{kind=link}

Here are the latest developments in global markets:

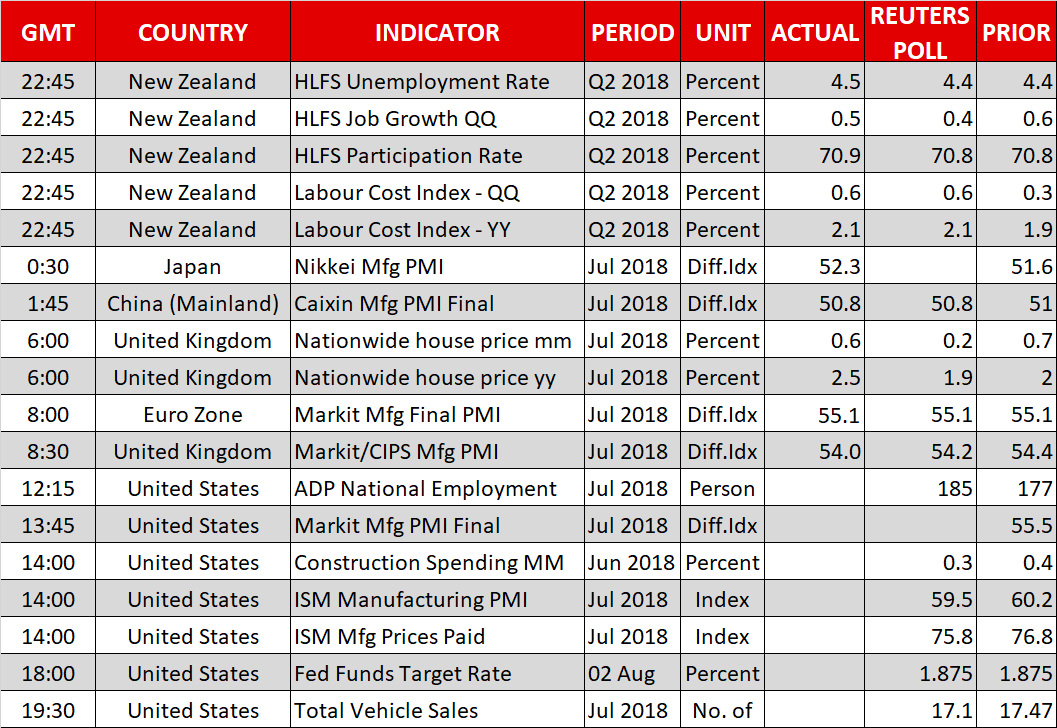

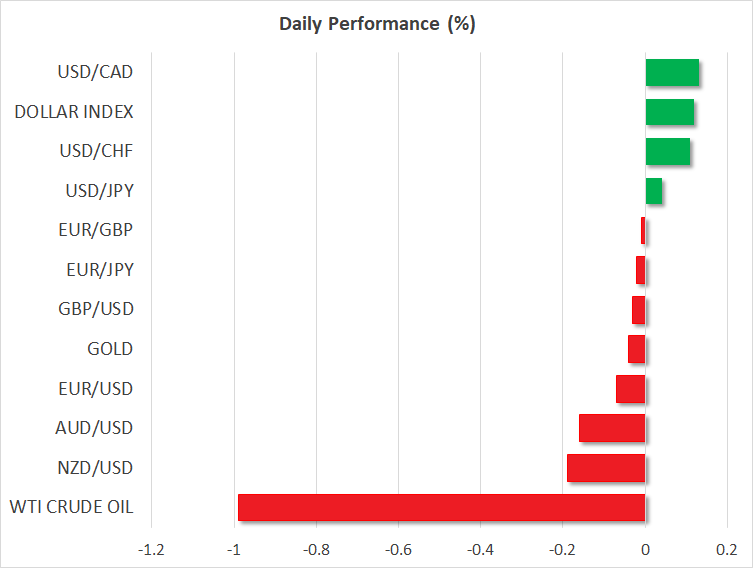

FOREX: The US dollar continued the bullish movement today against the Japanese yen (+0.05%), near 112.00, while tariffs returned to the spotlight as the US and China were reportedly seeking to resume talks to find common ground on trade. The main event of the day will be the FOMC monetary policy decision later in the day. In the Eurozone, the final IHS Markit manufacturing PMI posted a reading of 55.1 in July, unchanged from the flash estimate, while the German manufacturing PMI came in at 56.9 in July, slightly below a preliminary reading of 57.3. Euro/dollar slipped by 0.06% after the data, falling below the 1.1700 handle. Pound/dollar declined by 0.05% after the UK’s IHS Markit manufacturing PMI fell to a 3-month low of 54.0 in July from a downwardly revised 54.3 in the previous month, and below market expectations of 54.2. Meanwhile, sterling awaits the Bank of England’s rate hike tomorrow, which is almost fully priced in. In the antipodean sphere, aussie/dollar and kiwi/dollar moved lower by 0.23% on a report that the US administration will propose raising its planned tariffs on $200 billion Chinese imports to 25%, from the 10% rumored previously. Dollar/loonie pared some of its previous days’ losses, gaining 0.12%.

STOCKS: Major European benchmarks traded lower for the most part. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 dropped by 0.28% and 0.17% respectively. The German DAX 30 slipped by 0.26%, while the Italian FTSE MIB declined by 0.31%. UK’s FTSE saw a stronger loss of 1.00% and the French CAC 40 declined by 0.05%. In Asia, equities were mixed, while in the US, futures tracking stock indices were pointing to a negative open.

COMMODITIES: Oil prices plummeted on Thursday on the back of a stronger dollar and signs of US-China trade tensions. WTI crude oil tumbled by 1.03% and fell near the $68 level, while Brent plunged by 1.02% to $73.45. In precious metals, gold prices fell by 0.08%, flirting with the $1,222 level.

Day ahead: Fed meeting front and center; trade tensions in the spotlight too

