{kind=link}

The Bank of Canada (BoC) is widely expected to raise interest rates when it announces its policy decision on Wednesday, at 1400 GMT. What is much more uncertain, however, is whether policymakers will also highlight their support for further hikes in the coming months amid a relatively strong domestic economy, or whether boiling trade tensions will lead them to downplay such expectations. On balance, the former scenario appears more likely, though it’s a pretty close call.

Put simply, the upcoming BoC meeting will be about two vastly different narratives: a strong domestic Canadian economy, against rising protectionism risks from abroad. With a 25bps rate hike all but priced in already (96% probability according to Canada’s OIS), price action in the Canadian dollar will most likely be driven by the commentary around the future path of interest rates and specifically, by whether another rate increase is on the cards before the end of the year.

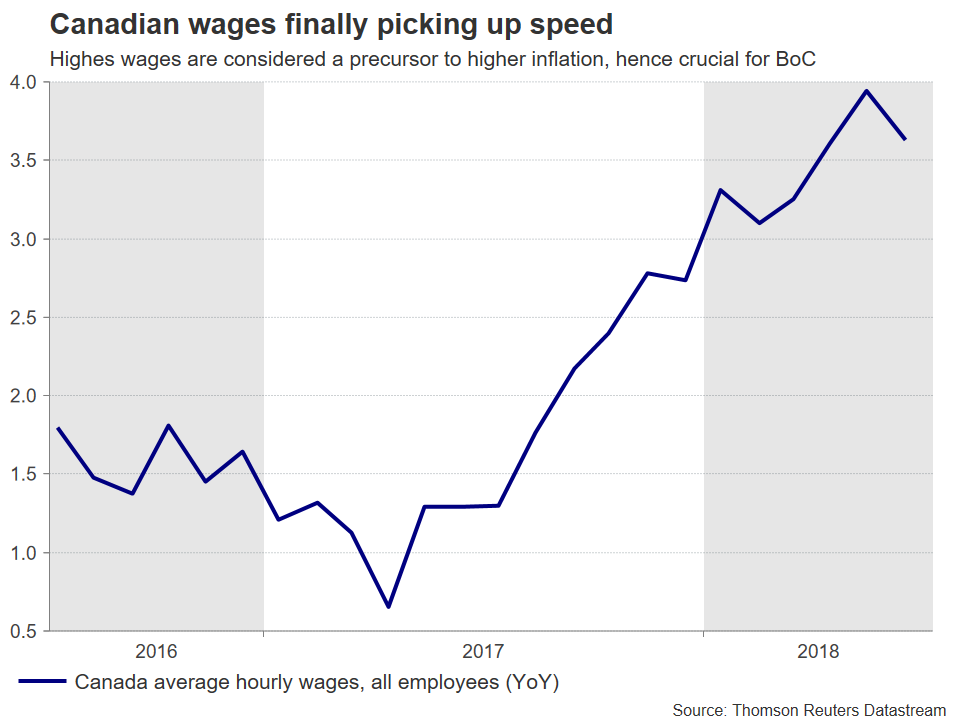

Looking at economic data and recent developments, they are broadly in support for a more hawkish bias. Inflation is close to its target, and while economic growth slowed in Q1, that may have been only transitory as forward-looking indicators like the Markit manufacturing PMI and the BoC’s own business outlook survey are pointing to a solid rebound. Meanwhile, the labor market remains strong, with wage growth picking up considerable speed in recent months, while oil prices have continued to soar, spelling good news for Canada’s oil-exporting economy. Last but not least, domestic risks that the BoC has consistently expressed concerns about – such as rapidly rising housing prices and high consumer debt – have begun to moderate.

On the flipside, trade tensions between the US and its major trading partners have continued to grow, with the latest “plot twist” being the possibility of US tariffs on imported cars, something that would likely complicate further the ongoing NAFTA negotiations. The trade outlook remains clouded, but that may not necessarily deter the BoC from proceeding with its hiking efforts, as the Bank’s underlying assumption so far has been that the current trade arrangement will be maintained – and the situation hasn’t changed drastically enough to derail that hypothesis.

