{kind=link}

Here are the latest developments in global markets:

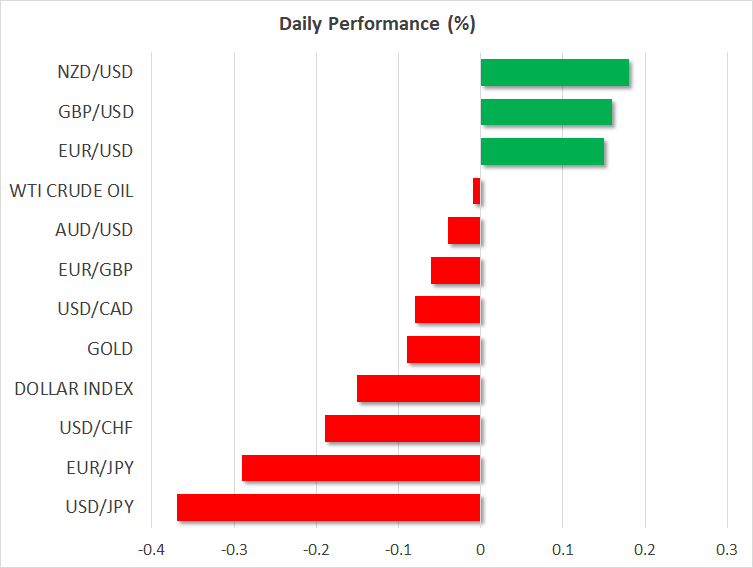

FOREX: The US dollar continued to find itself under pressure following the comments by President Trump criticizing the Fed’s rate hike plan and also characterizing the dollar as too strong and other countries as currency manipulators. The yen posted impressive gains because on the one hand there was some risk-off sentiment and on the other hand there were rumors that the Bank of Japan was thinking how to modify its monetary stimulus program so as to make it more sustainable and let markets play a bigger role.

STOCKS: Following a flat session on Wall Street on Friday, Asian stocks were mixed during Monday’s trading with Chinese stocks gaining but Japanese and Australian stocks posting losses. Europe was looking to open lower. Stocks are mostly moving positively because of an upbeat US earnings season although worries about trade wars have a limiting effect on their gains.

COMMODITIES: Gold continued to capitalize on the dollar’s weakness and managed to trade as high as $1235 an ounce during early Asian trading. It backed off to around $1230 later. There was not much excitement in the oil market as WTI futures were steady but well off Friday’s highs. Oil was slightly above $68 a barrel. Friday’s Baker Hughes oil rig count showed a drop in rigs in the United States.

Major movers: Trump comments rattle dollar; Yen gains on rumors that BOJ may alter stimulus program

President Donald Trump was yet again one of the main market movers, as this time he criticized the Federal Reserve about its rate hikes. Trump also accused countries such as Japan and the Eurozone of manipulating their currencies lower. It is difficult to determine how serious Trump’s comments are and the impact they are going to have in the medium-term. However, as was the case with the rhetoric about trade protectionism, it could be a mistake to disregard Trump’s comments as pure rhetoric. True, Trump does not have the constitutional power of affecting monetary policy directly but through his appointments on the Fed’s Board of Governors and by making interest rate policy a political debate, it could create problems for the Fed to carry out its mission in an independent way. This is, of course, a factor worth watching in the future but it is still unlikely to derail the current US dollar rally or to dissuade the Fed from raising interest rates further – at least in the short-term.

The yen, on the other hand, rallied on rumors that the Bank of Japan is considering revisions to its quantitative easing program. Any alteration to the Quantitative Easing program would almost certainly involve a tightening of conditions. The BoJ has been doing massive monetary stimulus for so long without achieving its desired goal of raising inflation, that one is justified in wondering whether a change is called for. The next monetary policy meeting is on July 30. There was an increase in Japanese Government Bond (JGB) yields that helped the yen climb higher. Another factor that was perhaps supporting safe havens such as the yen was a fresh tweet by President Trump that warned Iran with strong language against threatening the United States.

