{kind=link}

Here are the latest developments in global markets:

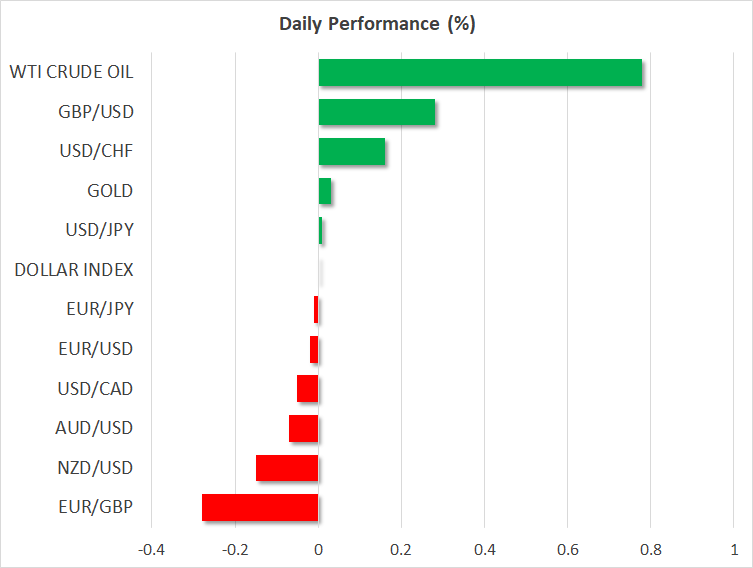

FOREX: The dollar is practically flat against a basket of six major currencies on Friday. It retreated in the previous session, but still held close to its recent highs. The yen saw a round of gains, with dollar/yen falling back below 114.00 as investors turned defensive amid high bond yields, and signs that the US-China “cold war” may be entering a new phase. Meanwhile, the commodity-linked currencies continued to underperform, with the aussie and kiwi touching fresh 2 ½-year lows against the dollar earlier today.

STOCKS: US markets retreated on Thursday as the recent climb in bond yields send shivers across equity markets, and tensions between the US and China seemed ready to heighten further (see below). The tech-heavy Nasdaq Composite (-1.81%) underperformed as the US Vice President hinted at industrial espionage by China, while the S&P 500 (-0.82%) and Dow Jones (-0.75%) were also on the back foot. Sentiment was sour in Asia on Friday as well, with Japan’s Nikkei 225 (-0.80%) and Topix (-0.47%) falling amid a stronger yen, and the Hang Seng in Hong Kong inching lower (-0.14%). Likewise, all major indices in Europe were set to open lower today, according to futures.

COMMODITIES: Oil fell from elevated levels on Thursday as risk appetite took a hit, though the precious liquid managed to recover some of its losses early on Friday. WTI eased to $74.83 per barrel, while Brent tumbled to $85.02, in the absence of any major supply-side news. In precious metals, gold remains stuck near the $1,200 per ounce zone, still moving sideways within a relatively narrow range between $1,180 and $1,213.

Major movers: Risk-off tones dominate as US-China tensions go beyond trade; dollar retreats

The greenback retreated against most of its major peers on Thursday, giving back some of the gains it recorded in recent days, but remaining at relatively elevated levels. There wasn’t any clear catalyst behind the pullback, with investors likely locking in some profits ahead of the highly-unpredictable nonfarm payrolls report today, and of course after six consecutive sessions of advances.

More broadly, risk-off tones dominated in the FX space, as the recent rise in US bond yields sent shivers through equity markets, feeding back into a stronger yen. To explain – rising bond yields are generally considered negative for stocks for two key reasons. First, bonds are considered safer than stocks, and as they begin to offer a higher return they become more attractive to hold relative to equities. Secondly, higher bond yields translate to higher borrowing costs for corporations, potentially disrupting their profitability. Thus, the performance of bond yields may very well prove crucial for the fortunes of stock markets heading into year-end.

