{kind=link}

New Zealand inflation data for the third quarter will be made public at 2145 GMT on Monday, probably giving impetus to the Reserve Bank of New Zealand’s hopes that inflation will rise towards the midpoint of its target. The kiwi lost significant ground lately against the greenback, becoming the worst performer among G10 currencies during the past month after aussie. While an upbeat inflation report could give some joy to the local currency if the numbers strengthen more than the markets are pricing in, the reasoning behind, though, could be unsustainable.

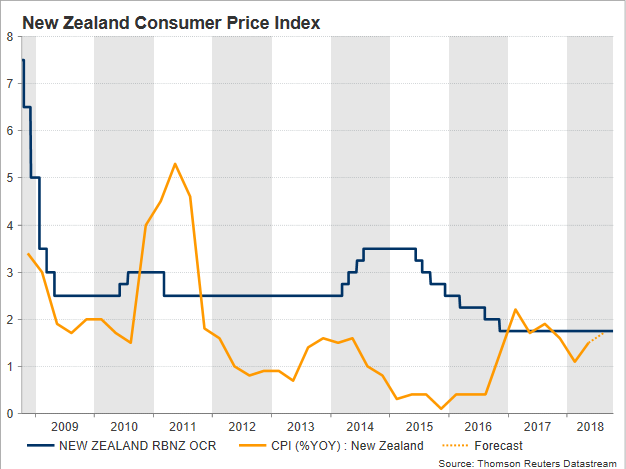

Consumer prices in New Zealand are said to have increased at an annual rate of 1.7% in the three months to September, slightly faster than in the second quarter when house prices pushed headline inflation higher to 1.5%, and much better than the 1.1% growth recorded in the first quarter. On a quarterly basis, upside inflationary pressures are expected to have gained momentum too, with the CPI inching up, from 0.4% to 0.7%. The core measure, though, which washes away volatile items such as food and energy and thus displays a better gauge of the actual inflation trend, decreased for the fourth consecutive quarter in Q2, flagging that the recent pickup in headline CPI might be temporary. Note that crude prices were elevated in the third quarter, with fresh taxes on fuel adding further pressure to New Zealanders’ pockets.

Turning to factors affecting price growth, consumers’ feeling about the economy was downbeat in the third quarter, the Westpac Banking Corporation said, with the corresponding index falling to the lowest in six years. A worrying sign that consumers might spend less in the coming months and therefore retailers might judge wiser to avoid any price rises for now. Yet recent evidence on electronic card retail sales indicated that things are not so bad, with the gauge hitting a one-year high of 6.7% y/y in August before easing to 5.7% in September.

On the supply side, business confidence was in the doldrums according to the Australia and New Zealand Banking Group (ANZ ). Although the measure ticked up in September, it held in negative territory and around 10-year lows, hinting that intentions for investment and hiring are very low, especially under a subdued currency and a risky global trade environment given the US-Sino import tariff game. Increasing wages seem to be another concern for companies as the new coalition government plans to push the minimum hourly wage up from NZ$16.50 this year to NZ$20 in 2021, reducing firms’ profitability.

In the monetary policy front, the RBNZ is positive that pricing pressures will build up and the CPI will gradually rise towards the 2.0% midpoint of its range target. However, policymakers have downgraded GDP growth forecasts for 2019 to 2.6% from 3.1% previously and have messaged that interest rates will remain steady at a record low of 1.75% until 2020, at a time when their US counterparts are ready to hike rates at least four times until 2020. Yet the deadlock in US-Sino trade talks, which will probably last for a while longer as US midterm elections approach, suggests that things could worsen before getting any better. Hence, as this is beyond the government’s control, policymakers judge that monetary policy should remain accommodative, while not ruling out any rate cuts in case the economy shows signs of slowing sharply.

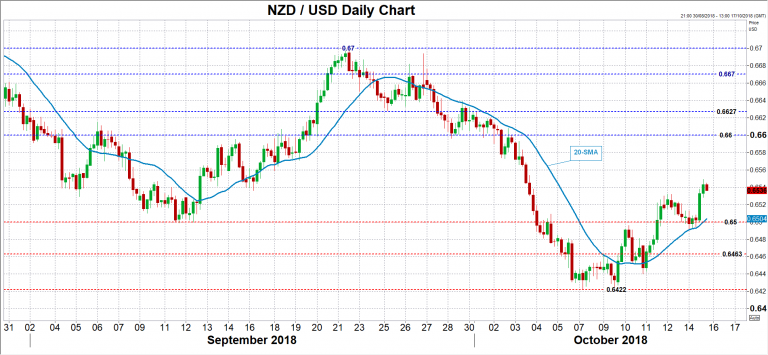

Turning to FX markets, kiwi/dollar has been pushing higher after creating a bottom at a 2 ½-year low of 0.6422, breaking a key resistance around 0.6500 on Thursday. Positive momentum could strengthen towards 0.6600 if inflation on Tuesday beats expectations, while slightly higher the area between 0.6625-0.6670, which halted both upside and downside movements in the past, should gather interest as well. Further above, the focus would shift to the 0.6700 level.

In the alternative scenario if inflation appears disappointingly lower, making rate cuts more likely in the future, the 0.6500 round level where the price strongly rebounded on September 11 and paused once again last Wednesday may stand as a wall to downside corrections. Moving lower, the inside swing high on October 10 could be another level to watch before the 2 ½ -year low of 0.6422 comes into view.