safe-haven bid, attempting to extend its gains from yesterday.

In terms of potential catalysts, it seems to be another case of the “usual suspects”, ranging from the continuing US-China trade standoff, renewed focus on the Italian budget, bond yields remaining high, and ever-increasing tensions in the Saudi Arabian saga. With regards to trade, it is most interesting that Chinese markets remain in dire straits even after a barrage of promises for fiscal and monetary easing by the authorities. With Beijing looking to shield its economy from the trade fallout through stimulus that takes months to filter into the economy, it is likely signaling it expects this conflict to be a prolonged one and is “digging in” for the long haul, thereby spooking foreign investors instead of soothing them.

Elsewhere, sterling surrendered ground across the board on Monday, after media reports suggested that Northern Ireland’s DUP party – that props up PM May’s administration – will back an amendment proposed by Brexiteers to make the EU’s Irish backstop proposal illegal. The news highlighted the fact that even in case PM May manages to broker a deal with the EU on the Irish border soon, the Brexit drama will be far from over, as she would still need to push any deal through Parliament, which is no easy task.

In euro land, the common currency declined in sympathy to sterling, weighed down by another rout in Italian markets. Italian bond yields edged back up amid a plethora of comments from Italian officials. While the remarks were not aggressive per se, mostly suggesting a compromise can be struck on the deficit, that was evidently not enough to calm investors. The EU Commission is now expected to respond negatively to the budget proposal, and the tone of the reply may be vital in determining the short-term mood in Italian assets and by extent, in the euro.

Day Ahead: EU to decide on Italian budget; Flash Eurozone consumer confidence eyed

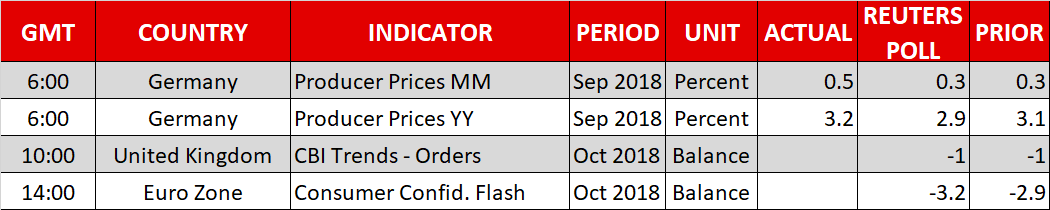

In the Eurozone, the European Commission will give an answer on the 2019 Italian budget which analysts widely expect to be rejected after the aforementioned legislative institute called Italy’s fiscal demands unprecedented as the indebted government aims to lift the public deficit from 1.8% to 2.4% of GDP. On Monday, the Italian Finance Minister backed the draft spending outline but showed willingness to adjust plans in coming years if economic growth stalls, while remaining open to dialogue with the EU. Yet he mentioned that Rome is ready to intervene so that targets are respected, a stance hinting that Italy wont easily step back from its budget goals in coming weeks. Should the EU ask the Italian government to revise its draft budget plan, Rome will have a three-week timeframe to re-submit new ideas. It is worth mentioning that a refusal to comply with EU rules could cost Italy million of euros of fines, though it is highly doubtful the Commission would seek such a confrontational route.

In the FX markets, the euro might not react much as investors have already priced in a no answer from the EU. Yet the common currency could see some fluctuation in the wake of the flash consumer confidence index out of the eurozone. Forecasts are for the index to have declined further in October, retreating from -2.9 to a fresh 1 ½-year low of -3.2. A worse-than-expected outcome could shift funds out of the euro, and vice versa.

Political concerns continue to drive sentiment in the UK as well, as uncertainties around Brexit remain high. Speaking before Parliament on Tuesday, the British Prime Minister reiterated that a Brexit deal is almost done, while saying that the details remaining to be solved are crucial. Still a few months before the UK departures from the EU, May continues to face leadership risks and perhaps even a no-confidence vote today as some members within her party as well as rivals from the Labour party turned more frustrated after May showed willingness to extend the transition period. Besides that, reports that May’s administration could accept an open-ended timeframe for the Irish backstop instead of thefixed-end date previously supported brought further disappointment to Brexiteers.

In oil markets, the American Petroleum Institute will deliver its weekly statement on US crude inventories at 2030 GMT.

In equity markets, Boeing, Caterpillar, Harley Davidson and McDonalds will be among companies to report on earnings before the US open bell.

In terms of public appearances, the economy ministers of Germany, Switzerland, Austria and Liechtenstein will hold their annual meeting in Zurich at 0900 GMT, where questions about the global economy could be of interest. At 1730 GMT Federal Reserve Bank of Atlanta President Raphael Bostic will be commenting on the economic outlook and monetary policy before the Committee of 100, in Baton Rouge, while at 1815 GMT Dallas Fed President Robert Kaplan will be participating in a Q&A session before the Galveston Economic Development Partnership 7th Annual Economic Development Summit, in Galveston, Texas.

Any potential updates regarding the US-Sino trade war could move the markets during the day.

