{kind=link}

Here are the latest developments in global markets:

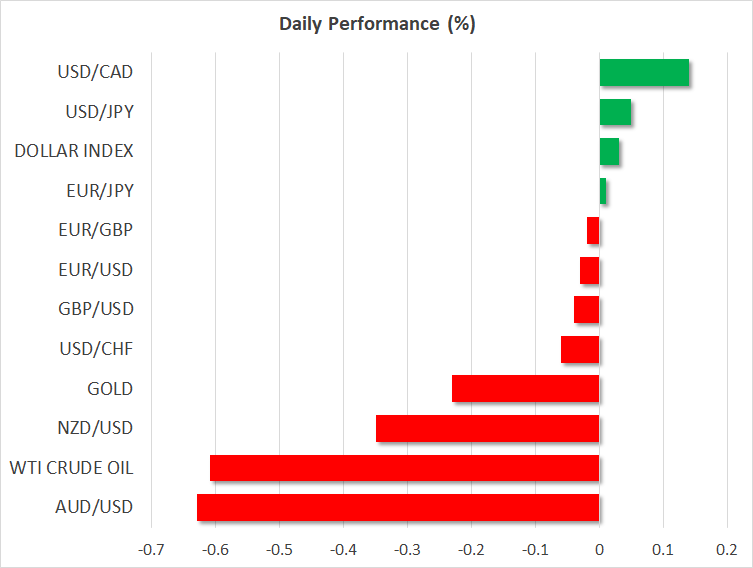

FOREX: The US dollar index is practically flat on Wednesday, after posting some very modest gains in the previous session. Commodity-linked currencies like the aussie, kiwi, and loonie, are all lower, following news overnight that the US is planning another set of tariffs against China.

STOCKS: US markets closed higher yesterday, with the Dow Jones and S&P 500 rising by 0.58% and 0.35% respectively, while the Nasdaq Composite managed to gain 0.04% as well. However, risk sentiment has turned sour after the US announced it is considering another round of tariffs on China. As a result, futures tracking the Dow, S&P, and Nasdaq 100, are all currently pointing to a much-lower open today. Asian indices felt the tariff-heat, with Japan’s Nikkei 225 and Topix dropping by 1.19% and 0.83% correspondingly, while in Hong Kong, the Hang Seng fell by 1.61%. The same was true in Europe, as all the major indices are expected to open considerably lower today, according to futures markets.

COMMODITIES: Oil prices are lower on Wednesday, with WTI and Brent crude being down by 0.61% and 0.98% respectively, following overnight news pointing to a further escalation in the US-China trade standoff. Rising protectionist measures between the world’s two largest economies could stifle economic growth, and hence weigh on oil demand moving forward. A larger-than-expected drawdown in the private API inventory data yesterday was largely overshadowed by trade concerns. In precious metals, gold is down by 0.23% today, trading just below the $1,253/ounce mark. The yellow metal continues to exhibit no responsiveness to boiling trade tensions, with investors instead favoring other haven assets like the Japanese yen and US Treasuries to express their risk aversion.

Major movers: Washington’s new tariff threats disturb market calm

The US announced overnight it is considering an additional 10% tariff on $200bn worth of Chinese imported goods, reigniting concerns around global trade and disturbing the relative market calmness seen over the last few trading sessions. The headlines came right after US markets closed, triggering a classic risk-off reaction. US stock futures fell, as did Asian equity indices and risk-sensitive currencies like the aussie and the kiwi, which are down by 0.62% and 0.35% respectively versus the dollar today. Meanwhile, the safe-haven Japanese yen came under buying interest, recovering some of the losses it had posted earlier in the session.

As expected, China replied a few hours later that it would be forced to retaliate; the Asian nation has responded to every US measure in a proportional, one-for-one manner so far. Overall though, the risk-off reaction was relatively modest, implying that investors still probably view these threats as mere posturing. That said, it’s becoming clearer that the two sides may be entering a vicious, self-enforcing loop of escalation, as neither wants to be seen backing down to the other. It will be crucial to see how Washington responds to the Chinese countermeasures when they are announced, i.e. whether it will hint at even more tariffs. The aussie and the yen will likely stay very sensitive to any developments.

In the UK, pound/dollar managed to edge slightly higher yesterday even despite some disappointing industrial data out of the UK, as the political situation appeared to have calmed down a little. Although still a possibility, the prospect of a no-confidence vote in PM May seems to have faded a little, while her Brexit proposals were welcomed by German Chancellor Merkel as a “step forward”. Although the attention has so far fallen on the domestic UK situation, what’s crucial now for the pound is how the EU will react to the specifics of May’s white paper, which may be released as early as tomorrow.

