{kind=link}

Here are the latest developments in global markets:

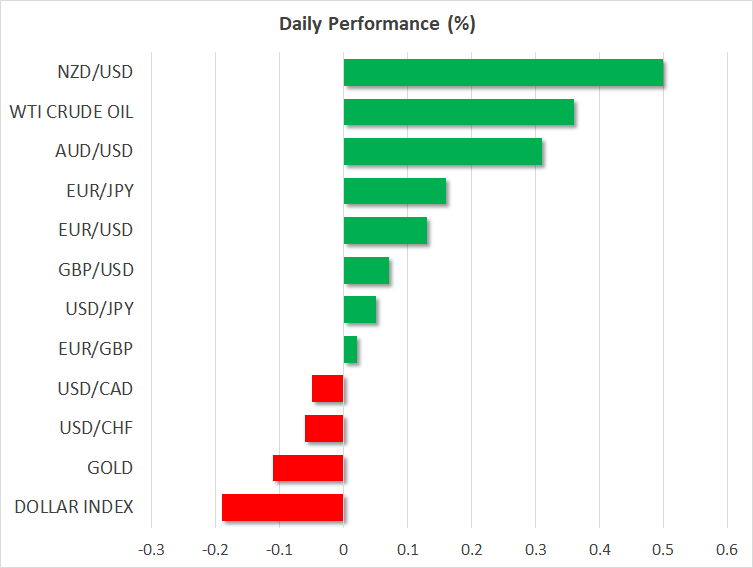

FOREX: The US dollar index is down by almost 0.2% on Friday, ahead of the release of the US employment report for June later today. Meanwhile, the safe-haven Japanese yen is on the back foot, with investors appearing largely unfazed by a possible escalation in the US-China trade saga (see below).

STOCKS: US equity markets closed higher on Thursday, undeterred by the looming threat of the US and China exchanging tariffs on Friday. The Nasdaq Composite led the way, rising 1.12%, with the advance fueled by technology stocks – which have shown remarkable resilience in the face of tariff-worries this year. The S&P 500 and the Dow Jones gained 0.86% and 0.75% respectively. Futures tracking the Dow, S&P, and Nasdaq 100, are currently in positive territory, though only marginally so. The positive sentiment was also evident in Asia, with Japan’s Nikkei 225 and Topix climbing by 1.12% and 0.92% correspondingly, while Hong Kong’s Hang Seng index rose by 0.61%. Europe looks set to follow suit, with futures tracking all the major indices signaling a higher open today.

COMMODITIES: Oil prices are a little higher on Friday, with WTI and Brent rising by 0.36% and 0.13% respectively. Both benchmarks recovered some of the notable losses they posted yesterday. The decline was triggered by reports Saudi Arabia increased its production in June, as well as a surprising build in the weekly EIA inventory data, instead of the anticipated drawdown. In precious metals, gold is lower by 0.1% on Friday, giving back the modest gains it posted in the previous session. The next major market mover for gold will probably be today’s US employment report. Given that the yellow metal is denominated in dollars, it’s likely to move in inverse fashion to the US currency today. Hence, a strong jobs report could weigh on gold, whereas a softer one may boost it.

Major movers: US fires first trade shot, Chinese retaliation eyed; dollar yawns after Fed minutes

The US officially fired the opening salvo in its trade standoff with China earlier this morning, as the announced 25% tariffs on $34bn Chinese goods went into effect. The market reaction was non-existent, given that the move was signaled well in advance. Instead, investors will look towards China’s countermove; the Asian nation has long said it will reply with proportional measures.

The main question is whether the US will then strike back again – as it has warned it will should China respond –, thereby provoking another move from China, and taking the “trade war” narrative to a whole new level. Should such moves unleash another wave of risk aversion in markets, haven currencies such as the yen could benefit over the near-term, to the detriment of risk-sensitive assets, like stocks and the aussie.

Overnight, the minutes from the latest FOMC meeting delivered no surprises, at least for dollar-traders, as the currency barely reacted to the release. While policymakers noted the strength of the US economy and reaffirmed their gradual hiking trajectory, they also sounded a note of caution, highlighting that trade uncertainty could weigh on business investment, and that downside risks have intensified. While their assessment fell short of suggesting suck risks could delay rate increases, that remains a clear possibility should tensions escalate further and manifest themselves into the real economy. Today, all eyes will be on the US jobs report.

In the UK, sterling/dollar erased all its early gains associated with a hawkish tone in BoE Governor Carney’s remarks yesterday, to close the day slightly lower following Brexit headlines. Reportedly, both German Chancellor Merkel and the UK Brexit Minister Davis consider the new customs plan for Brexit presented by UK PM May as “unworkable”.

The UK cabinet will meet today to decide whether it’ll back this plan, but admittedly, these reports likely poured cold water on expectations this proposal could break the deadlock in the negotiations. Theresa May now finds herself between an EU rock and a Brexiteers’ hard place, with political uncertainty likely to continue dominating sterling moves in the absence of any tier-one UK data on the economic calendar for a while.

