{kind=link}

Here are the latest developments in global markets:

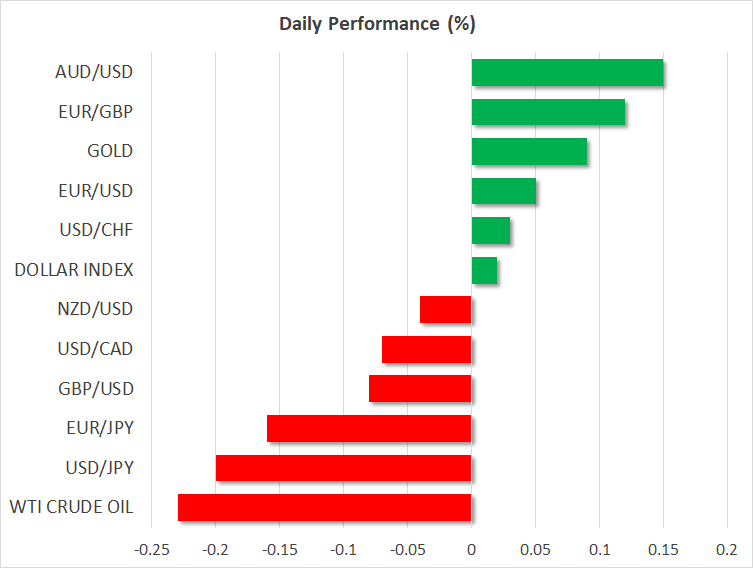

FOREX: The US dollar index – which tracks the greenback’s performance against a basket of six major currencies – was practically unchanged on Friday, after it posted considerable gains in the previous session. The surge came as the currency with the heaviest weight in that index by far – the euro – tumbled following the ECB policy meeting.

STOCKS: US markets closed mixed yesterday, as an 18.96% plunge in Facebook’s share dragged down the tech-heavy Nasdaq Composite (-1.01%) and to a lesser extent the S&P 500 (-0.30%). The Dow Jones, meanwhile, managed to gain 0.44%, as Facebook is not a constituent stock in that index. Futures suggest the Dow, S&P, and Nasdaq 100 are set to open higher today, albeit not significantly so. Asia was mixed as well, with both of the major Japanese indices – the Nikkei 225 and the Topix –advancing, but the Hang Seng in Hong Kong dropping marginally. European benchmarks were set to open higher across the board today, according to futures.

COMMODITIES: Oil prices were somewhat lower on Friday, with WTI and Brent dropping by 0.23% and 0.11% respectively, both giving back some of the gains they posted yesterday. News that Saudi Arabia halted shipments of crude through a shipping lane in the Red Sea kept a floor under prices. Interestingly, there was little market reaction to reports in Australian press overnight that the US is prepared to bomb Iran’s nuclear facilities, perhaps as early as next month. In precious metals, gold is up by a marginal 0.08% on Friday, hovering just above the $1,244 per ounce mark. The dollar-denominated yellow metal dropped notably yesterday as the US currency regained some ground.

Major movers: Draghi ‘keeps options open’, euro drops

All eyes were on the ECB meeting yesterday, which even though did not provide much new in the way of forward guidance, still managed to generate a decent reaction in the euro. The single currency initially spiked a little higher as President Draghi’s press conference got underway, after he noted the Bank remains confident on the inflation outlook amid a pick-up in wage growth. However, the euro soon gave back all its gains to trade lower overall, after the ECB chief said markets had understood correctly the message that interest rates will remain unchanged at least ‘through the summer’ of 2019.

He implied that current market pricing was close to where it should be, which investors took as a dovish signal. Draghi was essentially applauding the fact there is some uncertainty involved with current pricing, highlighting that the Bank wants to keep its options open with regards to the timing of the first hike. The probability for a 10bps rate increase in September 2019 was around 70% prior to the meeting, EONIA swaps suggested. It dropped to 58% in the aftermath.

The dollar managed to pare all the losses it had posted earlier in the day to trade much higher, drawing strength both from the tumble in the euro and from another uptick in longer-term US Treasury yields. The 10-year US bond yield touched 2.97%, rendering the greenback more attractive from a relative rates perspective, amid speculation for a strong US GDP print for Q2, due out later today.