Meanwhile, the euro took a hit early on Tuesday following a relatively disappointing German ZEW survey, but managed to recover most of its losses in the subsequent hours, with euro/dollar ending the day practically flat.

Day ahead: Bank of Canada decides; US producer prices due; trade developments again in the forefront

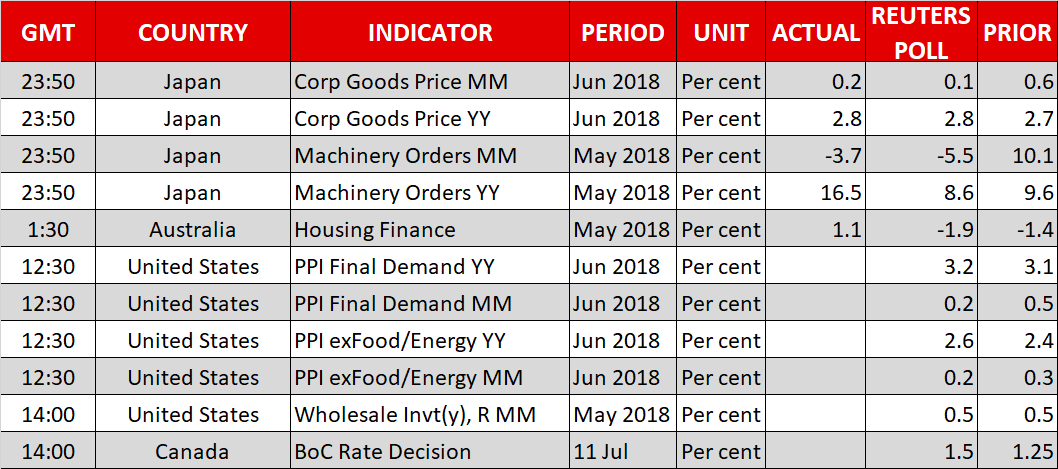

The Bank of Canada’s rate decision is likely to attract most interest out of today’s calendar. Meanwhile, data on US producer prices are also on the agenda, while, beyond releases, the trade (war?) saga is back again in the forefront.

June’s producer price figures will be made public out of the US at 1230 GMT. Both the headline and core measures – the latter excludes volatile food and energy items – are anticipated to accelerate on a yearly basis relative to May, and ease a bit on a monthly basis. The aforementioned readings come a day before the world’s largest economy sees the release of data on consumer price inflation. In addition, data on May’s wholesale inventories are due out of the country at 1400 GMT.

The Bank of Canada’s interest rate announcement and Monetary Policy Report will be released at 1400 GMT. The Bank is widely anticipated to deliver a 25bps rate hike, with the question being on whether it will be a “hawkish” one, that is whether the central bank’s communication will leave the door open for another rate increase soon, or a “dovish” one. The loonie will react accordingly; appreciate in the case of the former and depreciate in the other scenario. BoC Governor Stephen Poloz and Senior Deputy Governor Carolyn Wilkins will be holding a press conference at 1515 GMT – market sensitive comments are not to be ruled out.

On the trade front, China’s response to the US saying it would impose tariffs on additional Chinese imports amounting to $200 billion will be closely watched; tit-for-tat retaliatory actions are likely to trigger a flight to safety to the detriment of riskier assets.

The 9th ECB Statistics Conference will feature remarks by the central bank’s President Mario Draghi (he already delivered some comments at 0700 GMT), Chief Economist Peter Praet (0730 GMT), and Executive Board Members Yves Mersch (1200 GMT) and Daniele Nouy (1530 GMT). BoE Governor Mark Carney will be talking at a conference on the Global Financial Crisis in the US at 1530 GMT, while the Bank’s Deputy Governor, Sam Woods, will be speaking before the Treasury Select Committee. In the meantime, New York Fed President John Williams, who holds permanent voting right within the FOMC, will also be making a public appearance today (2030 GMT), though the topic of discussion is such that would render any comments on monetary policy unlikely.

A two-day NATO summit that President Trump will also attend might be of interest, given the US president’s expressed views on how the organization is funded.

EIA data on crude oil inventories due at 1430 GMT might offer some short-term direction to oil prices. Crude stocks are forecast to have declined by around 4.5 million barrels during the week ending July 6, after rising by around 1.2m in the previously tracked week. Meanwhile, OPEC’s monthly report, which also touches on demand and supply considerations, is due at 1120 GMT.