Contributing to the risk-aversion, were signs that US-China tensions are heating up further, and crucially not only on the trade front. Earlier this week, US and Chinese warships almost collided in the South China Sea in what was described as a “close encounter”. Yesterday, US Vice President Pence launched a verbal salvo, saying China is trying to sway the outcome of the US midterm elections through propaganda and influence operations. He also warned that Beijing uses “various” means to obtain US intellectual property, accusing China’s security agencies of stealing sensitive US technology, including military blueprints. Tech stocks felt most of the pain, with the tech-heavy Nasdaq Composite declining by 1.81%, likely on the rationale that American policy will move in a direction that disrupts the operations of US firms in China – especially those dealing in cutting-edge technologies.

Risk-sensitive currencies including the loonie, aussie, and kiwi underperformed in this risk-off environment, not least due to a broad-based retreat in commodity prices. All three of these currencies surrendered ground to the dollar, even on a day when the greenback was on the back foot itself. Aussie/dollar and kiwi/dollar touched fresh 2 ½-year lows earlier on Friday.

Elsewhere, the British pound was actually the best performer, as sterling-demand seems to have picked up now that the Conservative party conference is out of the way and Theresa May managed to stave off a mutiny. Today, attention may turn back to the Brexit process, with chief EU negotiator Barnier set to meet politicians from Northern Ireland.

Day ahead: US employment data firmly in focus with Canada’s respective report also eyed

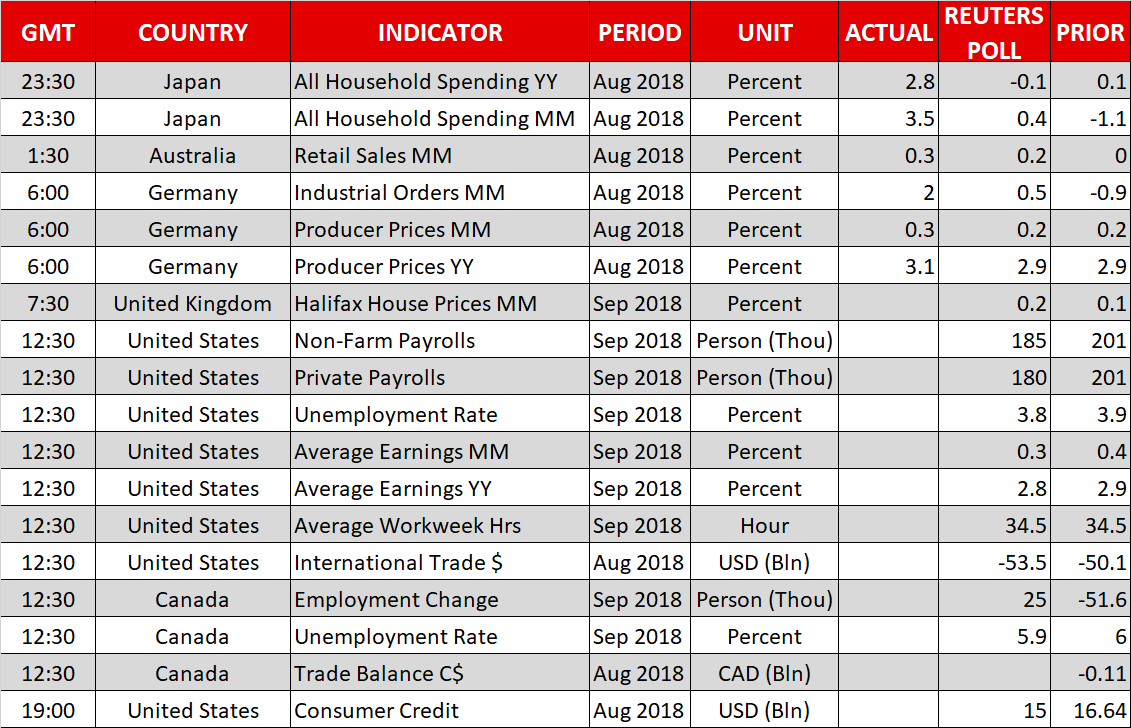

The US monthly jobs report is front and center in terms of data importance on Friday. In the meantime, Canada will be seeing its respective employment numbers hitting the markets as well.