Day ahead: US jobs report firmly in focus; Canada also receives employment data; trade developments eyed

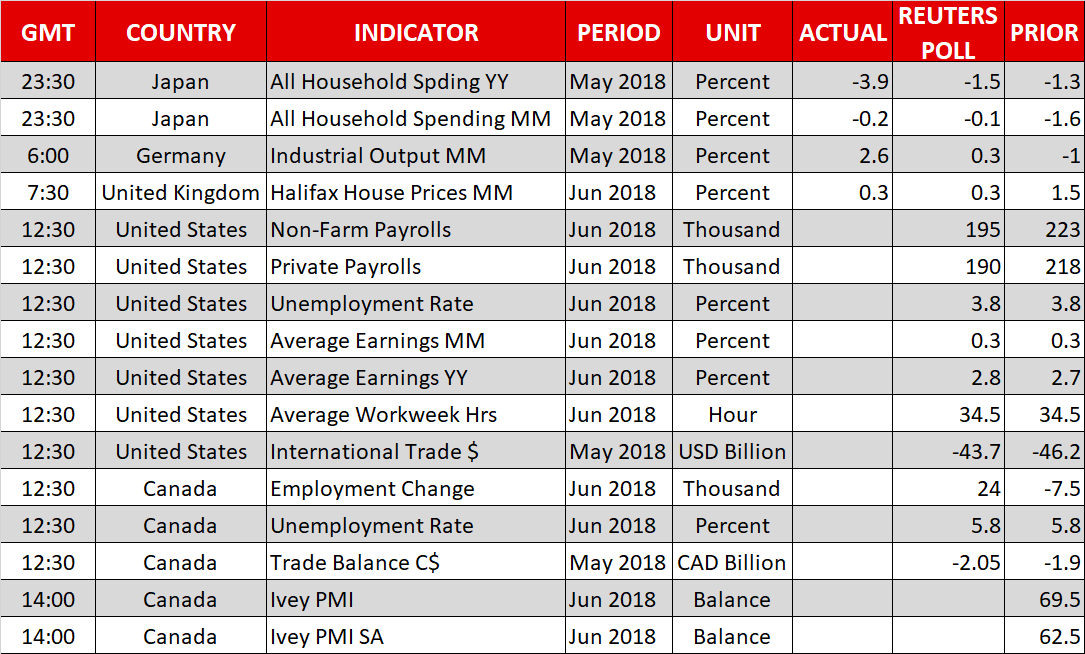

Friday will see the release of what is considered by many as the most important monthly release out of the world’s largest economy, namely the nonfarm payrolls report. Besides this, Canada will also be on the receiving end of employment data, while developments on the trade front will also be closely watched as US tariffs on Chinese goods kick in today.

At 0730 GMT, the Halifax index gauging house prices in the UK during June will be made public. An easing of growth in prices is projected by analysts.

The focus will next turn to the US which will see the release of its nonfarm payrolls report for June at 1230 GMT. After the addition of 223k positions in May, the economy is anticipated to have added another 195k during June. Meanwhile, the unemployment rate is expected to remain at the 18-year low of 3.8%. Economic theory suggests that such a low rate should drive wages up as employers have to compete to attract skilled workers. This takes us to wage growth, which is again expected to attract most interest out of the jobs data: average earnings are projected to expand by 0.3% m/m (the same as in May) and by 2.8% y/y (2.7% in May).

Stronger wage growth has the capacity to stoke inflation expectations, leading market participants to price in a more aggressive Fed tightening cycle, something which is theoretically dollar-positive.

Data on international trade out of the US are also due at 1230 GMT; the deficit is forecast to narrow to $43.7 billion from $46.2bn.

At the same time as the abovementioned figures, Canadian jobs numbers will be hitting the markets. The economy is anticipated to have added 24k positions during June, which compares to a reduction of 7.5k in May. In the meantime, June’s unemployment rate is forecast to remain unchanged at 5.8%, its lowest since the 1970s. Better-than-anticipated data releases have the capacity to more conclusively put on the table a rate hike by the Bank of Canada during next week’s meeting. Specifically, the odds for a rate increase currently stand at 67% according to Canadian overnight index swaps, and should it rise on the back of strong figures today, the loonie could come under renewed buying interest.

Other Canadian data out today include May’s trade balance (1230 GMT) and June’s Ivey PMI (1400 GMT).

With US tariffs on $34 billion of Chinese imported goods going into effect today, the attention now turns to China which has vowed to fight back. The reaction in the markets has so far been calm today. Escalating tensions, though, may trigger a flight to safety, boosting safe-haven perceived assets such as the yen, at the expense of riskier ones.

On the Brexit front, PM Theresa May will be meeting with her cabinet today to discuss key issues in negotiations such as the future trade relationship between the UK and the EU.

