{kind=link}

Here are the latest developments in global markets:

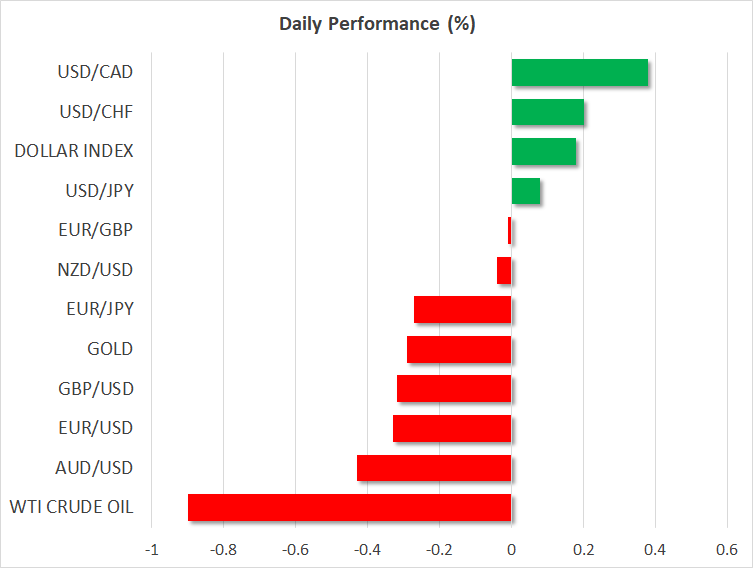

FOREX: The US dollar index – which tracks the greenback’s performance against a basket of six major currencies – was higher by 0.2% on Monday. The euro was a touch softer as German political uncertainties remained a key theme. The loonie was also on the defensive amid a drop in oil prices, giving back some of the gains it posted on Friday following strong data releases.

STOCKS: US markets closed higher on Friday, albeit not significantly so. The Dow Jones gained the most (+0.23%), while the Nasdaq Composite (+0.09%) and S&P 500 (+0.08%) lagged. However, risk appetite seems to have turned sour, as futures tracking the S&P, Nasdaq 100, and Dow, are all in negative territory, pointing to a notably lower open today. The risk-off move may be owed to lingering concerns on trade, as well as reports suggesting a potential reescalation in the North Korea conflict. Reflecting this, Asia was a sea of red on Monday. Japan’s Nikkei 225 and Topix plunged by 2.21% and 2.06% respectively, while in South Korea, the Kospi 200 was down 2.25%. Major European indices are also set to open with large gaps to the downside according to futures, amid continued political turbulence in Germany.

COMMODITIES: Oil prices opened lower on Monday, with WTI and Brent crude being down 0.9% and 1.1% respectively. The drop followed a tweet from US President Trump on Saturday stating that Saudi Arabia’s King Salman had agreed to raise his nation’s oil production. While this was quickly watered down by the White House – which said Saudi Arabia “could” raise production “if needed” – investors still took the opportunity to lock some profits on prior long-oil positions. Overall though, prices remain elevated near multi-year highs, which suggests that while this story may be taking some wind out of oil’s sails, the broader narrative is still one of higher prices and constrained supply. In precious metals, gold was down 0.3% on Monday, hovering just above the $1248/troy ounce level, and continuing to mimic the US dollar’s movements in inverse fashion.

Major movers: German politics keeping euro in check; loonie whipsaws

The euro is trading on a softer note on Monday, down by 0.35% against the dollar, following German political news over the weekend. The migration deal that German Chancellor Merkel brokered at last week’s EU summit was apparently not enough to appease her coalition partners, as Interior Minister Seehofer offered to resign from her cabinet after his CSU party rejected the deal.

The two sides are expected to continue negotiations today in hopes of reaching an agreement. Hence, the common currency will probably remain sensitive to news flow. A potential accord would dispel some political uncertainty, diminish the likelihood for early elections in Europe’s largest economy and likely help the euro to recover. Conversely, a no-compromise scenario could bring the single currency under renewed selling pressure.

On the trade front, the EU Commission reportedly warned the US that tariffs on imported cars would hurt the American economy, and could provoke counter-tariffs from the major US trading partners amounting to $300bn worth of US goods. This week will likely be very interesting, as on Friday, both the US and China are due to implement the $34bn of tariffs they previously announced. As usual, any fresh escalation has the capacity to weigh on risk appetite, triggering a flight into safety and out of riskier assets, such as equities.

