{kind=link}

Here are the latest developments in global markets:

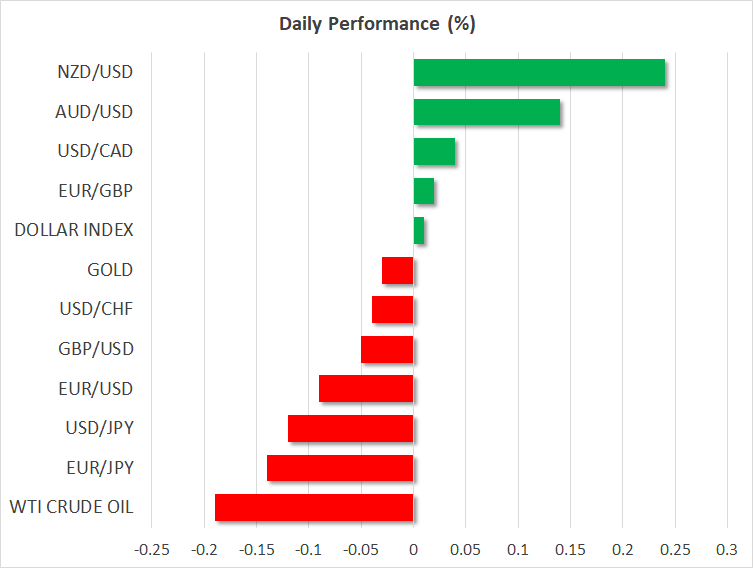

FOREX: The dollar index is practically unchanged on Wednesday (+0.02%), ahead of the Fed decision later today (1800 GMT), where a quarter-point rate increase is seen as a done-deal. The pound moved higher, outperforming its peers amid signs that the EU is finally ready to make concessions on the Irish border. Meanwhile, kiwi/dollar bounced earlier today (+0.23%), with an RBNZ rate decision also being on the menu for today (2100 GMT).

STOCKS: Wall Street closed mostly lower on Tuesday, with the Dow Jones (-0.26%) and S&P 500 (-0.13%) underperforming, though the Nasdaq Composite did manage to eke out some gains (+0.18%). Futures suggest the Dow, S&P, and Nasdaq 100 are all set for a higher open today, though to be fair, the performance of these indices will most likely depend on the Fed meeting later today. A hawkish Fed could prove negative for equities, and vice versa. Asia was generally in the green on Wednesday. In Japan, the Nikkei 225 rose (+0.39%) but the Topix ticked down (-0.04%), while in Hong Kong, the Hang Seng climbed by 1.22%. In Europe, all the major indices were set for a lower open today, according to futures.

COMMODITIES: Oil had a rocky session on Tuesday. Both WTI and Brent rose initially, but retreated a few hours later after the US President took aim at OPEC, calling for lower prices (see below). A larger-than-anticipated build in the API crude inventory data overnight also contributed to the pullback. Today, WTI is down by 0.17% at $72.19 per barrel, while Brent is higher by a marginal 0.09% at $82.03/barrel. In precious metals, gold is nearly flat (-0.04%) at $1,200 per ounce, continuing its unexciting sideways move within the narrow $1,189 – $1,214 range. The dollar-denominated metal could finally see some volatility today on the FOMC decision; recall that the greenback and gold are inversely correlated.

Major movers: Sterling and euro recover; dollar ticks lower ahead of Fed

The British pound was the best performer among the major currencies for a second straight session on Tuesday, buoyed both by monetary policy signals and some encouraging signs around Brexit. Sterling got an initial lift from BoE MPC member Vlieghe, who said his own forecast is for 1-2 rate hikes per year. This was somewhat more hawkish than market pricing, which currently sees the next 25 bps hike being delivered in August 2019 (UK OIS).

Then, media reports suggested EU negotiators are willing to offer the UK a “free-trade area” after Brexit, but contrary to Chequers, there should be a customs border that would involve some “friction” on trade. More importantly, the EU is prepared to make a “special case” of Northern Ireland given its small population and allow it to be one of these free trade areas – though extending this to the entire UK would give it an unfair advantage. While there wasn’t much further detail, the mere fact the EU seems ready to make some concessions on the Irish border issue is encouraging by itself, potentially laying the groundwork for some progress in the coming weeks.

The euro was briefly hammered lower on Tuesday by ECB chief economist Peter Praet, who downplayed the recent confident remarks from Draghi. That said, the single currency managed to recover its losses to close the session higher overall. In the US, consumer confidence as gauged by the CB survey soared to a new 18-year high in September, though the dollar couldn’t capitalize, ending the day lower. Today, all eyes will be on the Fed rate decision (see below).

On the trade front, US top trade official Robert Lighthizer said Canada was not making enough concessions to reach a deal before the October 1 deadline. Meanwhile, Trump took another shot at China in his UN speech, fueling speculation that yet another round of tariffs on the remaining $267bn of Chinese goods may be looming. Speaking about OPEC, the US President said the cartel is “ripping off” the world by elevating oil prices, and that the US won’t put up with this much longer. Oil prices fell modestly as a result. While he did not clarify what the US may do exactly, a potential short-term solution could be releasing the nation’s Strategic Petroleum Reserves.

