{kind=link}

Here are the latest developments in global markets:

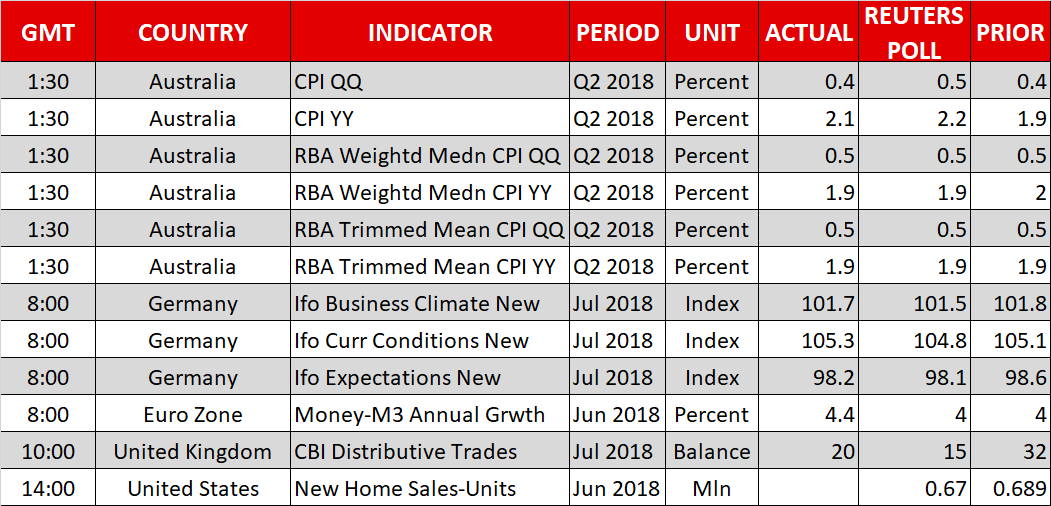

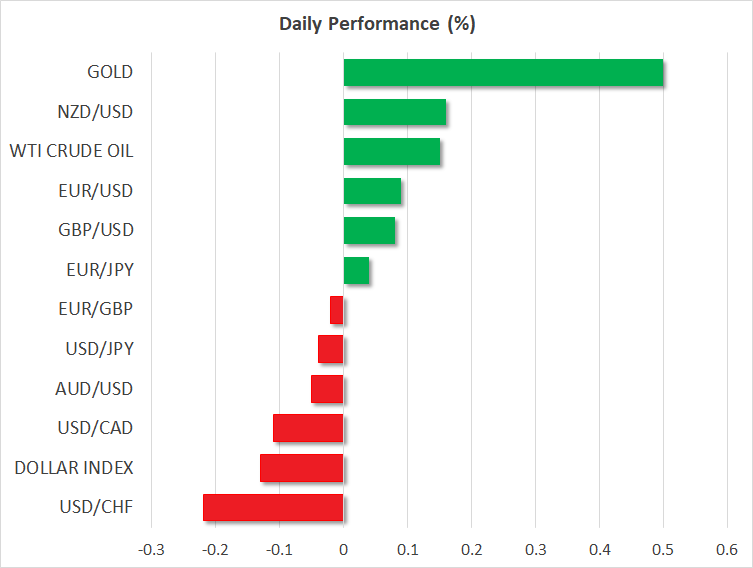

FOREX: The greenback and the single European currency barely moved on Wednesday before a meeting between US President Donald Trump and European Commission President Jean-Claude Juncker. The talks come after the US imposed tariffs on EU steel and aluminum and Trump’s recent threats to extend those measures to EU-made cars. Dollar/yen continued the bearish movement and slipped by 0.05% near 111.14, while euro/dollar jumped slightly above 1.1700 (+0.08%). The US dollar index dropped by 0.13% to 94.48. Furthermore, pound/dollar edged higher by 0.11% as Prime Minister Theresa May took control of Brexit talks yesterday. Overnight, aussie/dollar came under selling pressure after the release of Australia’s CPI data for Q2, which were a touch softer than projected. The pair managed to recover most of its losses during the European session and is currently down only by 0.05%, while kiwi/dollar advanced by 0.16%. Finally, dollar/loonie traded down by 0.10% to 1.3140.

STOCKS: European shares traded mixed on Wednesday after a green session in Asia, however, trade tensions are still in focus ahead of a meeting between Trump and Junker later in the day. The pan-European STOXX 600 moved lower by 0.04% as investors digested mixed earnings from Deutsche Bank and Banco Santander. The blue-chip Euro STOXX 50 opened lower by 0.24%, while the German DAX 30 retreated by 0.23%. The French CAC 40 gained 0.08%, while the Italian FTSE MIB 100 declined by 0.15%. The British FTSE 100 was in negative territory as well, losing 0.52%. Futures tracking US stock indices were flashing green, pointing to a positive open today.

COMMODITIES: Oil prices moved higher today and are set to post the second consecutive green day after private API data yesterday showed that US crude inventories declined more than expected in the preceding week. WTI and Brent crude were both up by 0.13% and 0.87%, at $68.61 and $74.08 a barrel respectively, ahead of the release of official EIA inventory data today. In precious metals, gold prices are trying to recover some losses. The yellow metal is up by 0.5% on the day, currently hovering just above the $1230 per troy ounce mark.

Day ahead: Juncker meets Trump, all eyes on trade; corporate earnings also in focus

In a relatively light day in terms of data releases, the main event will likely be a meeting between US President Donald Trump and European Commission President, Jean-Claude Juncker in Washington. The two are expected to discuss trade, with any material comments having the capacity to affect broader market sentiment.

Juncker will likely seek a waiver of the US tariffs on EU steel imports, and Trump will look for the EU to lower its levies on US imports in general. Crucially, a failure to reach an agreement could even provoke fresh tariffs on European cars imported into America – as Trump threatened a month ago. In light of this, the stocks of popular European carmakers like Daimler and BMW will probably be extremely sensitive to any developments. Besides equities, safe-haven currencies like the Japanese yen could also be impacted, attracting inflows in case of an escalation in tensions, or coming under selling pressure on signs of a potential deal. The opposite holds true for risk-sensitive currencies like the Australian dollar. In this sense, aussie/yen looks like a good proxy for how trade tensions may play out.

In terms of economic data, the only notable release will be US new home sales for June, due out at 1230 GMT. They are expected to have declined by 2.8%, a turnaround following a 6.7% gain in May.

Turning to equities, the earnings season continues with Boeing, Facebook, Paypal, and Qualcomm being some of the companies reporting their quarterly results today. Boeing’s earnings will go public before Wall Street’s opening bell, while the other three will report their own after the market close.

In energy markets, the weekly EIA inventory data are slated for release at 1430 GMT. The forecast is for a 2.3mn drawdown in crude stockpiles, after a 5.8mn rise in the previously tracked week.

As for other public appearances, a meeting between Canadian Foreign Minister Freeland and Mexican President-elect Obrador could attract the interest of loonie and peso-traders.