Day ahead: Eurozone flash Consumer Confidence Index in focus; trade developments eyed

On Monday, July’s flash figures on consumer confidence due at 1400 GMT will attract the most attention in the Eurozone as investors are eagerly looking for signs showing that the bloc’s economic slowdown in the first quarter was a temporary blip. The European Commission, however, is expected to say that the measure remained in negative territory for the second month running, with analysts predicting the index to deteriorate to -0.7 from -0.5 in June, a bearish growth evidence that could keep growth prospects for the second quarter pessimistic ahead of the preliminary PMI readings on Tuesday and the ECB monetary policy meeting on Thursday. While the central bank has already announced its decision to terminate its asset purchasing program at the end of this year, a miss in data this week could turn policymakers cautious on future rate hikes as the central bank is planning to shift focus back to rate adjustments after ending its QE program, with markets projecting the first rate rise to come not until the end of 2019. Should today’s data indicate that consumers have lower-than-expected prospects on their future spending, euro/dollar could start erasing Friday’s gains. On the other hand, a surprising improvement in the numbers could help the pair to continue its recovery.

At the same time (1400 GMT) in the US, the calendar is scheduled to deliver stats on existing home sales for the month of June. After contracting by 0.4% month-on-month (m/m) in May and plunging by 2.7% in April, forecasts are now for a growth of 0.5%. The number of existing residential buildings sold in the previous month is anticipated to inch up from 5.43 million to 5.44mn. Still, new potential developments on the trade front could offset any data impact today as the G20 meeting between finance ministers and central bank delegates during the weekend did little to ease tensions. Instead, the US backed its import tariffs and urged its allies to ease their barriers on US products, a few days after the US president said he was ready to impose tariffs on all goods imported from China. European finance ministers were also on the defensive, claiming that no trade deal is possible with the US unless the US removes its duties. On Wednesday, all eyes will turn to Washington, where Trump and the President of the European Commission, Jean-Claude Junker will meet to discuss on security and economic matters such as tariffs on metals and imported cars, with markets being interested to see whether Junker could achieve some progress in the countries’ relations.

Meanwhile in neighboring Canada, May’s wholesale trade figures will gather some attention at 1230 GMT.

As of today’s public appearances, Bank of England’s Deputy Governor Ben Broadbent will give a speech to the Society of Professional Economists in London at 1700 GMT.

In stock markets, earnings releases continue, with Google’s parent Alphabet being among companies to report quarterly reports after the market close. The company is expected to report higher earnings per share year-on-year.

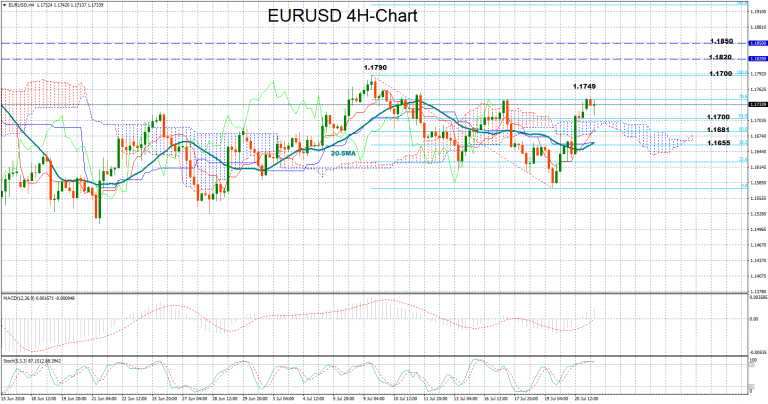

Technical Analysis: EURUSD in bullish mode; stochastics in overbought zone

EURUSD managed to rebound after touching 3-week lows at 1.1574 last week, rallying back above the Ichimoku cloud and the 20-period moving average in the four-hour chart. While the MACD continues to gain strength in positive territory above its red signal line, hinting that the market could maintain bullish momentum, stochastics signal that some weakness in the very-short-term cannot be excluded as the blue %K line is set to cross below the red %D line above 80, in overbought zone.

Still, an upward surprise in Eurozone’s consumer confidence readings could help the market to extend its bullish move above today’s peak of 1.1749, with scope to test July’s 9 top of 1.1790. If this proves a weak resistance, the price could also break the 1.1800 key-level which could be of psychological significance to test the area between 1.1820 and 1.1850 which bulls have failed to overcome since mid-May.

In the alternative scenario, if the numbers show a steeper-than-expected deterioration in consumers’ future spending appetite, euro/dollar could fall back below 1.1700, where the 61.8% Fibonacci of the bearish move from 1.1790 to 1.1574 is placed. Even lower, the pair could touch the 50% Fibonacci of 1.1681 before it meets the 20-period and the 38.2% Fibonacci around 1.1655.