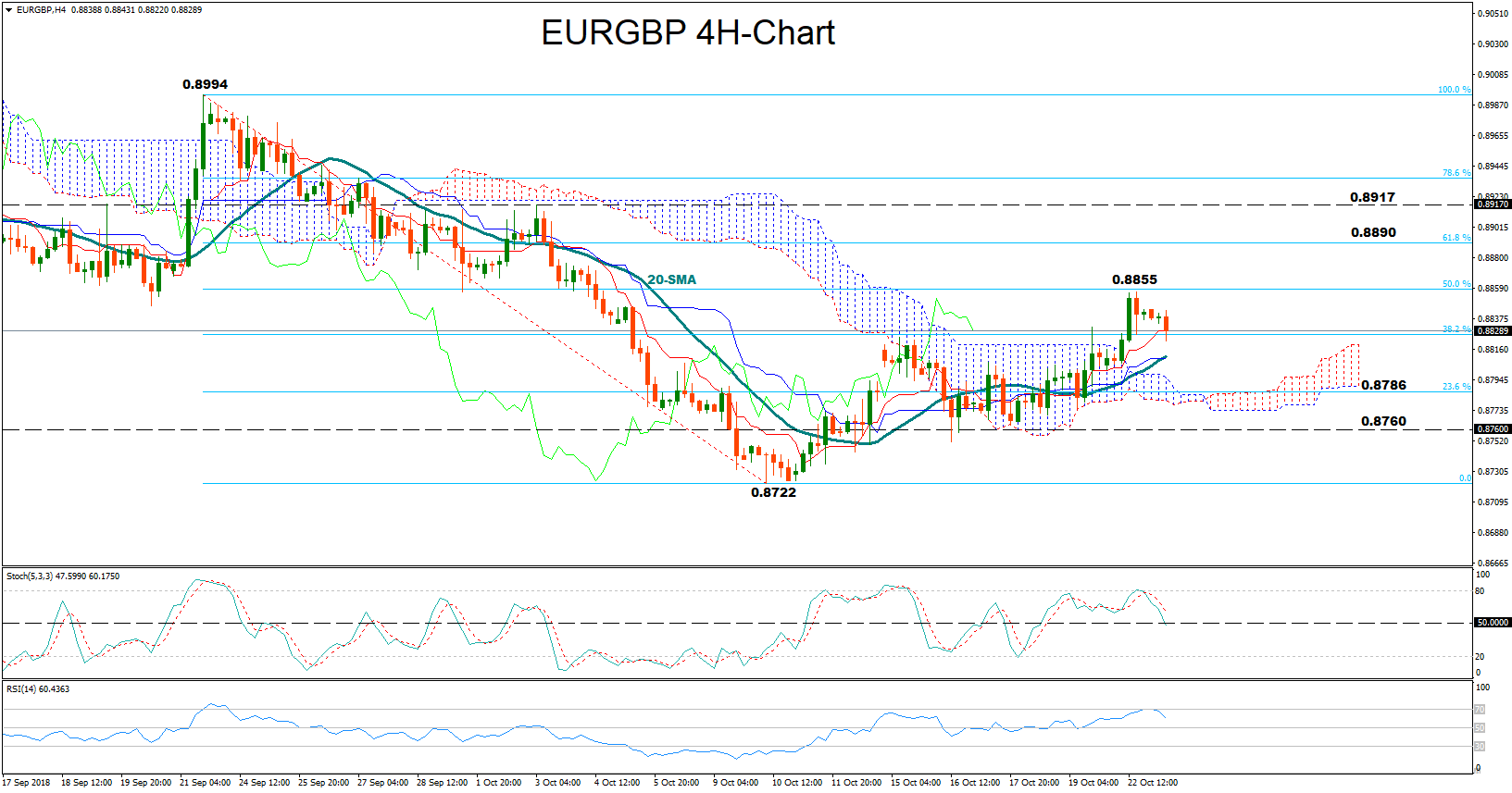

Technical Analysis – EURGBP reaches overbought levels; could move sideways in short-term

EURGBP managed to jump above the Ichimoku cloud early on Tuesday in the four-hour chart, rising as high as 0.8855, the highest in almost three weeks. But the pair failed to sustain gains as both the RSI and the Stochastics touched overbought levels, with the former hitting 70 and the latter posting a bearish cross around 80. The RSI now heads lower towards its 50-neutral mark, hinting that the price might enter consolidation in the short-term.

However if eurozone consumer confidence proves better than projected in October, the pair could reverse higher probably with scope to retest the 0.8855 peak. That is also where the 50% Fibonacci of the downleg from 0.8994 to 0.8722 stands. Above that the focus could shift towards the 61.8% Fibonacci of 0.8890 and the area around 0.8917 where the bulls found some resistance back in September.

Alternatively, a miss in the data could see prices falling towards 0.8810, a previous resistance zone, while slightly lower the 23.6% Fibonacci of 0.8786 could be also another obstacle to have in mind before eyes turn to 0.8760, which acted as support last week. Steeper bearish extensions could open the way towards the 0.8722 bottom.