{kind=link}

The nonfarm payrolls report will be eagerly awaited on Friday at 12:30 GMT for the latest indications on the United States labour market. However, with Sino-US trade tensions running high and tariffs on $34 billion worth of Chinese imports and counter tariffs of similar value on US products due to come into effect the same day, the jobs report may fail to generate the usual amount of fanfare. That is not to say that any surprises to the data won’t sway the dollar as any positive shocks could still lift the currency higher given that a fourth rate hike is not yet fully priced in by the markets.

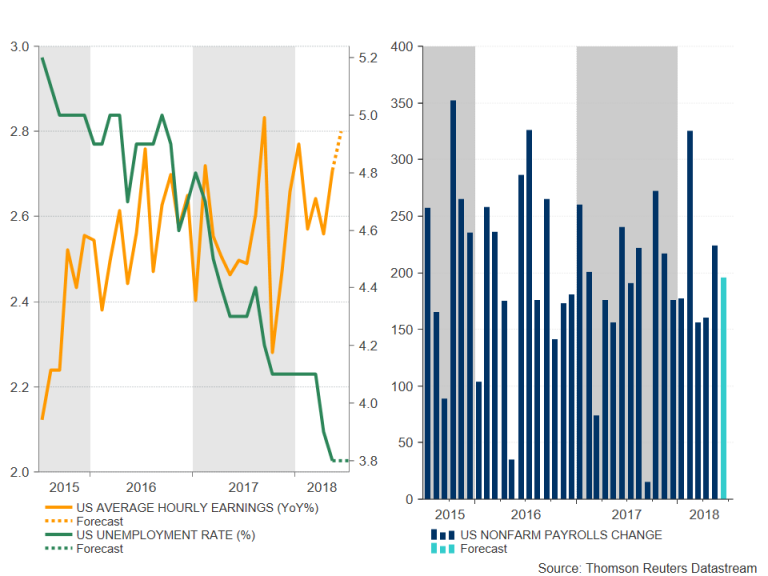

After solid job gains of 223k in May, the US economy is forecast to have added a somewhat more moderate 195k positions in June. The unemployment rate is expected to have held steady at the 18-year low of 3.8% in June. At this point, with the labour market so tight, a miss in the headline payrolls figure wouldn’t cause much concern for investors, while a beat in expectations would only underscore the strength of the US economy.

On the other hand, any big surprises in the other key component of the NFP report – average hourly earnings – could trigger some repricing in fed fund futures. With the Federal Reserve keeping a close watch on wage growth, signs that wages are rising faster than anticipated could worry policymakers, especially now that the Fed has achieved in raising inflation to its 2% target. Average hourly earnings are forecast to have increased by 0.3% month-on-month and by 2.8% on a 12-month basis.

