{kind=link}

Tuesday September 25: Five things the markets are talking about

It’s a return to the drawing board for many investors who are now back online beginning their holiday shortened Asian trading week.

Euro equities are trading mixed following a “get back to basics” Asian session as investors ponder the outlook for global trade and U.S politics.

The U.S dollar continues to hang tough, while stateside, Treasury yields consolidate atop of +3.1% while crude oil trades at a four-year high.

In Europe, Italian bonds rally as the country edges closer to delivering a budget.

Topping investors’ agenda this week is today’s two-day FOMC meeting, along with the Fed’s updated forecasts and the chair’s quarterly press conference (Sep 25-26).

Note: The market is looking for a third +25 bps rate hike and is pricing in another one for December. Investors await Fed chair Powell’s views on trade and tariffs tomorrow.

1. Stocks mixed results

In Japan, the Nikkei rallied for a seventh consecutive session overnight, helped by gains in chip-related stocks that offset weakness in construction equipment manufacturers. The ‘big’ dollar trading through ¥112 also helped to support overall sentiment. The index gained +0.3% to hit its highest print in more than eight-months.

Note: Both Hong Kong and South Korea indexes were closed for holidays on Tuesday.

Down-under, Aussie stocks traded flat overnight as an escalation in Sino-U.S trade tensions hit risk sentiment, while energy stocks rallied on a firmer oil prices. The benchmark dipped -0.1% on Monday.

In China, stock fell on Tuesday in their first trading session after fresh U.S tariffs on +$200B worth of Chinese imports began yesterday. At the close, the Shanghai Composite index was down -0.58%, while the blue-chip CSI300 index was down -1%.

In Europe, in early trade, regional bourses are being supported by stronger commodity prices and optimism over the Italian budget.

U.S stocks are set to open in the ‘black’ (+0.1%).

Indices: Stoxx50 +0.3% at 3,419, FTSE +0.3% at 7,482, DAX +0.2% at 12,373, CAC-40 +0.2% at 5,486, IBEX-35 +0.4% at 9,550, FTSE MIB +0.5% at 21,450, SMI +0.3% at 8,972, S&P 500 Futures +0.1%

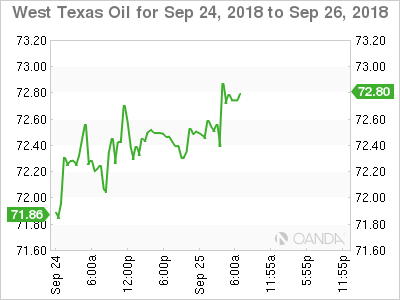

2. Oil hits new four-year highs as OPEC resists output rise, gold steady

Crude oil prices remain better bid after Brent hit a fresh four-year high amid looming U.S sanctions against Iran and an apparent reluctance by OPEC and Russia to raise output to offset the expected hit to supply.

With OPEC and Russia having ignored Trump’s twitter pleas to increase production, coupled with U.S sanctions to hit Iran exports in November, should again provide support for oil ‘bulls’ to seek higher price prints.

Brent crude futures are up +30c, or +0.4% from Monday’s close at +$81.69 a barrel, a level not seen since November 2014. U.S West Texas Intermediate (WTI) crude futures are at +$72.28 a barrel, up +20c or +0.3% from yesterday’s close.

The U.S from Nov. 4 will target Iran’s oil exports with sanctions, and Trump continues to put pressure on governments and companies around the world to fall in line and cut purchases from Tehran.

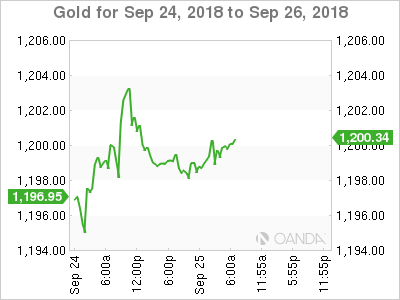

Ahead of the U.S open, gold prices trade steady as the market remains somewhat cautious ahead of today’s two-day U.S Fed meeting, which could offer direction on future interest rate hikes. Spot gold is little changed at +$1,199.06 an ounce. U.S gold futures are also steady at +$1,203.70 an ounce.

