{kind=link}

Canada will see the release of its inflation and retail sales data on Friday at 1230 GMT. Forecasts point to an acceleration in price pressures and a sharp rebound in sales, which if confirmed, could enhance speculation for another BoC rate increase this year. Beyond economic data, any developments on the NAFTA front could also be crucial for the loonie’s forthcoming direction.

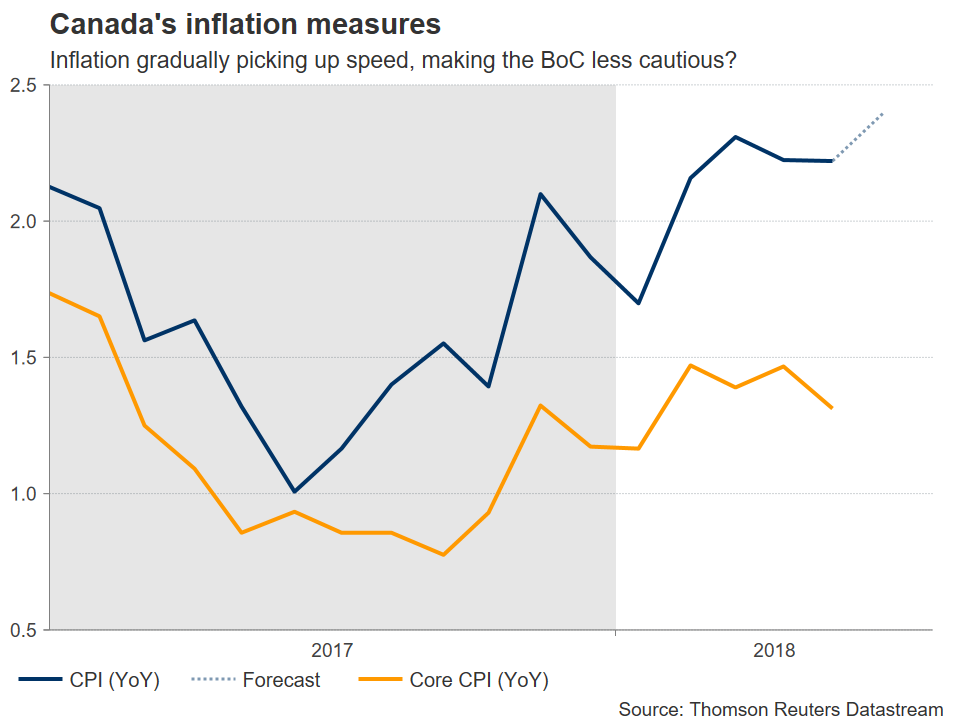

When the Bank of Canada (BoC) raised interest rates last week for the second time this year, it maintained a relatively neutral tone. It acknowledged the Canadian economy is strong and will likely require higher rates over time, but also recognized that uncertainty surrounding trade tensions had risen further. Overall, policymakers signaled that a deteriorating trade outlook was unlikely to deter them from hiking rates further in the coming months, provided that domestic economic figures hold up, of course.

Hence, the quality of incoming economic data will likely be crucial in determining the timing of the next rate increase. At the time of writing, investors are still undecided on whether such an action will take place this year. Implied odds derived from Canada’s overnight index swaps (OIS) suggest investors see a 43% probability for a 25bps rate hike at the Bank’s October meeting, which jumps to 54% when looking at the December gathering.

Turning to this week’s data releases, Canada’s CPI rate is anticipated to have risen to 2.4% in June on a yearly basis, from 2.2% previously. No forecast is available for the core, median, or trimmed mean CPI measures. As for retail sales, they are projected to have grown by 1.1% in monthly terms in May, a rebound following a 1.2% drop in April. Put together, such prints would signal both that inflationary pressures continue to mount and that April’s setback in retail sales was only temporary. Supporting the inflation forecast is the nation’s Markit manufacturing PMI, which indicated that goods prices rose at the fastest pace for over seven years in June.

A strong set of data that amplifies the case for another rate increase this year is likely to help the loonie recover. Technically, declines in dollar/loonie may find the first line of support near 1.3062, the low of July 9. A downside break could open the way for the June 8 trough of 1.2917, with another break lower increasingly bringing into view the 1.2815 zone, defined by the low of May 31.

On the flipside, weaker-than-expected readings could push dollar/loonie higher, as investors begin to doubt whether the BoC will touch the hiking button again soon. In such a case, if the pair has a successful closing session above 1.3256, marked by the inside swing low of June 22, the one-year high of 1.3385 would come into view before the focus shifts to 1.3540, the peak from 9 June 2017.

In the big picture, beyond economic data and expectations around the BoC, the loonie’s broader direction will also depend on the outlook for global trade and specifically, whether some NAFTA deal is reached in the foreseeable future. Judging by the fact the loonie has weakened substantially in recent months even despite a vibrant Canadian economy and higher oil prices, markets seem to have priced in a rather adverse outcome. This implies that any encouraging developments around NAFTA could lead to an outsized positive reaction in the loonie, though there is currently little to suggest anything like that is imminent.