{kind=link}

Here are the latest developments in global markets:

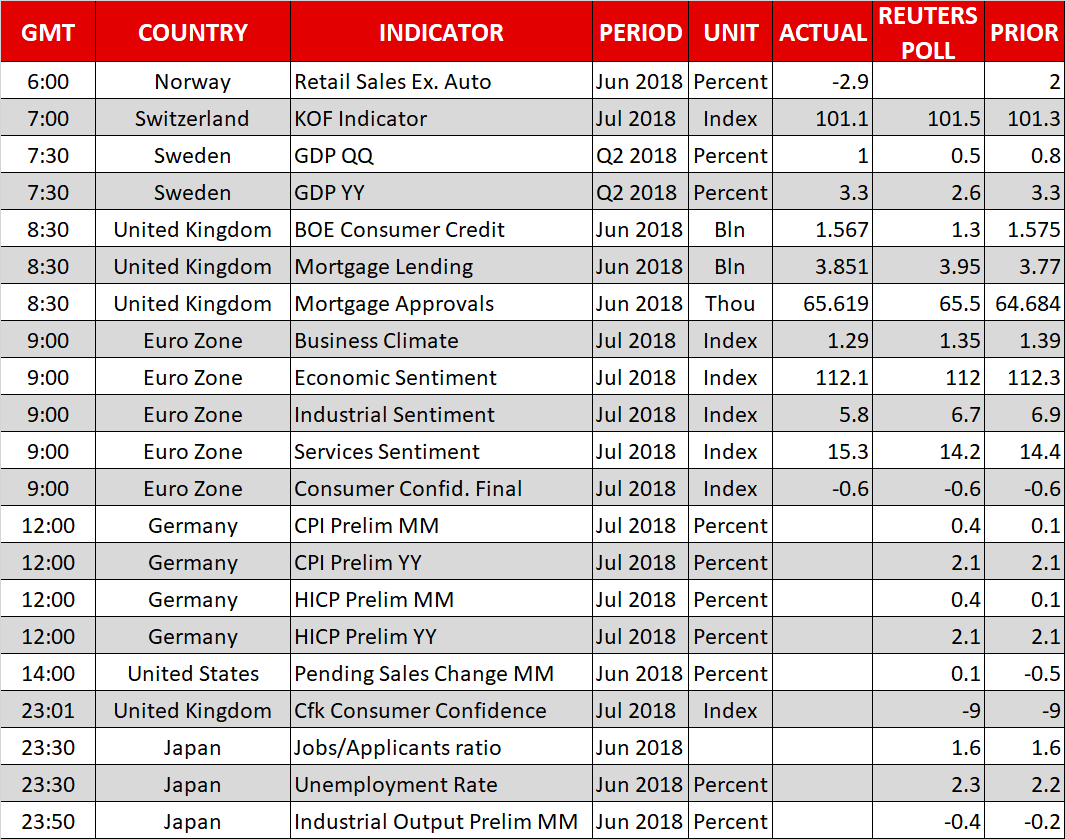

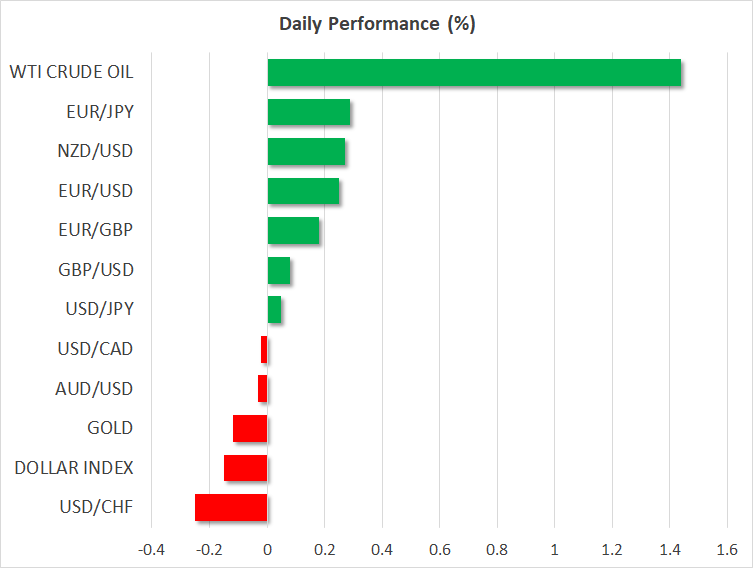

FOREX: The dollar index, which gauges the greenback against a basket of six major currencies, was trading lower by around 0.2%, with euro/dollar being up by roughly the same proportion and trading around 20 pips below the 1.17 handle. The reaction to business and consumer confidence surveys out of the eurozone was minimal, with the focus being on German inflation figures which may act as the preamble to tomorrow’s respective numbers out of the eurozone. Dollar/yen was close to flat and not far above the 111 level, with the immediate focus being on the outcome of the Bank of Japan’s meeting due on Tuesday. Pound/dollar traded marginally higher at 1.3111; the Bank of England meeting on Thursday is eyed, with Brexit uncertainty remaining in the background. Meanwhile, the Swedish krona was elevated on better-than-anticipated Q2 GDP figures out of Sweden; USDSEK was down by 0.9% and EURSEK lower by 0.7% at 1110 GMT.

STOCKS: Major European benchmarks traded lower for the most part, though their losses were limited in magnitude. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 were down by 0.2% and 0.3% respectively. Meanwhile, the UK’s FTSE 100, German DAX and the French CAC 40 were trading lower by 0.1%, 0.2% and 0.25% correspondingly. Some disappointment on the earnings front, in conjunction with negative sentiment on the back of considerable losses from big US tech stocks on Friday, acted as the catalysts for the decline in European equities. In US stocks, futures tracking the Dow were up by 0.1%, those on the S&P 500 were marginally lower, while contracts on the tech-heavy Nasdaq 100 traded down by 0.1%. Caterpillar’s earnings are expected soon; before Wall Street’s opening bell.

COMMODITIES: WTI oil was supported on the back of a draft proposal to scale back on US automobile efficiency requirements that has the potential to boost fuel consumption. The benchmark was last up by 1.4% at $69.70 per barrel. Meanwhile, Brent crude was trading higher by 0.7% at $74.79 a barrel. In precious metals, gold was little changed at $1,222.46 per ounce, trading not far above its lows for the year, at roughly $1,211.

Day ahead: German inflation coming up; US pending home sales also due; Bank of Japan in focus

Important releases as the day unfolds will be the advance estimates of German inflation for July. Meanwhile, pending home sales data out of the US will attract some interest, while Tuesday’s Asian calendar will be a busy one, featuring among others the much-awaited outcome of the Bank of Japan’s latest policy meeting.