The main event today will be the Fed policy decision at 1800 GMT. No change in interest rates is expected, and since this is one of the “smaller” meetings that do not include updated economic forecasts or a press conference, markets will focus solely on any tweaks in the phrasing of the accompanying statement. Considering the strength of the US economy in Q2 – with the preliminary GDP estimate coming in at a 4.1% annualized pace – and that inflation as measured by the core PCE index is just shy of the Fed’s 2% target, a broadly hawkish message appears to be in store.

At the time of writing, markets have fully factored in another 25bps rate hike before the end of the year, while they also assign a 69% probability for a second one, Fed funds futures suggest. Should an upbeat statement push the market-implied probability for a second hike higher, the dollar could benefit. The key risk to this view would be some mention to trade tensions posing downside risks to business investment and the broader economy, though this seems quite unlikely to be included in the statement.

A few hours before the Fed, two key US data points for July could impact price action in the dollar: the ADP employment report at 1215 GMT and the ISM manufacturing PMI at 1400 GMT. The ADP is forecast to show that the private sector added 185k jobs, more than the 177k in June. The ISM print, meanwhile, is projected to decline to 59.5 from 60.2 previously. While this would signal a slowdown in the sector, the index is still expected to remain at a very healthy level, consistent with strong expansion – anything above 50 indicates growth.

Turning to trade, recent reports suggest the US is considering imposing “heavier” tariffs on China to ramp up the pressure. Specifically, the 10% tariffs on $200bn worth of Chinese imports may be raised to 25%. Reportedly, such an announcement could come as soon as today, and if so, it is likely to be viewed as a fresh escalation in tensions, potentially weighing on risk sentiment and risk-sensitive assets – like stocks.

In energy markets, the weekly EIA crude inventory data at 1430 GMT are likely to attract attention. Stockpiles are anticipated to fall by 2.8mn barrels, after declining by 6.15mn in the previous week.

In equities, Tesla will be among the companies releasing quarterly earnings results after the US market close today.