{kind=link}

The Fed will release the minutes from its June policy meeting on Thursday, at 1800 GMT. Not only did policymakers raise interest rates for a second time this year at that gathering, they also revised higher their rate-path projections to signal a total of four hikes in 2018, from three previously. The minutes may shine a fresh light on how confident the Committee as a whole is on that prospect, with any conversation on trade frictions also attracting attention.

The latter part of this week promises to be a busy and volatile period for the US dollar. After the Fed releases minutes on Thursday, the US employment report for June will hit the markets on Friday – the same day when the US and China are expected to slap tariffs on each other, potentially escalating already-boiling trade tensions.

Focusing on the minutes, they will be released one day later than usual – on Thursday – due to the US Independence Day holiday on Wednesday. Back at the June gathering, the Fed surprised in a somewhat hawkish manner. While a 25bps rate hike was well-signaled and fully priced in ahead of the event, the Committee also upgraded its rate path projections for 2018. The caveat, however, was that the decision to signal faster hikes was a very close call. Just one official raised her/his projection to signal four hikes from three previously, which resulted in the median projection being pushed up as well.

Perhaps due to how close the decision was, markets have not really been convinced the Fed will proceed with raising rates another two times (to bring the total to four this year). While investors are confident at least one more will materialize, something fully priced in already, they are skeptical of a second one – a prospect they assign a mere 39% probability to, according to the Fed funds futures.

Hence, the focus may turn to the conversation on the economic outlook, to gauge what the more cautious officials would need to see for them to join the camp supporting four hikes as well. Moreover, any discussion on the US-China trade standoff will attract attention. Although the Fed had not appeared particularly worried by these frictions, comments by Chairman Powell a few days after the June meeting suggested otherwise. He said businesses are talking about postponing hiring and investment decisions in this environment, though such talk hasn’t shown up in economic data yet. Given the lack of confidence in Powell’s remarks, markets will look for clues on whether the Fed may turn more dovish if trade tensions begin to act as a drag on the economy, perhaps by delaying rate hikes to provide some cushion. Any such signals could work against the dollar.

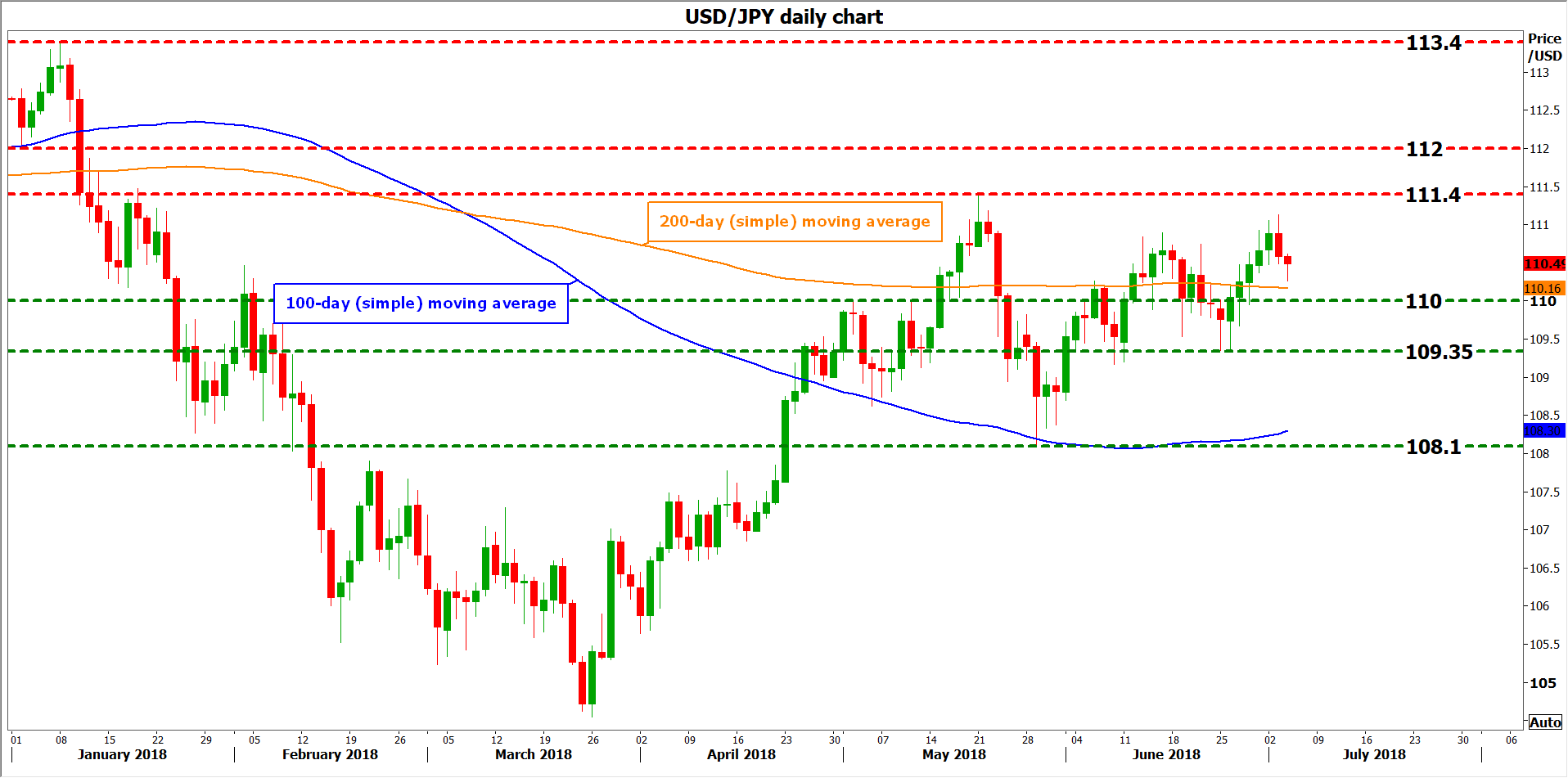

Technically, looking at dollar/yen, potential declines may encounter immediate resistance near the round figure of 110.00, which may hold some psychological importance. The area around it also encapsulates the 200-day moving average, at 110.16. A downside break from there would shift the focus to the June 26 low of 109.35, before the May 29 trough of 108.10 comes into view – notice that the 100-day moving average lies not far above, at 108.30.

On the upside, further advances in the pair could stall initially around 111.40, a zone that halted the rally on May 21. If the bulls power through it, the January 2 low of 112.00 may provide resistance. Even higher, the January 8 top of 113.40 would be eyed.