Meanwhile, yen bulls remain in the driver’s seat, with the Japanese currency trading a little higher against the dollar, euro, and pound on Friday. The theme that the Bank of Japan may make hawkish adjustments to its ultra-loose policy framework as early as at next week’s policy meeting remains at the forefront.

In emerging markets, the Turkish lira took another hit yesterday, after US President Trump tweeted his nation ‘will impose large sanctions on Turkey’ unless it freed an American pastor that has been detained for nearly two years on terrorism charges.

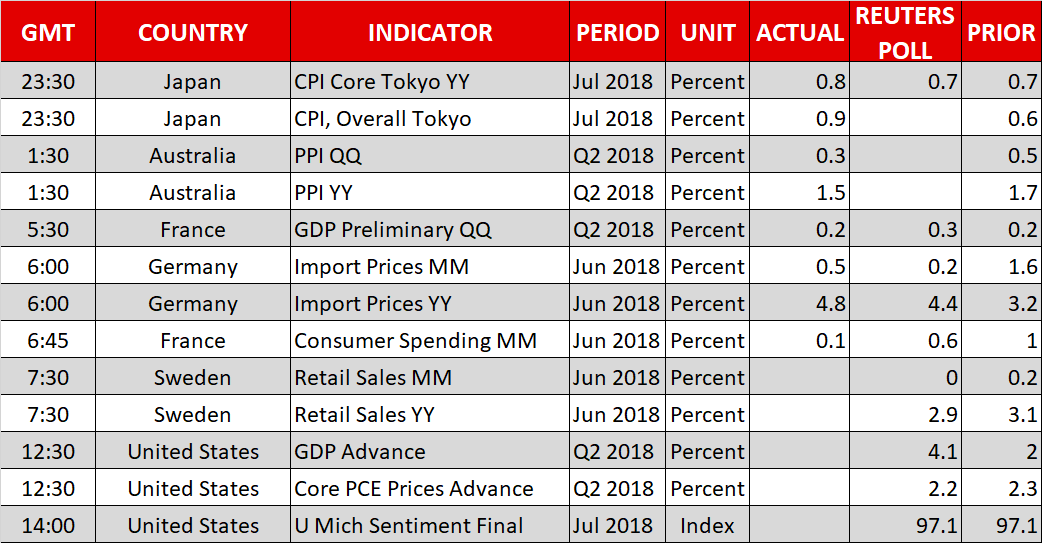

Day ahead: US GDP firmly in focus

The advance estimate of US GDP growth for the second quarter of the year is undoubtedly the highlight out of Friday’s calendar.

Retail sales data out of Sweden are due at 0730 GMT, bringing krona pairs to the fore.

The initial estimate of US GDP growth during Q2 will be made public at 1230 GMT. The economy is expected to have expanded by 4.1% on an annualized basis, a far higher pace relative to Q1’s 2.0% and at its highest since Q3 2014. Fed funds futures currently project that market participants have fully priced in an additional rate hike by the US central bank in 2018, while they assign a 66% probability for a second one. A more upbeat reading than forecasted is likely to push those odds even higher, consequently boosting the greenback; the opposite holds true as well. Meanwhile, advance data on core PCE prices for Q2 will be released alongside numbers on economic growth.

Also out of the US will be the University of Michigan’s final survey on consumer sentiment for the month of July; the relevant reading is expected to be confirmed at 97.1, below June’s 98.2.

Mexican Economy Minister Ildefonso Guajardo’s visit to Washington will conclude today, with any updates on the future of NAFTA to be closely watched.

In equities, Chevron, Exxon Mobil, Merck & Co and Twitter will be releasing quarterly earnings on Friday.

Oil traders will be keeping an eye on the Baker Hughes count of active US oil rigs due at 1700 GMT.