Overnight, the kiwi spiked higher following the ANZ business confidence survey for September. The index came in at -38.3, still in negative territory but markedly better than the -50.3 recorded previously. The RBNZ is widely expected to remain on hold today (2100 GMT), and it will be interesting to see whether policymakers keep a rate cut on the table.

Day ahead: Fed to hike rates, Bank’s rate guidance eyed; PM May talking Brexit in New York

Undoubtedly, the upcoming decision by the US central bank and specifically its rate guidance is dominating attention out of Wednesday’s calendar. In the meantime, UK PM May’s Brexit comments in New York will also rank high in terms of potential to move FX markets.

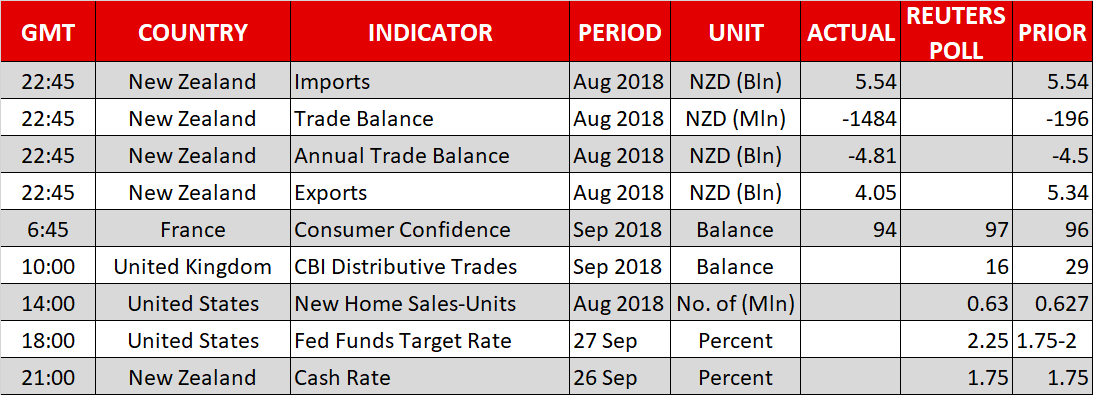

The UK Confederation of British Industry’s distributive trade balance gauging retail sales growth will be hitting the markets at 1000 GMT. The measure is projected to weaken, falling to its lowest since May. Sterling, though, will again be most sensitive to Brexit developments. Relating to this, PM Theresa May will be talking at the Bloomberg Global Business Forum in New York, where she will attempt to “pitch” post-Brexit Britain, among others stressing a low-tax environment in the nation. She will also be meeting US President Donald Trump to discuss Brexit and a bilateral trade deal.

Out of the US, new home sales are anticipated to have increased by 0.5% in August. Sales unexpectedly fell by 1.7% in July to touch a nine-month low, adding to worries that the housing market is slowing down; a rising rate environment is negative for the housing market. The numbers are due at 1400 GMT.

However, all eyes will be on the Federal Reserve’s rate decision which will be made public at 1800 GMT, alongside the FOMC statement and fresh economic projections. The central bank is widely expected to raise rates by 25bps, marking the eighth such increase since late 2015 when it started its rate normalization cycle. As there is virtually no uncertainty surrounding this, the focus will fall on the Bank’s rate outlook as reflected by its dot plot, which shows where Fed policymakers see rates moving forward. Another rate hike is also in large part – around 80% – priced in by year-end, but the outlook for 2019 is not as clear and the dot plot will shed more light on FOMC members’ expectations.

Updated economic forecasts by the central bank will also be closely watched, with any comments on trade and how it may affect the US economy amid the ongoing Sino-US dispute gathering attention as well. Fed chief Jerome Powell will be giving a press conference at 1830 GMT. It is not uncommon for the head of the most influential central bank to share market sensitive remarks.

At 2100 GMT, the Reserve Bank of New Zealand will also be deciding on rates. No change in the Bank’s cash rate is expected, with the focus falling on the central bank’s guidance.

In Italian politics, deliberations for a budget, which must be presented by Thursday, will be generating interest. Reports suggested Italy is willing to make a compromise on this front, which if true, may help the euro as the odds for an Italy-European Commission clash would be seen as decreasing.

ECB chief Mario Draghi will be meeting German President Steinmeier at 1000 GMT, with the two expected to make some short comments. Elsewhere, President Trump will be chairing a UN Security Council meeting on Iran and weapons of mass destruction during the annual gatherings of world leaders at the organization. Trump is also expected to meet Japanese PM Shinzo Abe; the two are anticipated to touch on trade issues.

In energy markets, EIA data on US crude stocks are due at 1430 GMT. A drawdown by around 1.3 million barrels is forecasted for the week ending September 21, following a fall by around 2.1m during the previously tracked week.