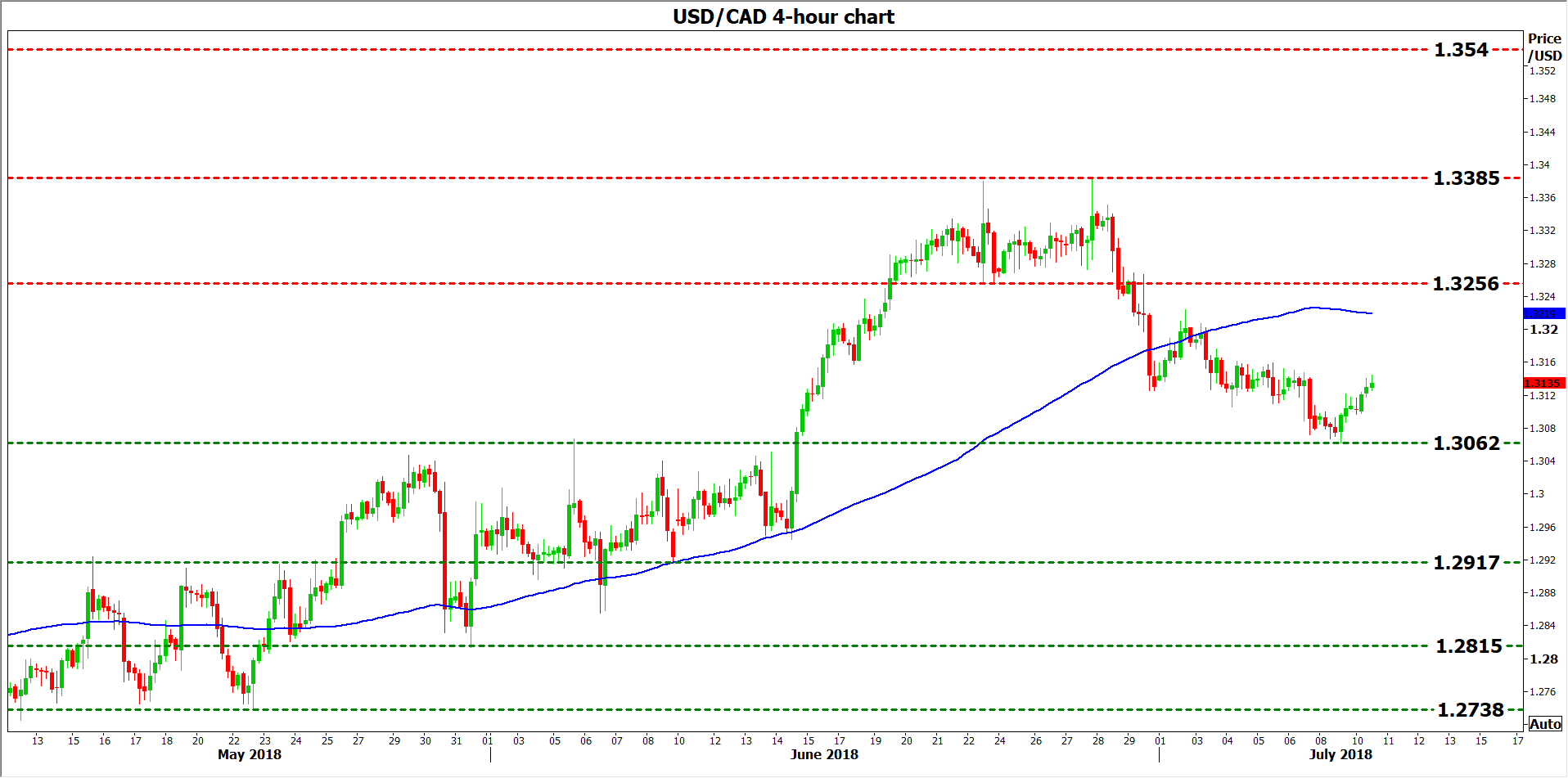

Looking at market pricing, beyond this rate increase that is practically fully priced in already, investors assign a 62% probability for one more hike before the year ends. Should the Bank amplify expectations for another hike, pushing that probability upwards, then the loonie could come under renewed buying interest. Technically, declines in dollar/loonie could encounter immediate support near 1.3062, the low of July 9. A downside break may open the way for the June 8 low of 1.2917, with even further declines bringing into focus the 1.2815 zone, marked by the trough of May 31.

On the contrary, in case of a cautious commentary by the BoC that downplays hiking expectations, dollar/loonie could meet resistance around the 1.3256 area, defined by the inside swing low of June 22. Even higher, the one-year high of 1.3385 would come into view before the focus shifts to 1.3540, the peak from 9 June 2017.

Finally, besides the statement accompanying the decision, note that the Bank will also release updated economic forecasts, and Governor Poloz will hold a press conference at 1515 GMT. Price action in dollar/loonie could be impacted by these as well, particularly any forward-guidance comments during the press conference.