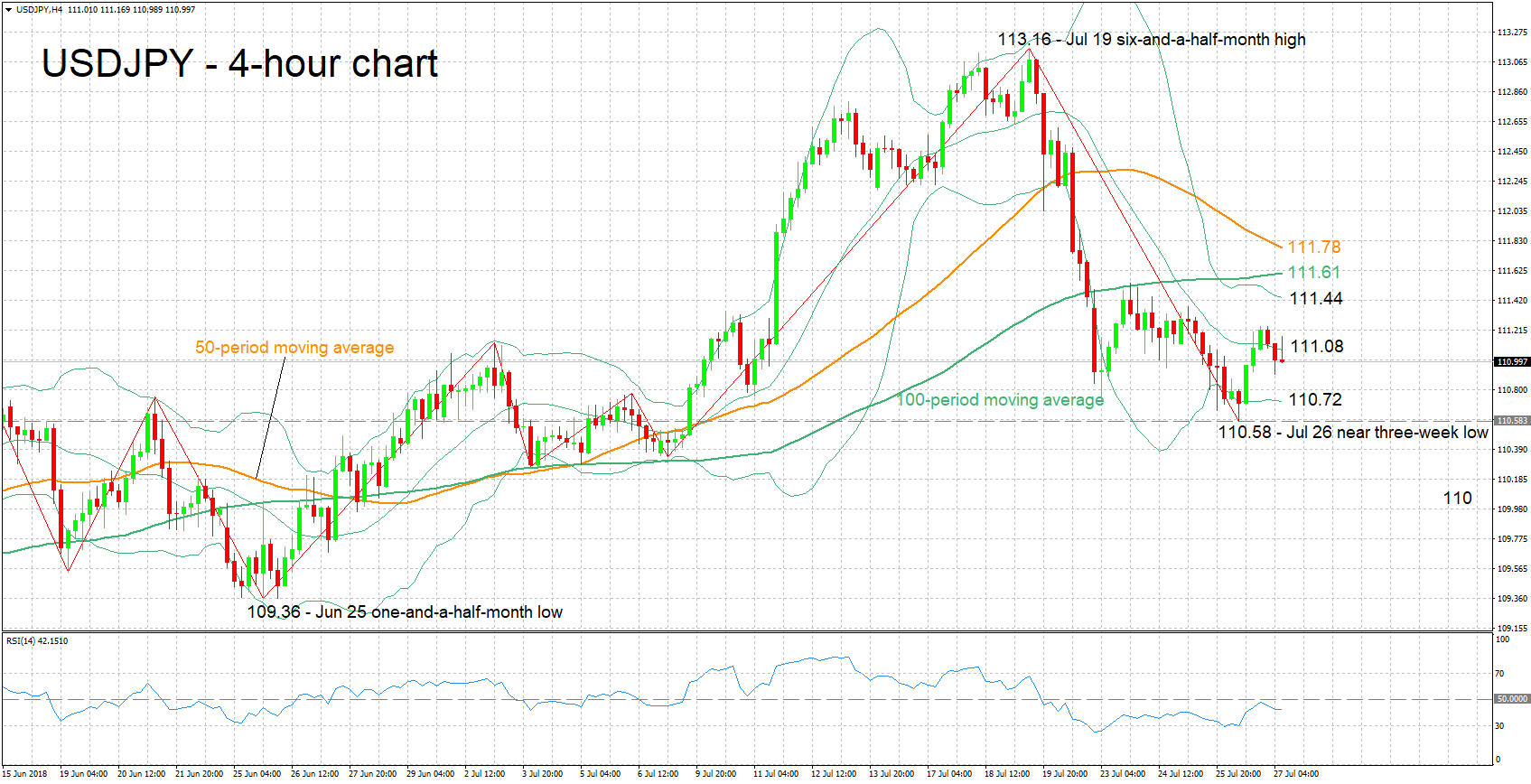

Technical Analysis: USDJPY looking neutral in the short-term

USDJPY has eased after a previous rise from a near three-week low of 110.58 touched on Thursday. The RSI is moving sideways at the moment, projecting a neutral picture in the short-term.

A better-than-anticipated GDP reading out of the US is likely to boost the pair. Given a break above the middle Bollinger line (a 20-period moving average line) at 111.08, the pair may next meet resistance from the region around the upper Bollinger band at 111.44. Notice that the current levels of the 100- and 50-period moving average lines lie not far above, at 111.61 and 111.78 respectively.

On the downside and in case of a data miss, support may come from the area around the lower Bollinger band at 110.72, which also encapsulates yesterday’s near three-week low of 110.58. Steeper losses would increasingly bring into scope the 110 round figure.