July’s preliminary inflation data out of Germany, the eurozone’s largest economy, are due at 1200 GMT. Inflationary pressures as gauged by the consumer price index (CPI) are anticipated to grow by 0.4% m/m, reflecting an acceleration compared to June’s 0.1%. In yearly terms, CPI is forecast to expand by 2.1% y/y, the same pace as in June. The Harmonised Index of Consumer Prices (HICP), that uses a common methodology across EU countries, will also be generating interest.

It is of note that the abovementioned figures are coming one day ahead of the eurozone’s corresponding numbers and may thus be seen as giving an indication as far as tomorrow’s release is concerned; in other words, euro pairs may prove sensitive to the German prints. Meanwhile, flash Q2 GDP growth numbers for the eurozone, as well as June’s unemployment rate, will be released alongside euro area inflation readings on Tuesday at 0900 GMT.

Out of the US, pending home sales are slated for release at 1400 GMT; sales are expected to increase by 0.1% m/m in June, after declining by 0.5% in May.

US Secretary of State Mike Pompeo, Commerce Secretary Wilbur Ross and Energy Secretary Rick Perry will be speaking at the Indo-Pacific Business Forum at 1230 GMT. In the meantime, President Trump is scheduled to meet Italian PM Guiseppe Conte at the White House.

Tuesday’s Asian session will be rather packed, including household spending numbers, industrial production figures, as well as data on employment (and unemployment) out of Japan. China will be on the receiving end of readings on manufacturing and services PMI, while business confidence and building approval prints are due out of New Zealand and Australia respectively.

However, the Bank of Japan’s meeting on monetary policy, which is to be concluded tomorrow, is attracting the lion’s share of attention out of Asia. Since around mid-July, the yen has benefitted on the back of growing speculation that the Japanese central bank will adjust its monetary policy framework in a manner that is supportive of a stronger yen. Should this indeed materialize, then the currency is likely to post further gains. It should be kept in mind though, that economic releases that include subdued inflation and weak household spending, are not lending credence to a hawkish tilt by the BoJ. Should the Bank not deliver to the somewhat “hawkish positioning” by markets, then the yen may be in for a sharp sell-off.