{kind=link}

Data on US personal income and spending is not anticipated to attract the usual level of attention on Tuesday (due at 12:30 GMT) as the June figures were already incorporated in last week’s robust GDP stats. The focus will therefore be on core PCE inflation, which the Fed puts the most emphasis on when setting monetary policy. That is not to say that another solid set of numbers tomorrow would not be positive for the US dollar, helping it gain some upside momentum after losing steam earlier this month.

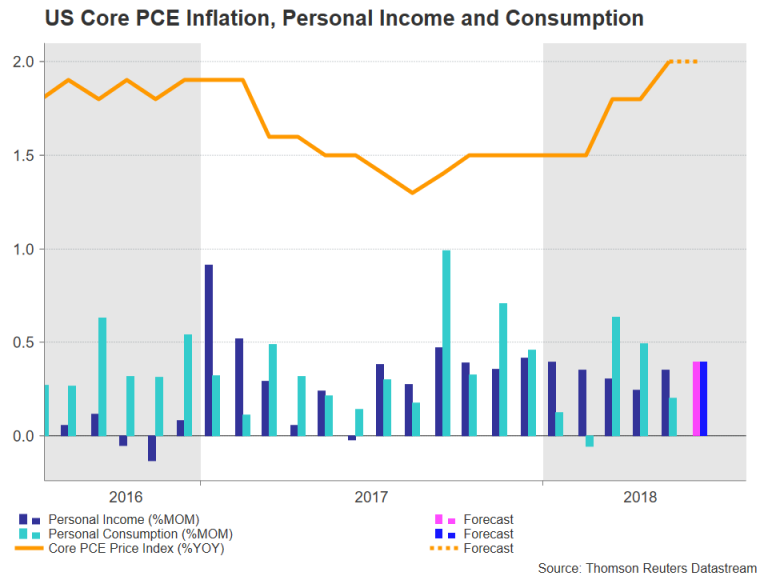

Personal income, which has been growing at a modest but steady pace since the middle of 2017, is forecast to continue this trend in June, rising by 0.4% month-on-month, unchanged from the prior month. Personal consumption is also expected to expand by 0.4% m/m, accelerating from the 0.2% rate seen in May. Strong consumer spending was one of the biggest contributors to the GDP surge in the second quarter and a solid end to the quarter could signal a continuation of this strength going into the third quarter.

Turning to the Fed’s preferred inflation indicator, the core personal consumption expenditures (PCE) price index is projected to remain at 2% year-on-year in June. It hit the Fed’s objective of 2% only in May for the first time in six years. But as the Fed has been stressing its ‘symmetric’ target in recent meetings, the possibility of core PCE inflation moving slightly above 2% in the coming months is unlikely to prompt the Fed to quicken its pace of rate increases.

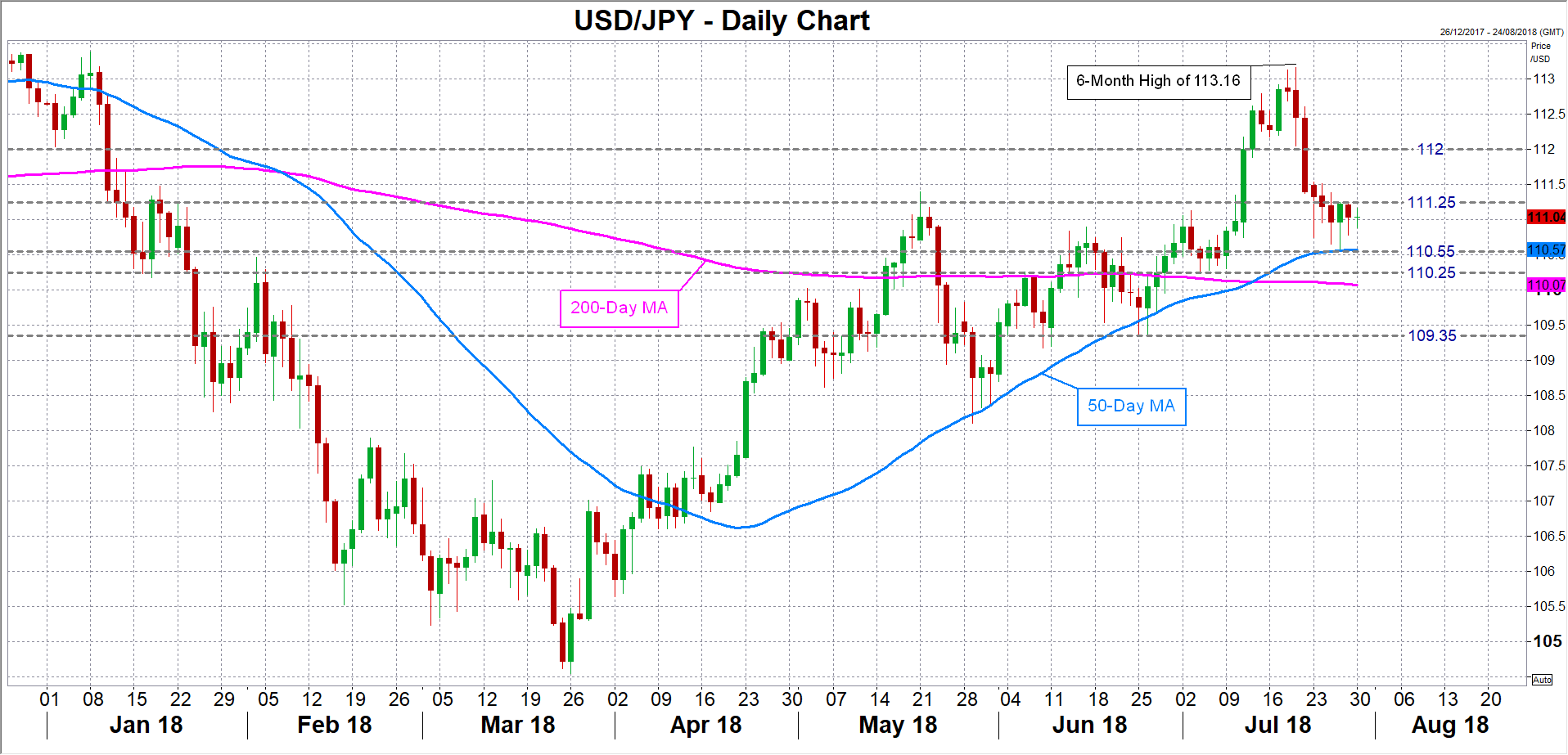

Nevertheless, if there is an upside surprise in the PCE readings, the dollar could receive a much-needed lift, particularly versus the Japanese yen, which the pair has been trading sideways for much of the past week. A push higher could see dollar/yen meeting immediate resistance around 111.25, which it failed to overcome late last week. A break above this level would turn the focus to the 112 handle (a previous support and resistance point), which it needs to overcome if it is to challenge its July top of 113.16.

Should any positive surprises fail to prevent the dollar from resuming its slide, or in the event of some data misses, the 50-day moving average (MA) would likely provide immediate support at around the 110.55 level. A breach of the 50-day MA would increase the risk to the downside, with the next support coming at 110.25, followed by the 109.35 region.

Also to keep in mind prior to Tuesday’s releases are the latest FOMC decision on Wednesday when the Fed concludes its two-day policy meeting, and the July nonfarm payrolls report on Friday. Traders are unlikely to place large bets ahead of those big risk events.