{kind=link}

Here are the latest developments in global markets:

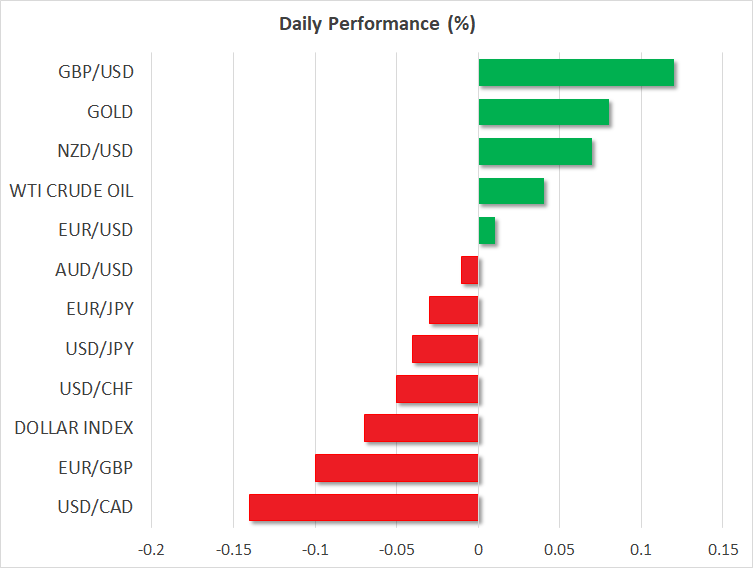

FOREX: The US dollar was trading lower against the Japanese yen on Friday, though by not much, at 112.40 (-0.07%) remaining below the 1-year high of 113.15 reached on Thursday as investors kept in mind Trump’s criticism made on Thursday about higher US interest rates and a stronger dollar. Renewed US trade warnings against China today did little to move the pair (see below). The dollar index against a basket of currencies moved down by 0.05% after the bounce off the 1-year high of 95.65. The weakness of the greenback, drove euro/dollar and pound/dollar higher by 0.03% and 0.18% respectively. The antipodean currencies were mixed today, with aussie/dollar losing 0.01% to trade at 0.7358 and kiwi/dollar advancing by 0.09% to 0.6749. Moreover, dollar/loonie headed lower by 0.15% ahead of the release of Canadian CPI and retail sales figures later in the day.

STOCKS: European stocks were trading lower on Friday, as autos and bank stocks dropped amid a new escalation in trade tensions. The benchmark European STOXX 600 and the blue-chip Euro STOXX 50 were lower by 0.54% and 0.66% respectively. The German DAX 30 tumbled by 0.83%, the French CAC 40 plunged by 0.97%, the Spanish IBEX 35 slipped by 0.60% and the British FTSE 100 dipped by 0.40%. The Italian stocks were also on the backfoot (-0.47%), facing additional pressure from political divisions in Italy. US stock futures were in a sea of red.

COMMODITIES: Oil prices rose today; however, the weekly session remains negative. West Texas Intermediate (WTI) crude oil traded higher by 0.30% at $69.67 per barrel, while London-based Brent surged by 0.43% to $72.89 per barrel. In precious metals, gold and silver bounced off one-year lows, with the former being up by 0.14% at $1,223.70 per ounce and the latter 0.81% higher.

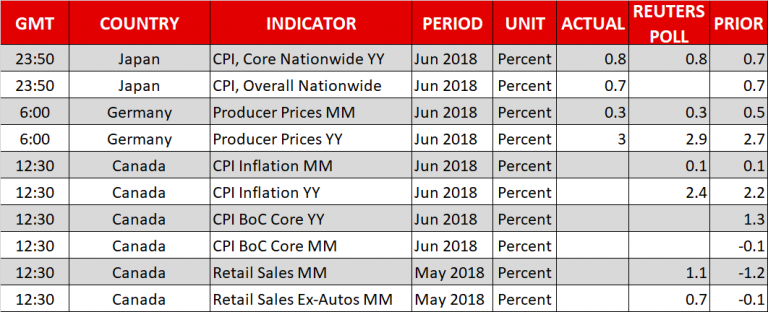

Day ahead: Canada reports on inflation and retail sales; G20 meeting kicks off in Buenos Aires

Friday’s economic calendar will feature Canadian CPI and retail sales figures, while the global trade turmoil will continue to feed risk-off sentiment as the US shows no appetite to pull back its protectionist tariff measures, whereas the EU and China seek ways to defend their interests.