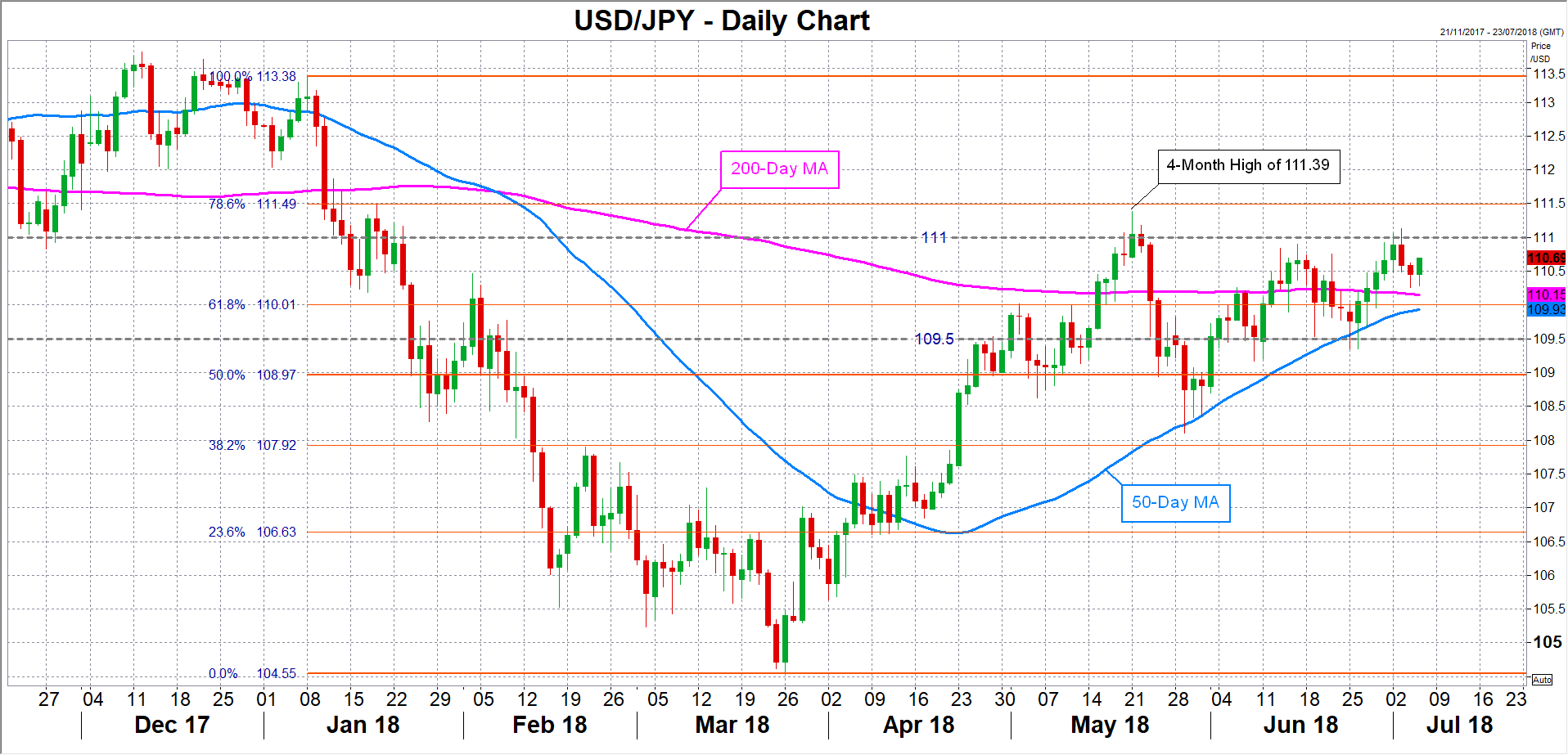

Stronger-than-expected growth in earnings could push up the odds of the Fed hiking rates two more times this year, which are currently hovering around 70%. It could also drive the US dollar higher versus the yen, which this week hit a 6-week peak. The pair could aim for a successful close above the 111 handle, having failed to do so several times this week. A decisive break above the level would clear the way for the May 4-month high of 111.39 with the 78.6% Fibonacci retracement of the January-March downleg at 111.50 not too far away.

Alternatively, a jobs report that is broadly in line or misses the expectations could lead to dollar/yen retreating from the week’s highs. Initial support should come at around the 110 region, which is not only the 61.8% Fibonacci level but also a possible conversion point for the 50- and the 200-day moving averages. Sharper losses could see the pair stalling around 109.50. A breach of that support would open the way to the 109 handle.

However, a bigger threat to the greenback may not come from the NFP data but from trade-related headlines. Any new comments by President Trump or his team that escalates the stand-off between the US and China could hurt investor sentiment in a week where risk appetite is already in short supply. But even in the absence of fresh rhetoric or further retaliatory action, the market mood could still take a turn for the worse as the tariffs look set to come into force with no sign of either side making any concessions and no end in sight to the ongoing uncertainty.

Should fears of a full-blown trade war intensify and trigger another market rout at the end of the week, the dollar would once again likely enjoy demand from safety flows and post fresh gains versus emerging market and risk-sensitive currencies. However, against the safe-haven yen, the dollar would be faced with selling pressure on renewed market volatility.