A lecture by Daniele Nouy, ECB’s Chair of the Supervisory Board, is on the agenda at 1000 GMT.

In energy markets, Baker Hughes data on the number of active oil rigs in the US are due at 1700 GMT.

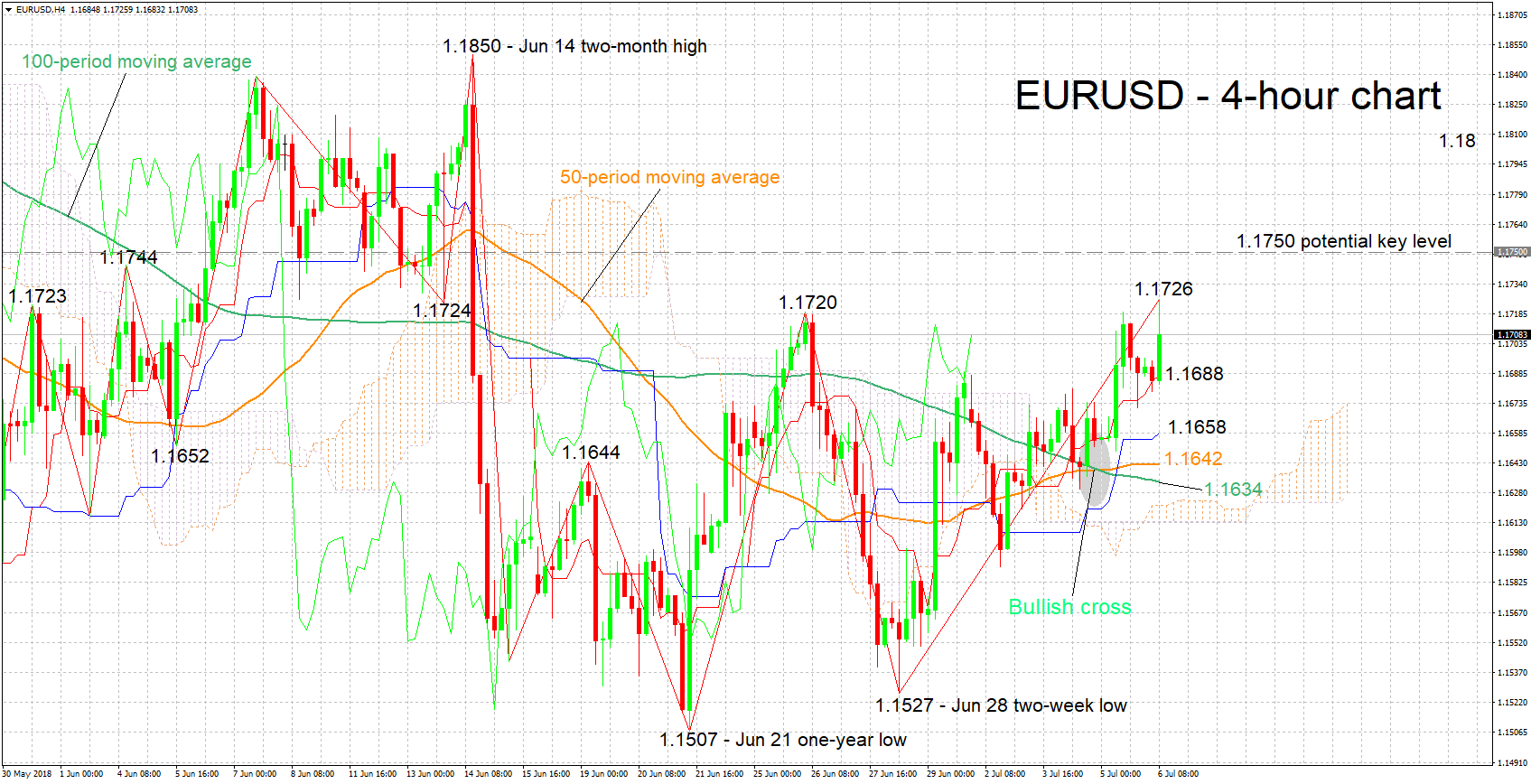

Technical Analysis: EURUSD looking bullish in the short-term, records 3-week high

EURUSD has risen by roughly 200 pips after touching a two-week low of 1.1527 on June 28. Earlier on Friday, it hit a three-week high of 1.1726. The positively-aligned Tenkan- and Kijun-sen lines are projecting a bullish bias in the short-term.

A stronger-than-expected US NFP report, especially on the wage growth front, is likely to weaken the pair. Support could come around the current level of the Tenkan-sen at 1.1688, including the 1.17 round figure. Further below, the focus would turn to the Kijun-sen at 1.1658.

Conversely, weaker-than-anticipated data could push EURUSD higher. Resistance may come around the 1.1750 handle, an area which was somewhat congested in the past. The 1.18 handle would increasingly come into focus in case of stronger bullish movement.

Trade developments can also move the pair.