{kind=link}

Monday July 23: Five things the markets are talking about

A new week starts with equities under pressure as capital markets digest warnings from G20 finance ministers about the impact of protectionism on growth – “risks to the world economy have increased.”

Also raising concerns is the Sino-U.S trade war is now spilling over into currency markets with President Trump rhetoric supporting the U.S administration preference for lower U.S dollar interest rates and a weaker currency.

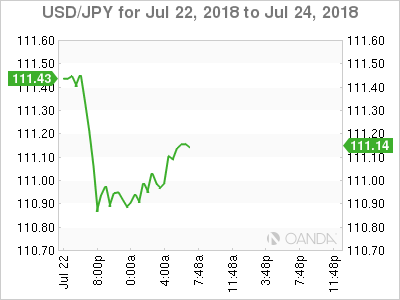

Elsewhere, the yen (¥111.00) has found support while JGB’s slid on speculation about Bank of Japan’s (BoJ) stimulus. Crude prices trade a tad softer amid concern the escalating trade rows will destabilize energy demand.

On tap: an E.U Trade Commission is due to arrive stateside this week for trade talks. Expect some tough questions, demands and their own list of retaliatory measures in response to proposed U.S tariffs. The highlight of the week should be Thursday’s European Central Bank (ECB) monetary policy meeting.

1. Stocks start the week under pressure

Japan’s Nikkei fell to a ten-day low overnight, with exporters under pressure by the yen’s (¥111.00) rally and by market speculation that the Bank of Japan (BoJ) could wind back its exchange-traded fund purchases. The Nikkei ended the day down -1.33%.

Note: The market is speculating that the BoJ could debate changes in its monetary policy at its upcoming meeting, with potential tweaks to its interest rate targets and stock-buying techniques on the table.

Down-under, Aussie shares fell on President Trump’s threat to impose tariffs on all Chinese imports. The S&P/ASX 200 index declined -0.9% at the close of trade. The benchmark gained +0.4% on Friday. In S. Korea, it was a similar story. The Kospi fell about -1% overnight following Trump’s comments about tariff’s and the currency last week.

In China, stocks rallied on Monday, aided by strength in financials and industrial stocks, but a slump in healthcare shares capped the broader gains. The blue-chip CSI300 index rose +0.9% while the Shanghai Composite Index ended up +1.1%.

In Hong Kong, it was a similar story. Stocks rose slightly overnight, as declines in tech and consumer shares were offset by strength in financials. The Hang Seng index rose +0.1%, while the China Enterprises Index gained +0.5%.

In Europe, regional bourses are trading mostly lower across the board, following a mixed session in Asia. The Italian FTSE MIB is in focus following weakness in shares of Fiat and Ferrari after the stepping down of its CEO Sergio Marchionne due to health.

U.S stocks are set to open in the ‘red’ (-0.1%).

Indices: Stoxx600 -0.1% at 385.1, FTSE -0.4% at 7651, DAX -0.1% at 12549, CAC-40 -0.3% at 5382, IBEX-35 +0.2% at 9743, FTSE MIB -0.1% at 21,775, SMI -0.5% at 8947, S&P 500 Futures -0.1%

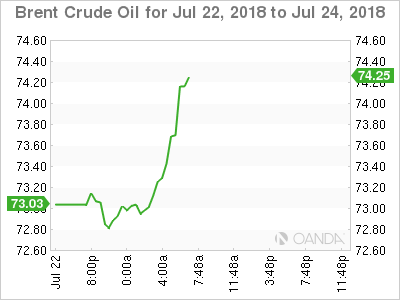

2. Oil steady after G20 warns of risks to growth, gold higher

Oil prices have stabilized as worries over production losses were outweighed by concerns that trade disputes would reduce economic growth and hit global energy demand.

Benchmark Brent crude oil is up +15c at +$73.22 a barrel, while U.S light crude is unchanged at +$68.26.

G20 Finance ministers over the weekend called for more dialogue to prevent trade and geopolitical tensions from hurting growth as “downside risks over the short and medium term have increased.”

Note: Baker Hughes data on Friday showed that U.S energy companies last week cut the number of oil rigs by the most since March following recent declines in oil prices. Drillers cut five oilrigs in the week to July 20, bringing the count down to 858.

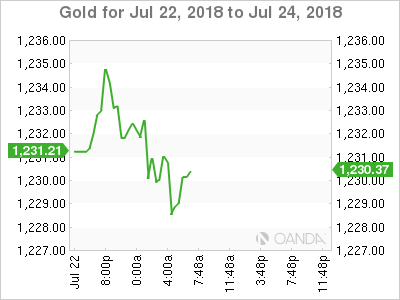

Ahead of the U.S open, gold prices are steady atop of a one-week high as the dollar eased to a two week low after President Trump criticised the Fed’s interest rate tightening policy. Spot gold holds steady at +$1,231 an ounce. U.S gold futures for August delivery are nearly unchanged at +$1,231 an ounce.

3. Japan yields in focus

JGB’s have sold-off along the curve on reports late Friday that the BoJ might consider changes to interest rate targets. The market is speculating that the BoJ might be willing to let 10-year JGB yields (+0%) rise to some degree including a possible hike of the target level. Overnight, JGB 2-, 10- and 30-year yields were higher (+1.8, +4.5, and +8.0 bps respectively).

BoJ officials said to be looking for ways to keep stimulus program sustainable while reducing the harm it causes to markets and bank profits.

Note: The BoJ stepped in to buy unlimited bonds at a fixed rate of +0.11%, to cap the move.

On tap for this week: The ECB monetary policy meeting is on Thursday, no policy stance expected, but the market is looking for clarification on their first potential rate hike.

Elsewhere, the yield on 10-year Treasuries gained less +1 bps to +2.90%, the highest in more than a month, while in the U.K; the 10-year Gilt yield advanced +1 bps to +1.232%.

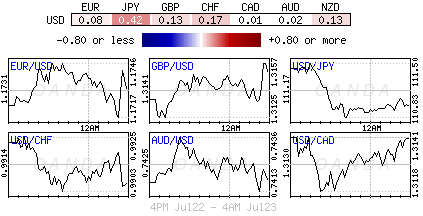

4. Dollar under pressure from Trump rhetoric

The ‘mighty’ USD maintains its softer tone after President Trump criticized the Fed for raising interest rates and suggested the USD was too strong.

Aside from currency Twitter rants, the markets focus this week will be on the ECB rate decision and press conference on Thursday. Consensus is ‘not’ anticipating any policy change in the short to medium term, however, the markets will be on the lookout for any clarification on the first potential rate hike. The EUR/USD is still flipping alternately between moves towards €1.16 and over €1.17 in response to news on the trade row, given the lack of clear direction.

GBP (£1.3124) continues to remain vulnerable to “headline risk,” but consensus believes a lot of negativity seems to be already priced. With parliament in recess, sterling has the potential to stage a modest retracement from its current area.

5. G20 communiqué

In their final communiqué yesterday from their meeting in Argentina, finance ministers and central bankers from the G20 economies said, “Heightened trade and geopolitical tensions pose an increased risk to global growth” and called for greater dialogue.

“Global growth remains robust and unemployment is at a decade low. However, growth has become less synchronised recently, and downside risks over the sort and medium term have increased,” said the communiqué.