{kind=link}

Here are the latest developments in global markets:

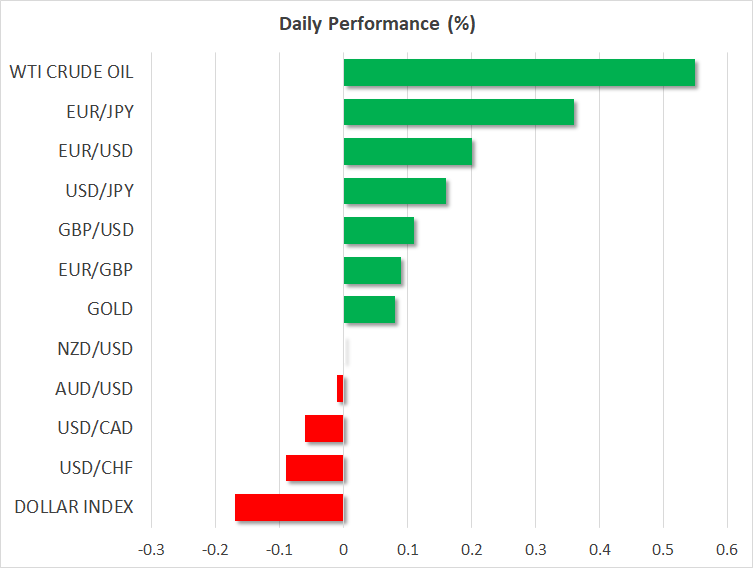

FOREX: The dollar was down by 0.17% against a basket of six major currencies on Monday, extending losses from Friday. Those losses came as the currency with the biggest weight by far in this index – the euro – rebounded, amid encouraging signals that the EU and Italy may manage to avert a full-fledged conflict over budget deficit rules. The British pound edged higher on hints the UK may be softening its Brexit red lines, while the loonie crumbled after a set of disappointing Canadian economic data.

STOCKS: Wall Street closed mixed on Friday, giving back early gains as strong earnings from firms like Procter & Gamble (+8.80%) and PayPal (+9.42%) were eclipsed by another uptick in global bond yields, as tensions between Italy and the EU looked to be fading. The Dow Jones inched higher (+0.26%), the S&P 500 was nearly flat (-0.04%), while the tech-heavy Nasdaq Composite tumbled (-0.48%). That said, sentiment appears to be on a much stronger footing this week, with futures tracking the Dow, S&P, and Nasdaq 100 all pointing to a much higher open today. Accordingly, Asia was mostly in the green on Monday, with gains being led by China, where authorities announced plans to reduce income taxes. China’s CSI 300 is up by 4.32%, while in Hong Kong, the Hang Seng gained 2.29%. European indices were also set to open much higher today, futures suggest, amid a rosier outlook in Italy (see below).

COMMODITIES: Oil was higher on Monday, building on gains from Friday thta came on the back of improving risk sentiment. Earlier today, Saudi Arabia’s energy minister said his nation has no intention of unleashing an oil embargo on Western consumers. He added the Kingdom will isolate oil from politics, alleviating concerns it may use crude production (and by extent prices) as a bargaining chip amid a diplomatic crisis over the death of a Saudi journalist. In precious metals, gold is up by almost 0.10% today at $1227 per ounce, looking set to post its third consecutive session of modest advances.

Major movers: Euro bounces on hopes for Italian compromise; loonie crumbles

The euro posted notable gains in an otherwise quiet session on Friday, following signals that the EU-Italian standoff likely won’t escalate any further, and may instead be settled soon via a negotiated compromise. Specifically, EU Commissioner Moscovici said that the EU will not interfere with Italy’s economic policies, while separate reports suggested Rome is willing to consider lowering its highly controversial 2019 budget deficit target to 2.1% of GDP, from 2.4% previously, in an attempt to appease Brussels.