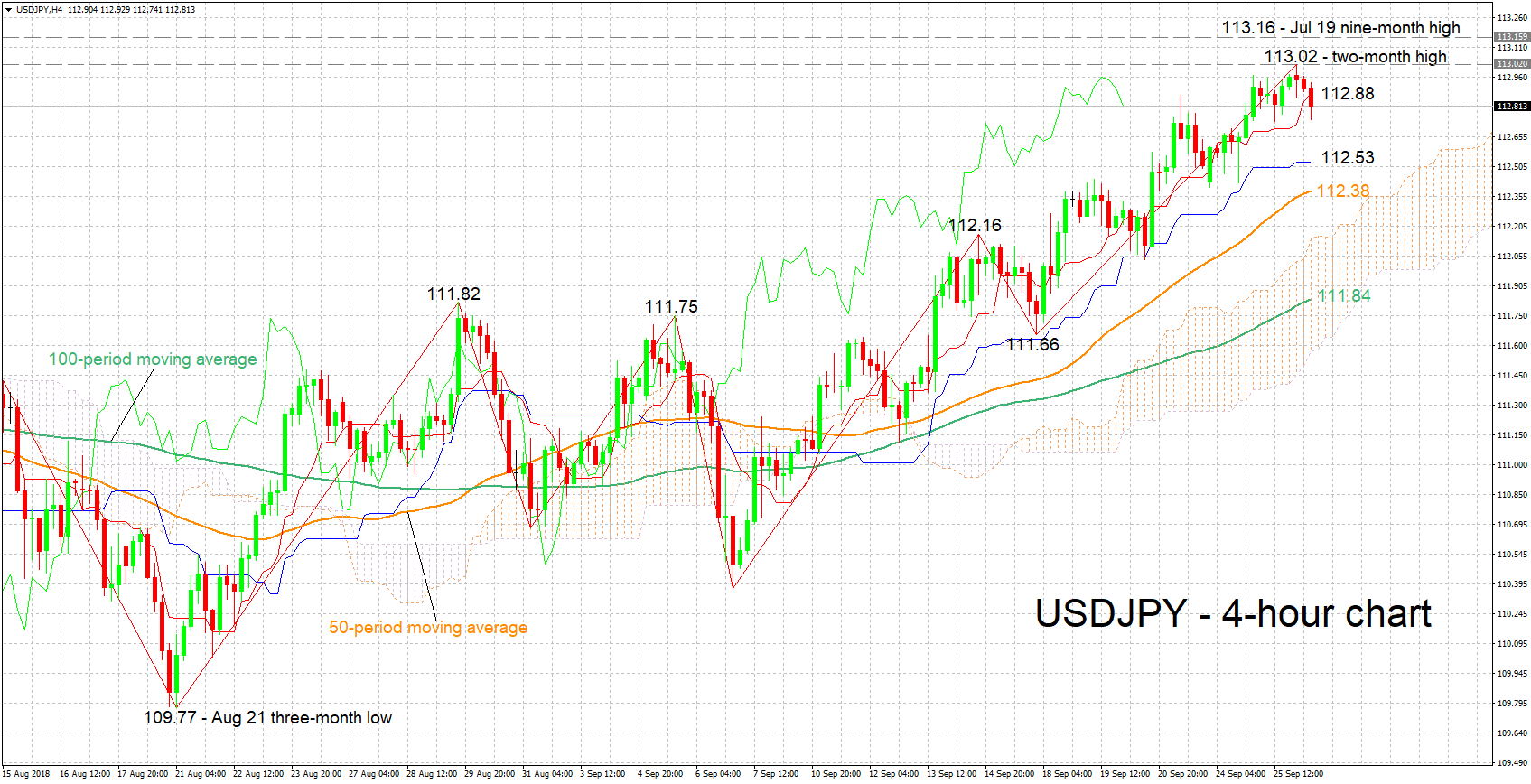

Technical Analysis: USDJPY bullish as it exceeds 113-handle to reach fresh 2-month high; positive momentum may be easing

USDJPY reached a fresh two-month high of 113.02 earlier on Wednesday. It is currently trading roughly 20 pips below that peak. The Tenkan- and Kijun-sen lines are positively aligned, supporting the case for a bullish bias. The latter though has flatlined, the implication being that positive momentum may be easing.

A hawkish Fed relative to market expectations is expected to boost the pair. A move above the Tenkan-sen at 112.88 may meet immediate resistance around the earlier hit high of 113.02, with July’s nine-month high of 113.16 lying not far above at 113.16. Stronger gains would increasingly bring into scope the 114 round figure.

On the downside and in case of a relatively dovish rate outlook by the US central bank or considerable concerns by policymakers about the effects of a deteriorating trade outlook on the US economy, support could occur around the Kijun-sen at 112.53; the current level of the 50-period moving average at 112.38 is in proximity to this point. Steeper losses would turn the attention to the zone around the Ichimoku cloud top at 112.14 and the 100-period MA at 111.84.