{kind=link}

Here are the latest developments in global markets:

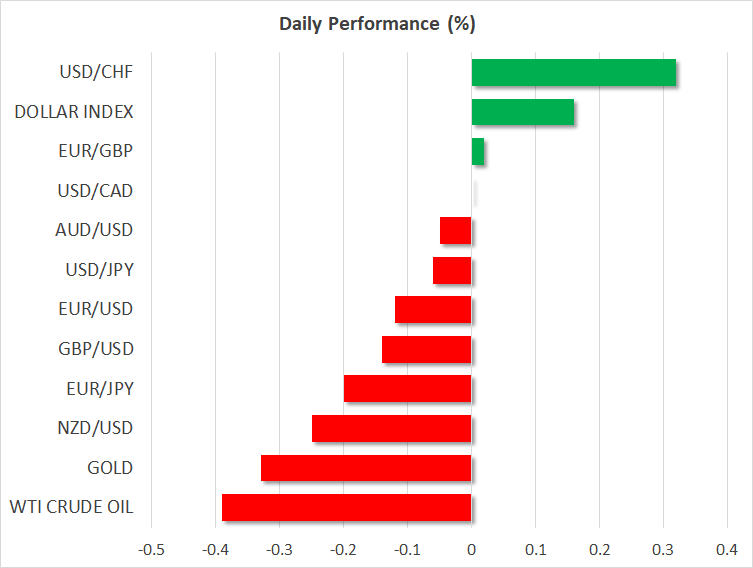

FOREX: The dollar’s index against a basket of six major currencies was trading higher – though by less than 0.2% – building on Thursday’s notable rise. Dollar/yen was little changed ahead of the US report on Q2 GDP and with market participants eagerly awaiting to see whether the Bank of Japan will indeed tweak its policy framework when it completes its meeting on monetary policy on Tuesday. Euro/dollar was 0.1% down, extending the losses which acted as the catalyst for the dollar index’s gains yesterday after the ECB reiterated what markets seem to interpret as a relatively dovish rate-normalization guidance. Specifically, the pair traded at 1.1628 at 1014 GMT, not far above a one-week low of 1.1619 hit earlier in the day. Pound/dollar was 0.15% lower, with concerns over the progress of Brexit negotiations overshadowing optimism relating to the likely delivery of a 25bps rate increase by the Bank of England next week.

STOCKS: European equities were broadly in the green, with overall upbeat corporate earnings and the continuing positive sentiment following the Trump-Juncker meeting on Wednesday contributing to the rise. The pan-European STOXX 600 and the blue-chip euro STOXX 50 were up by 0.3% and 0.5% respectively. Meanwhile, the UK’s FTSE 100, German DAX and the French CAC 40 traded higher by 0.55%, 0.4% and 0.2% correspondingly. Some of these benchmarks may have also received a boost from the sliding euro and sterling versus the dollar, given their heavy export dependency. Turning to the US, futures markets were pointing to a marginally higher open for the Dow and the S&P 500 and an even higher open for the Nasdaq 100; contracts tracking the latter were up by 0.3%. Chevron, Exxon Mobil, Merck & Co and Twitter are expected to soon release their quarterly results; they’re all due before Wall Street’s opening bell.

COMMODITIES: WTI was 0.4% lower at $69.35 per barrel, erasing part of the gains which came after an attack on Saudi tankers spurred supply concerns, consequently boosting prices. Brent crude was down by the same proportion, trading at $74.24 a barrel. In precious metals, gold extended yesterday’s losses on the back of a stronger dollar. It was last down by 0.3% at $1,218.90 per ounce.

Day ahead: US GDP in the spotlight

All eyes will be on the preliminary estimate of US GDP growth for the second quarter of the year due at 1230 GMT.

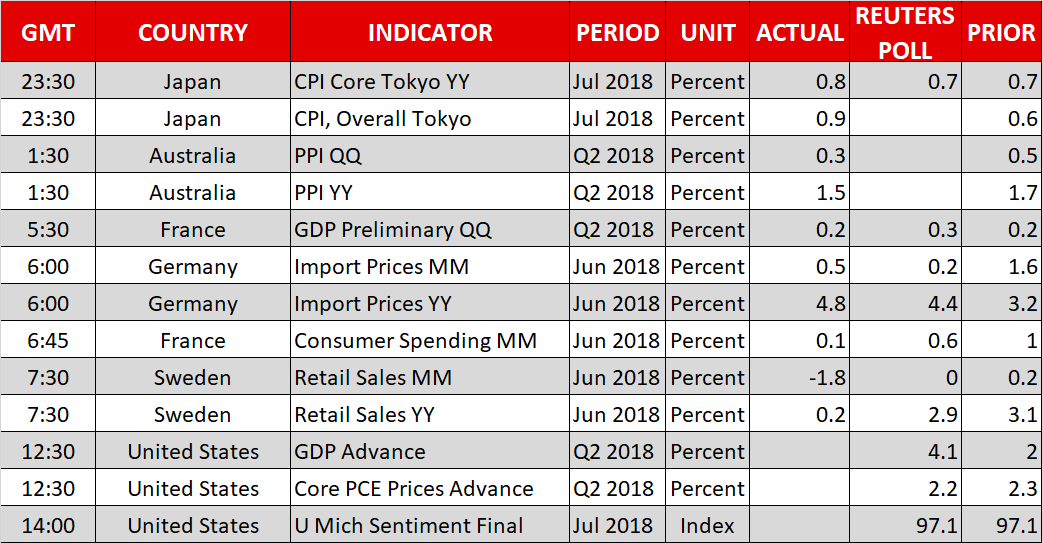

US economic growth is expected to have risen by 4.1% on an annualized basis in Q2, at a far higher pace relative to Q1’s 2.0% and at its quickest since Q3 2014. A better-than-expected reading is likely to be seen as more conclusively putting on the table two more 25 bps rate hikes by the Fed as the year unfolds – bringing the total number for the year to four –, thus supporting the dollar. A weak reading could on the other hand cause some profit-taking for the greenback. At the moment, Fed funds futures project that market participants have fully priced in an additional rate increase, while they see a 68% probability for a second one. In the meantime, advance data on core PCE prices for Q2 will be released alongside the numbers on GDP, while the University of Michigan’s final reading on consumer sentiment for the month of July will be hitting the markets at 1400 GMT; the relevant index is expected to be confirmed at 97.1, below June’s 98.2.

Mexican Economy Minister Ildefonso Guajardo’s visit to Washington, which included meetings with US Trade Representative Robert Lighthizer, will conclude today. Following constructive talks on trade between the US and the EU earlier this week, it will be interesting to see if positive momentum carries through into NAFTA talks, something which is likely to benefit the Mexican peso and the Canadian dollar.

In energy markets, oil traders will be keeping an eye on the Baker Hughes count of active US oil rigs due at 1700 GMT.