Out of the UK, September house prices as gauged by the Halifax index are due at 0730 GMT. Sterling will yet again be eyeing any Brexit updates though for direction.

The eagerly-awaited US jobs numbers for September are slated for release at 1230 GMT, with an overall healthy nonfarm payrolls report being anticipated. The number of positions added to the economy is predicted to stand at 185k, below August’s 201k but still constituting a robust number. Meanwhile, the unemployment rate is expected to tick down to 3.8%, a number also recorded in May of the current year and way back in April 2000. On the wage growth front, which continues to attract most attention as it can act as an inflation driver, average earnings are anticipated to have grown by 0.3% m/m, below August’s 0.4%. This would put the annual rate of expansion in earnings at 2.8%, weaker than August’s 2.9% which was the biggest annual gain for the measure in more than nine years.

Encouraging numbers, especially on wages, are likely to boost the greenback, stoking expectations for a fourth quarter-percentage point rate increase in 2018. Upbeat releases out of the country this week, including a better-than-expected ADP employment report on positions added to the economy by the private sector, possibly render a beat in the numbers more likely.

Additionally, the reading on August’s US trade balance will be made public at the same time as the NFP report. The relevant deficit is projected to widen to $53.5 billion from $50.1bn in July, which was the highest since February. The politically sensitive trade gap with China that rose to an all-time high in the previously reported month will probably come under the spotlight. Lastly on US releases, data on August’s consumer credit are due at 1900 GMT.

Also out at 1230 GMT will be Canada’s jobs report for September, with employment forecast to bounce back in positive territory during the month. Specifically, the economy is predicted to have added 25.0k positions, after losing 51.6k in August; last month’s headline number is misleading though in the sense that the fall came on the back of a sharp slide in part-time jobs, with full-time ones rising. The unemployment rate is expected to fall to 5.9% from 6.0% in August.

In similar fashion to the US, a beat in the figures has the capacity to stoke expectations for a late October 25bps hike by the Bank of Canada, with the opposite holding true as well; Canadian OIS currently project an 85% probability for such an outcome. Meanwhile, the numbers pertaining to the nation’s trade balance for August will be released at the same time.

ECB Vice President Luis de Guindos will be talking at 1045 GMT, while regional Fed Presidents Kaplan (non-voting FOMC member in 2018) and Bostic (voter) will be making public appearances at 1430 GMT and 1440 GMT respectively.

Elsewhere, US Secretary of State Mike Pompeo will be meeting North Korea’s Kim Jong-Un during the weekend; he will be paying a visit to Japan first to meet PM Shinzo Abe and his Japanese counterpart.

In energy markets, Baker Hughes data on active oil rigs in the US are scheduled for release at 1700 GMT.