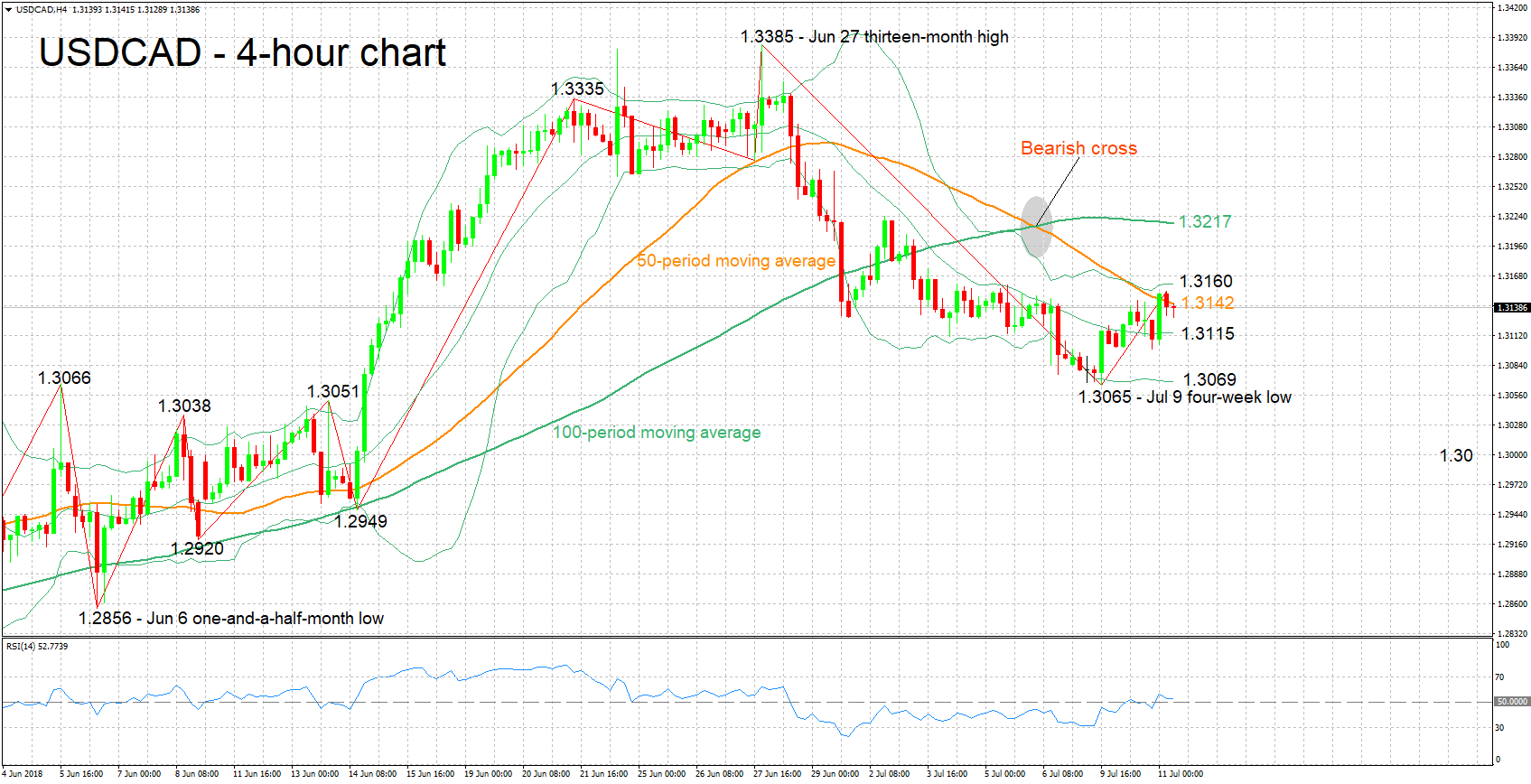

Technical Analysis: USDCAD looking mostly neutral in the short-term

USDCAD has been largely moving sideways since late June in support of a predominantly neutral picture in the near-term. The RSI, which has been hovering around the 50-neutral perceived level, lends credence to the view for a neutral bias in the short-term.

A more hawkish stance by the BoC than priced in by markets later today is expected to boost the loonie, pushing USDCAD lower. Initial support to declines may come around the middle Bollinger line – a 20-period MA line – at 1.3115; the area around this was congested recently, while it also encapsulates the 1.31 round figure. Further below, the focus would fall to the range around the lower Bollinger band at 1.3069 (including the four-week low of 1.3065 from July 9), with stepper losses turning the attention to the 1.30 handle.

Conversely, a relatively dovish BoC is likely to push the pair higher. Immediate resistance seems to be taking place around the current level of the 50-period MA at 1.3142, including the upper Bollinger band at 1.3160. Further above, the 100-period MA at 1.3217 would increasingly come into scope.

US data can also move the pair.