Note: Gold has fallen -12% since hitting a peak in April against a backdrop of trade disputes and rising U.S interest rates.

3. Italian yields’ fall on budget hopes, Bund yields rally

Italian borrowing costs rally, narrowing the gap with its German counterparts, on signs that Italy’s coalition is likely to reach a compromise over next years budget. The ruling coalition is willing to keep the budget deficit below +2% of GDP.

In contrast, Germany’s Bund yields continue to back-up, trading atop of their four-month highs, a day after ECB chief Mario Draghi pointed to a “vigorous” pick-up in underlying inflation.

In early trade, Italy’s 10-year BTP yield has fallen -9 bps to +2.86%, narrowing the spread over the benchmark German Bund yield to around +232 bps, from around +245 bps late yesterday.

In Germany, the 10-year bund yields has rallied to a four-month high at +0.54%, a day after posting their biggest one-day jump since June.

Elsewhere, the yield on 10-year Treasuries has advanced +1 bps to +3.09%, its highest yield in almost 19-weeks. In the U.K, the 10-year Gilt yield has climbed +1 bps to +1.624%, , the highest in more than seven months.

4. Bitcoin’s pullback quickens

In early trade, BTC has slid to new intraday lows, falling nearly -4% to +$6,400 in the overnight session, moving the cryptocurrency back toward this month’s lows. The BTC ‘bears’ continue to eye the +$6,000 region.

TRY has rallied +6% in the past 24-hrs to $6.1374 on reports that Turkish authorities are sending signals that an American pastor facing terrorism charges could be released next month.

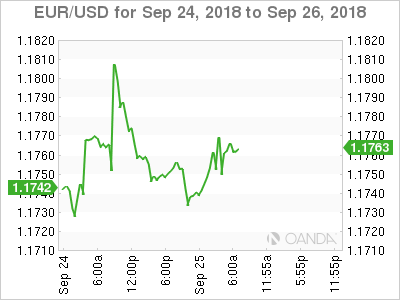

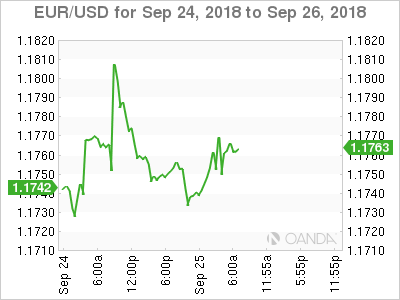

EUR/USD (€1.1762) softened slightly after comments from ECB’s Praet noting that comments from Draghi yesterday were nothing new. The pair fell -30 pips to a low of €1.7133 following the comments.

Note: The ‘single unit’ found support yesterday after ECB President Draghi said there has been a relatively vigorous pick-up in inflation.

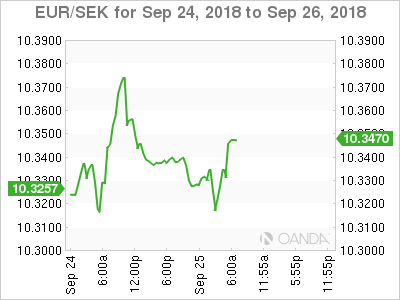

5. Swedish PM Lofven ousted in no-confidence vote

Earlier this morning, Swedish PM Stefan Lofven lost a no-confidence vote in parliament and will step down after four-years in power, but with neither major political bloc holding a majority it remained unclear who will form the next government.

Note: Voters delivered a hung parliament in the Sept. 9 election with Lofven’s center-left bloc garnering 144 seats, one more than the center-right opposition Alliance.

SEK is down -0.18% at €10.3374.