At 1230 GMT, Statistics Canada is expected to show that overall consumer prices have risen by 2.4% year-on-year in June, 0.2 percentage points faster than in May when the headline CPI stood at 2.2%. Given that Bank of Canada aims to keep the total CPI inflation at the 2.0% midpoint of a target range of 1-3.0% over the medium-term, markets could increase speculation that policymakers are preparing another 25bps rate hike in coming months. The soonest such a rate hike could be delivered would be at the October or December meeting where investors give a chance of 43% and a 54% respectively. While there are is no forecast available for the core, median, or trimmed mean CPI measures, these will be closely reviewed as the central bank uses these volatility-free indices to identify changes in the inflation trend.

Canadian retail sales, which are considered an ideal proxy for household spending, will also be under the spotlight at the same time. After a 1.2% decline in April, analysts believe that retail sales have rebounded substantially by 1.2% m/m in May. If this is the case, that would be the strongest growth registered since December 2017. In the absence of automobiles, the core equivalent is also projected to recover, rising by 0.7% m/m after falling by 0.1% in the previous month.

Should retail sales increase more than analysts predict, signaling that the previous downturn could be temporary and instead inflationary pressures are heating up, something that could be also proved if CPI figures beat forecasts today, the loonie, which is set to close in the red for the second consecutive week, could erase losses. Alternatively, in the wake of disappointing prints which could reduce odds for further stimulus reduction, the loonie could once more find itself under pressure.

Still, trade uncertainties remain a high risk for the loonie as Canada has already started being subject to steel and aluminum import tariffs to the US, while the NAFTA story continues to hold in the dark as Canada and Mexico have no intentions to leave the pact despite the US pushing to trim the free-trade agreement and sign separate deals with its Canadian and Mexican counterparts. Therefore, trade issues are something policymakers will seriously consider before proceeding with further stimulus reduction.

Developments on the trade front could create headlines during the weekend (or next week) as the Group of 20 finance ministers and central bank presidents will be gathering in Buenos Aires in Argentina, where trade issues might be high on the agenda. The atmosphere though might not be positive as tariff-affected countries are expected to express their frustration over the US import tariffs on steel and aluminum and the retaliatory responses the measures created. In the meantime, the US unleashed fresh warnings towards China, threatening to punish all imports from China, worth $505bn per year. Note that at the March G20 meeting, financial representatives criticized protectionism and called for further dialogue which so far had minimal effect.

Meanwhile in Eurozone, Italian politics moved to the forefront, pushing Italian stocks to negative territory after reports that the Italian Deputy Prime Ministers, Luigi Di Maio, and Matteo Salvini, had asked for the resignation of the Minister of Economy Giovanni Tria if he did not back government nominees to lead key companies. While the statements were denied on Friday, the news reminded investors that political divisions within the Italian government are still a risk for the markets. In other concerns, comments from Italy’s Head of the budget committee at the Lower House Claudio Borghi, written on Italy’s daily newspaper” The Corriere della Sera”, stated that “Italy will come out of the Euro sooner or later”, adding to the bearish sentiment.

In Northern Ireland, UK Prime Minister, Theresa May, will reiterate that a border infrastructure down the Irish sea is unacceptable, while at the same time the EU Brexit negotiator, Michel Barnier will be delivering EU’s position on the Brexit plan approved in Chequers. Barnier will speak to the media after his meeting with 27 EU ministers.

In oil markets, Baker Hughes is scheduled to issue its report on the numbers of active rigs for oil drilling at 1700 GMT.

As of today’s, public appearances, St. Louis Fed President, James Bullard (non-voting member this year), will be giving a presentation on the U.S. economy and monetary policy before the Glasgow Chamber of Commerce at 1220 GMT.