{kind=link}

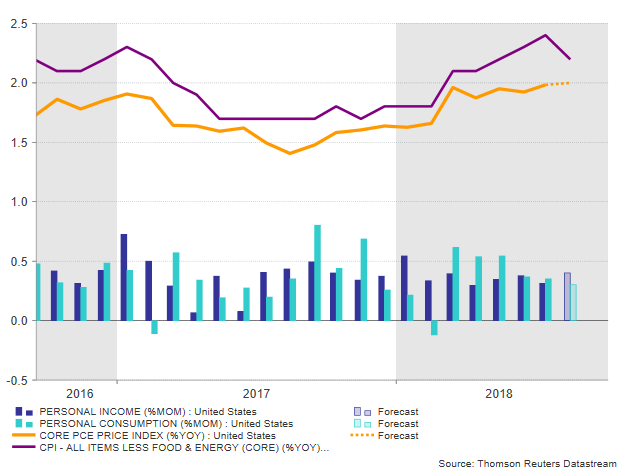

On Friday, the updated core Personal Consumers Expenditure (PCE) price index, the Federal Reserve’s favorite inflation measure, will dominate investors’ attention as economic evidence out of the US and Trump’s restrictive trade policy point to stronger inflation in the coming months. Forecasts, however, support that in August price growth in the US mainland flattened. As usual, personal income and personal consumption readings accompanying the inflation report will gather interest as well given their positive contribution to inflation, but no big changes are foreseen on this front.

According to analysts, the core PCE which excludes the volatile and seasonal components such as food and energy, is expected to arrive at 2.0% year-on-year (y/y) in August, maintaining July’s pace of inflation and thus remaining at the highest level reached since May 2012. On a monthly basis the gauge is said to ease to 0.1% from 0.2% in the preceding month.

Taking into account the Consumer Price Index (CPI) which also gets a lot of press but does not affect monetary decisions, a weakness in inflation cannot be ruled out as the core CPI inflation eased to 2.2% in September after topping at 2.4% in August, the fastest expansion since October 2008. The pullback in CPI was triggered by a sharp decline in apparel prices (-1.6%) and that might weigh on September’s core PCE index too. Decreases in medical costs in August could add pressure to the PCE inflation as well, as the sector constitutes the biggest component in the index.

Yet latest stats out of the labor market suggest that inflation might rather evolve positively in the coming months, a view backed by the FOMC policymakers as well. The government’s Nonfarm Payroll report conducted in August showed that the unemployment rate stuck for the second month at the 18-year low of 3.9%, while average hourly earnings ticked surprisingly higher to 2.9% y/y, marking the largest increase in pay in nine years. Consequently, with consumers and businesses enjoying a tax gift from the US President and new import tariffs on various products (imposed in June and September) increasing costs for US factories, inflation might not take long to pick up steam or at least hold above the Fed’s 2% price goal. A heat up in inflation would then comfortably allow FOMC policymakers to deliver further rate hikes, something the committee already plans as the famous dot plot published on Wednesday at the end of the FOMC policy meeting mirrored another rate hike this year, three more in 2019 and one rate rise in 2020. Recall that FOMC members project inflation to average 2.1% y/y in 2018, while in 2019 they see a pullback to 2.0% before rebounding to 2.1% in the following two years. It is also worth noting that September’s Nonfarm payrolls due next week are expected to say that the unemployment rate inched down to 3.8% and average hourly earnings gained momentum towards 3.0%.

About personal income, analysts believe that the monthly measure bounced from 0.3% to 0.4%, though, they speculate that consumers did not spend more but probably saved more, pushing the monthly personal spending down by 0.1 percentage points to 0.3%.

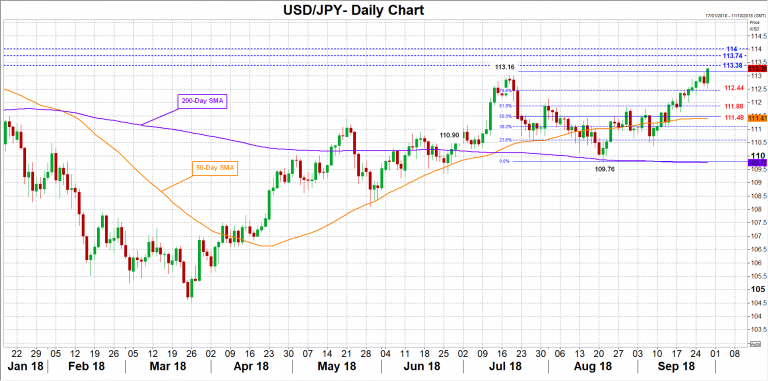

In FX markets, USDJPY managed to pierce the 113 key level on Thursday but softly so. Should the PCE price index and /or personal income and personal consumption readings surprise to the upside on Friday, the market could post further gains. In this case, traders could look for immediate resistance between 113.38 and 113.74, taken from the highs recorded in December 2017 and January 2018. Even higher, bullish actions could meet a wall at 114.00, while the 114.72 top created on November 2017 may come under the radar too.

Alternatively, discouraging figures may lead the pair down to 112.44, the 78.6% Fibonacci of the downleg from 113.16 to 109.76, before attention shifts to the 61.8% Fibonacci of 111.88, which provided some resistance recently. Moving lower, a break below the 50% Fibonacci of 111.48 would put the rally off 109.76 into doubt.