{kind=link}

Here are the latest developments in global markets:

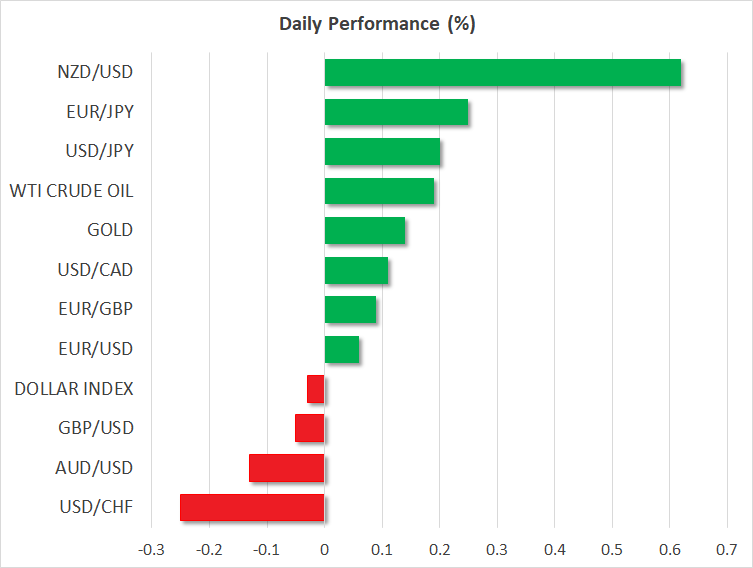

FOREX: The US dollar was trading higher at 112.48 against the Japanese yen (+0.20%) ahead of the Federal Reserve Chairman Jerome Powell’s semi-annual testimony on the economy and monetary policy. Overall, the dollar index was weaker against a basket of six major currencies (-0.13%) and is set to post the third consecutive negative day. Pound/dollar touched a session high of 1.3267 after the Office for National Statistics revised April’s average earnings index (including bonuses) from 2.5% to 2.6%. May’s average earnings (including bonuses) grew by 2.5% as expected, while the unemployment rate remained unchanged at 4.2%. The pair, though, soon returned to 1.3240, trading near today’s opening levels as the BoE chief Mark Carney highlighted during his testimony that a no-Brexit deal could be a risk to interest rates. Euro/dollar broke the 1.1700 handle once again, developing higher by 0.15%. Meanwhile in Tokyo, the EU and Japan signed a trade agreement which was under negotiation since 2013. Still, the partnership needs an approval from the Japanese and European parliaments before it takes effect. Kiwi/dollar traded higher by 0.71% on the day following a rise in core inflation measures, while kiwi/yen added 0.80%. Aussie/dollar seemed to be firm today after the RBA reaffirmed that the next move in interest rates is likely a hike rather than a cut. Finally, dollar/loonie held near its opening levels today, near 1.3132.

STOCKS: European equities were on the backfoot at 1100 GMT. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 were down by 0.25% and 0.40% respectively, with telecommunications overshadowing gains in basic materials. The German DAX 30 declined by 0.17%, while the French CAC 40 lost 0.33%. The Italian FTSE MIB was slighlty up, while the UK’s FTSE 100 was weaker by 0.14%. In the US, even though the S&P dived on and Dow Jones closed up yesterday, futures tracking these indices are currently in the red, pointing to a lower open today.

COMMODITIES: Oil prices were slightly up during the early European session on Monday as worries about possible disruptions to supply eased, while fears over the impact of the US-Sino trade war were holding investors cautious. West Texas Intermediate (WTI) crude oil inched up by 0.10% to $68.13/barrel, holding near 3-week lows reached yesterday. Brent oil edged up to 71.93 (+0.06%) after completing a fresh 3-month low at $71.35 today. In precious metals, gold was also marginally up at $1,241.80/ounce.

Day ahead: Dollar waits for Powell’s semi-annual testimony; US industrial production in focus as well

The Fed chairman’s semi-annual testimony before the Senate Banking Committee later today will be the highlight of the day, while industrial production data out of the US are expected to expose the dollar to volatility prior the speech. Brexit will remain in the forefront as well, as the debate over the withdrawal plan continues today, with the trade bill coming to the House of Commons.

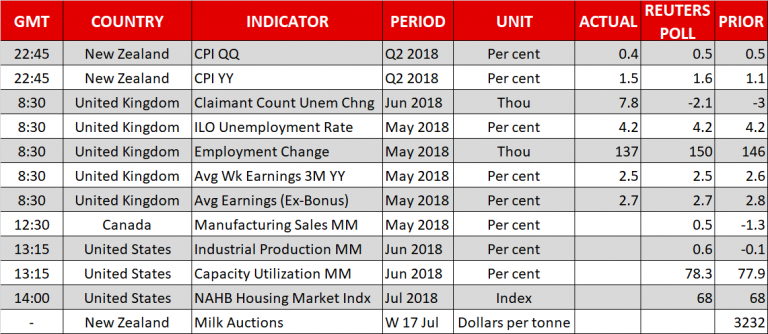

At 1315 GMT, the Federal Reserve is expected to say that US industrial production has returned to positive territory, rising by 0.6% month-on-month in June after contracting by 0.1% in the preceding month. Capacity utilization readings delivered at the same time are also projected to come in higher in June on a monthly basis, whilst a few minutes later at 1500 GMT, July’s NAHB housing market index is anticipated to remain unchanged.

While a data beat could provide support to the dollar, Jerome Powell’s testimony on the economy and monetary policy starting at 1400 GMT could bring steeper fluctuations to the greenback as investors wait to hear any clues on the pace of interest rates, having in mind that two more rate hikes are expected to be delivered later this year. However, as the trade tensions between the US and China continue to boil, Powell could use a cautious tone over the Fed’s future monetary strategy and the country’s economic outlook despite the recent upbeat economic evidence, highlighting the negative impact of a global trade war on the US business environment. In this case, Powell’s message could push the dollar lower. Alternatively, should the Fed chairman appear positive on the economy, signaling that the US could bear higher borrowing costs even under uncertainty about world trade, then the greenback could expand south. On Wednesday, Powell will give his semi-annual testimony in front of the House Financial Services Committee as well.

Meanwhile in New Zealand, changes in global dairy prices are poised to move the kiwi later on Tuesday after the inflation report published earlier showed that a core inflation measure monitored closely by the Reserve Bank of New Zealand climbed to seven-year highs in June.

In Canada, manufacturing sales for the month of May will be under the spotlight at 1230 GMT as analysts believe that the gauge has bounced up by 0.5% m/m in May after declining by 1.3% in April. The API weekly report on US crude oil inventories could also give direction to the commodity-linked loonie at 2030 GMT.

In other events of interest, Russian Energy Minister Alexander Novak and Ukraine-EU officials will hold a two-day meeting to discuss gas supplies.

Goldman Sachs and Johnson & Johnson are among companies releasing quarterly results today; both will be reporting before the US market open.