Most strikingly, the euro is also outperforming on Monday even though Italy’s deputy PM Di Maio poured cold water on hopes for a near-term settlement over the weekend, indicating Rome is definitely not rethinking its deficit target. What’s more, Moody’s also downgraded Italy’s sovereign debt rating on Friday, to one notch above junk status. Yet, both Italian bonds and the euro took the news in their stride, with Italian bond yields declining today across the entire maturity spectrum. Judging by the market moves, investors seen to expect this situation to blow over before too long given the EU’s apparent unwillingness to enforce its fiscal prudence, perhaps paving the way for an even larger relief bounce in the euro. That said, a lot may also depend on how the ECB meeting this week plays out.

In Canada, the loonie gave back some early gains to finish the session lower on the back of disappointing inflation and retail sales data. Interestingly, implied odds for a rate hike by the BoC this week remained stable at 90% according to Canada’s OIS. Hence, markets seem confident these won’t derail the Bank’s near-term plans, but could still lead to a so-called “dovish hike”, where any rate increase is accompanied by cautious commentary – downplaying the prospect of further action in the coming months.

Elsewhere, sterling popped higher on Friday amid reports the UK is ready to ditch one of its a key Brexit demands on the Irish border, in order to break the impasse in the talks. Meanwhile, the safe-haven yen was the worst performer on the day, surrendering ground even against the battered loonie, as the risk aversion that was at play for most of the week gradually dissipated. Risk appetite seems to have improved further this week, most likely aided by news out of China hinting at plans to cut individuals’ income taxes to boost growth.

Day Ahead: Brexit and Italy’s draft spending plans in the center stage; US-Sino trade war in the spotlight

The economic calendar will be lacking important releases on Monday with the Canadian wholesale trade data being the only of interest in major markets. Yet political noise around Brexit and Italy’s fiscal demands are expected to keep investors busy, while the US-Sino trade war will be another area of caution during the week.

On the Brexit front, the UK Prime Minister, Theresa May is scheduled to speak in the Parliament later today probably assuring lawmakers that the Brexit deal is almost complete after last week’s summit left EU leaders deadlocked over mechanisms to avoid a hard border in Northern Ireland. The meeting also follows a report from Bloomberg which revealed during the weekend that May’s administration is set to soften some of its Brexit demands regarding the sticking Irish border point, probably accepting an open-ended timeline for the backstop instead of a fixed end-date strongly supported previously. Yet May might be under severe pressure in the Parliament as some of her Conservative counterparts and some Labour members continue to disagree with her Brexit strategy. Should lawmakers criticize May’s plans once again, erasing optimism that a Brexit agreement is settled, the pound could give up earlier gains.

Meanwhile, investors will be closely monitoring progress on the Italian draft budget plan which the European Commission called non-compliant with the EU rules, while characterizing the deviation from its targets as unprecedented. Markets are now seriously considering that the EU will probably reject Italy’s budget on Tuesday and ask the government for revision. However, the fact that the Italian governing partners managed to end their fights over the budget draft on Saturday, shows that the battle with the EU could intensify in coming days, with the euro probably diving back below the 1.1500 key level.

Elsewhere, China’s willingness to use fiscal relief to mitigate threats from the US trade protectionism after GDP growth figures out of the country eased for the third quarter, signals that Beijing is not ready to give up on the trade war but remain on the defence. This leaves markets wondering whether the nations will turn to negotiations ever soon.

In equities, Ryanair will be among companies to report on earnings before the US bell, while Logitech International will issue results after US markets close.

