{kind=link}

Here are the latest developments in global markets:

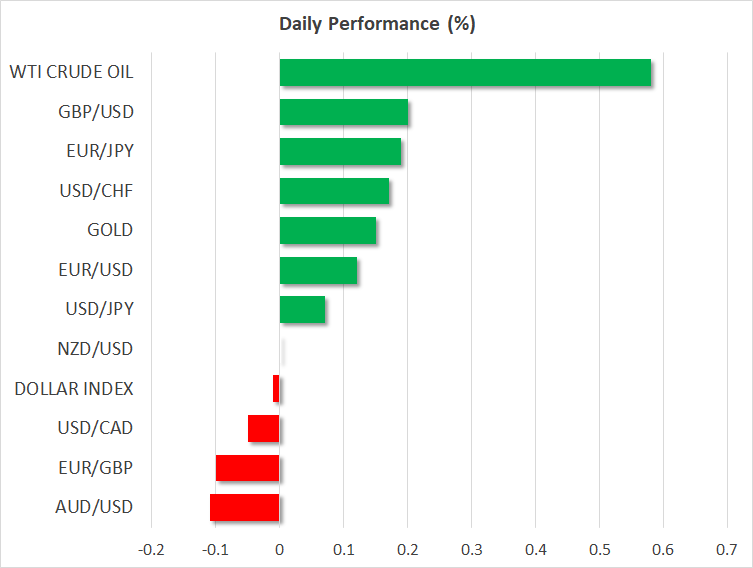

FOREX: The Japanese yen remained under pressure versus the US dollar as the 10-year US government bond yields reached fresh 4 ½-year highs at 3.10%. Dollar/yen returned to 112.88 (+0.08%) after peaking as high as 112.96 early today, the highest since July 19, while the dollar index stood flat at 94.16. Following somewhat dovish comments by the ECB chief economist Peter Praet, euro/dollar dropped to a low of 1.1731 before crawling up to 1.1762 (+0.12%). Praet offset hawkish remarks by the ECB chief Mario Draghi made yesterday, saying today that inflation needs further accommodation before reaching the 2% ECB price target. Note that the eurozone headline CPI arrived at 2.0% y/y in August, though the core equivalent appeared at 1.0%. Flash CPI readings for September are scheduled to come out on Friday. Euro/yen topped at 132.96 before slipping to 132.75 (+0.18%). The pound outperformed its major counterparts, trading higher at 1.3144 (+0.19%) against the dollar and at 148.37 (+0.29%) versus the yen. Against the euro, the pound was also in a better position gaining 0.08%. The upside in the British currency strengthened even further today after the BoE MPC member, Gerjan Vlieghe recommended one or two rate hikes a year assuming that productivity growth and thus wages improve. Still, his view is not much different from the BoE’s gradual rate hike approach. In antipodean currencies, the trade-sensitive aussie/dollar and kiwi/dollar were struggling to recover as escalated trade tensions and particularly China’s refusal to resume trade talks with the US, kept investors cautious in the market. The former was last seen lower at 0.7246 (-0.08%), while the latter hovered around 0.6643 (-0.02%). Dollar/loonie was moving sideways at 1.2952. In emerging markets, dollar/lira changed hands lower at 6.11 (-0.41%). The Turkish lira recouped part of earlier losses in the wake of news that US and Turkish officials will meet this week to discuss the fate of a US pastor on trial in Turkey.

STOCKS: European stocks were in the green at 1050 GMT, with the pan-European STOXX 600 and the blue-chip Euro STOXX 50 trading higher by 0.52% and 0.38% respectively, led by energy and technology. The German DAX 30 rose by 0.34%, the French CAC 40 climbed by 0.36%, and the British FTSE 100 was up by 0.43%. The Italian FTSE MIB was the best performer, gaining 1.35%. In Asia, equities closed mixed, with Japanese indices finishing the session higher and Chinese and South Korean stocks finishing lower. In the US, futures tracking S&P 500, Nasdaq 100 were heading up, pointing to a positive open.

COMMODITIES: Oil prices were in bullish mode for the third consecutive day as OPEC and Russia seemed so far to be rejecting calls from the US to raise output in order to offset supply shortages in Iran, the third largest OPEC producer. Meanwhile, the OPEC Secretary General, Mohammad Barkindo, said during an event in Madrid organized by the Spanish oil and gas company Cepsa that global demand for energy is projected to increase by 33% to 2040. WTI crude surged by 0.60% to $72.51/barrel but stood below the 2 ½ -month high of 72.74 reached yesterday. Brent crude rallied by 1.0% to a 4-year high of 82.20. In precious metals, gold edged up to $1,199.6/ounce (+0.12%), remaining within the range it has traded in sinceAugust 23.

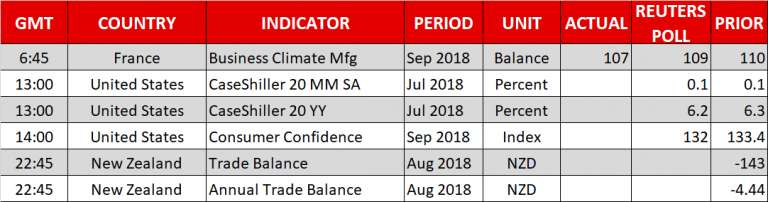

Day Ahead: US consumer confidence the major release ahead of a quiet day; trade negotiations eyed

In a relatively quiet day in terms of data releases, the US CaseShiller house price index and the Conference board consumer confidence index will come under the spotlight. Yet any potential trade headlines could prove of more importance as investors are eagerly waiting to see how far the US and China can stretch their trade dispute. Regarding NAFTA, reports suggest that informal discussions between Canada and the US will take place during the UN meeting in New York on Tuesday. Also, in New York, US President Donald Trump will be having a meeting with Japanese PM Shinzo Abe to discuss trade. Note that Trump considers Japan as his next trade war target.

Out of the US, at 1300 GMT, the CaseShiller indices gauging house prices during the month of July will be made public, while data on consumer confidence for the month of September will be released at 1400 GMT. The consumer confidence index is expected to rise to 132.2 from 133.4 before. Furthermore, the US Federal Reserve’s Federal Open Market Committee (FOMC) starts its two-day meeting on interest rates today, due to make its rate announcement on Wednesday.

In energy markets, investors will be waiting for the API weekly report to show changes in US crude oil inventories at 2030 GMT.

In addition, later in the day, New Zealand trade balance for December is scheduled for release at 2245 GMT.

In terms of public appearances, at 14:40 ECB Board Member Benoit Coeure will be participating at the 3rd ECB Annual Research Conference in Frankfurt.