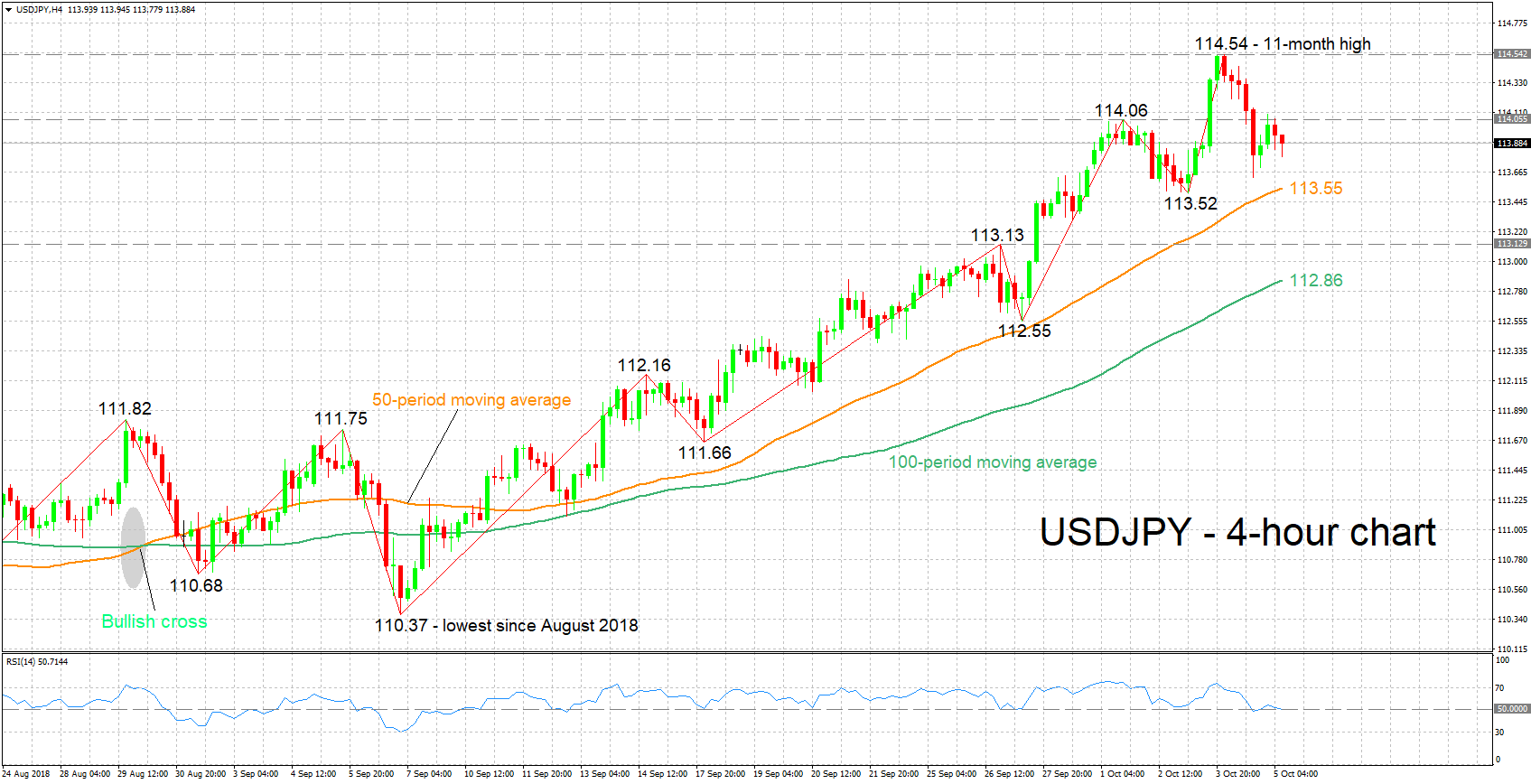

Technical Analysis: USDJPY momentum heads south

USDJPY is trading roughly 70 pips below Thursday’s 11-month high of 114.54. The RSI turned lower after entering overbought zone – signaling a shift in momentum – and is currently hovering around the 50 neutral-perceived level.

Better-than-expected US employment data, especially on wage growth, can push the pair higher. Given a move above 114.06, this being a previous peak, the zone around yesterday’s multi-month high of 114.54 may act as a barrier to the upside. Stronger gains would turn the attention to the 115 handle.

On the downside and in case of a disappointment in the numbers, support may come around the current level of 50-period moving average line at 113.55; the area around this captures a previous bottom at 113.52. Further below, the region around 113.13 – a previous top – and the 100-period MA at 112.86 would be eyed.