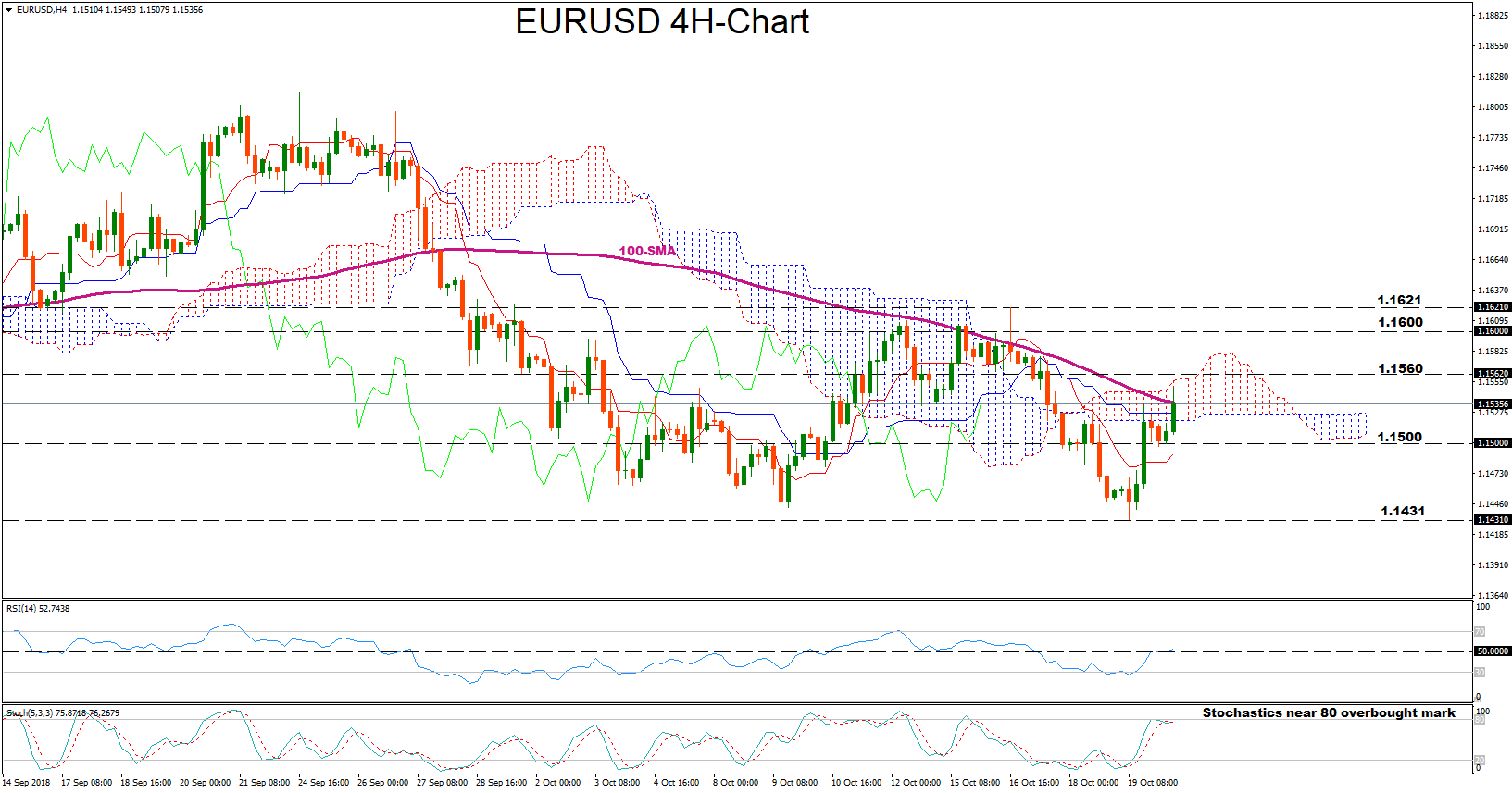

Technical Analysis – EURUSD holds support around 1.1500; negative risks still possible

EURUSD bounced on the 1.1500 round level early on Monday and is currently increasing momentum to increase distance above its 100-period (simple) moving average and surpass the Ichimoku cloud. The RSI is fluctuating around its neutral threshold of 50 supporting that the price might enter consolidation in the short-term, though Stochastics signal that a reversal to the downside in likely as the green %K line and the red %D line are close to the overbought territory.

Should the market weaken, immediate support is expected around 1.1500. Moving lower, the area around 1.1460 could be another obstacle to get through before eyes turn to the 1.1431 bottom.

Alternatively a continuation of the recent rebound could target the area around 1.1562 which has been frequently acting as support in previous weeks. Steeper increases could also challenge resistance between 1.1600 and 1.1621.