Also potentially keeping a lid on risk sentiment, are reports that North Korea may have increased its production of fuel for nuclear weapons. If confirmed, this could trigger a fresh deterioration between US-North Korea relationships, providing another reason for havens like the Japanese yen to stay in demand.

Elsewhere, the loonie surged on Friday, following stronger-than-anticipated Canadian GDP data for April and the BoC’s quarterly business outlook survey, which was upbeat on most fronts, stoking speculation for a rate hike at the upcoming July 11 meeting – a prospect now priced in with a 79% probability. Although dollar/loonie rebounded on Monday, trading 0.4% higher, this move appears to be owed mainly to the tumble in oil prices – Canada being a major oil exporting economy.

Day ahead: US, Eurozone, and UK deliver PMI figures; German political conditions in focus

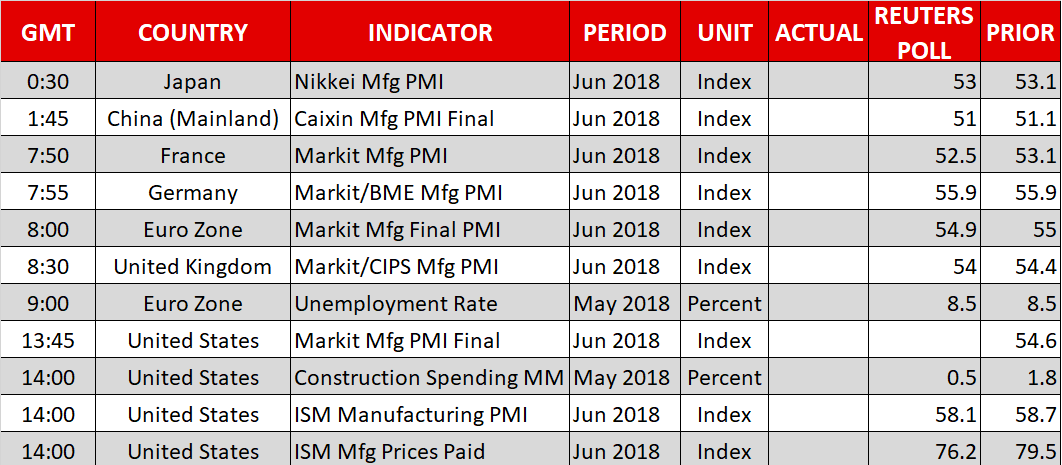

Moving into the second half of year, the trade turmoil and political risks in the Eurozone will continue to weigh on the markets, potentially keeping investors in safe-haven waters for now. But in the absence of any trade or political news, investors will look at the economic calendar for direction on Monday, as Purchasing Managers Index (PMI) readings out of the US, the UK, and the Eurozone are scheduled to give evidence on business activities in the aforementioned regions.

At 0800 GMT, Eurozone’s final Markit Manufacturing PMI for the month of June is expected to come at 55 as was initially estimated, unchanged from May’s mark and below December’s multiyear-high of 60.6. Still, any print above 50 indicates growth in the industry. An hour later, at 0900 GMT, Eurostat will update Eurozone’s unemployment rate, with analysts projecting the measure to stand flat at 8.5% in May, at the lowest since 2009. While an upward surprise in the data could help the euro to recover some gains, the migration puzzle in Germany could refrain investors from taking a position on the common currency, despite the two-day EU summit ending on Friday indicating that EU leaders are broadly on the same side on the topic. Particularly, the issue came back to the surface after news that the German interior minister, head of the coalition CSU party, offered to step down from all offices, complaining that his conversation with German Chancellor Merkel over migration on Sunday had no effect, and that the solution secured with the EU leaders was “ineffective”. Should the dispute remain in place, the euro could find it hard to rebound.

Meanwhile, in the UK, June’s Markit/CIPS Manufacturing PMI due at 0830 GMT is anticipated to ease to 54.0 from 54.4 in May. The report follows Friday’s upward revision of Britain’s GDP growth for the first quarter, which boosted speculation that the BoE will likely push interest rates higher in August. However, Brexit risks could hold traders cautious as the UK Prime Minister, Theresa May, who left the EU summit a day earlier, was unable to give a detailed description on her Brexit plans due to existing divisions in her Conservative party.

In the US, the ISM Manufacturing PMI will attract the most attention in terms of data ahead of the FOMC meeting minutes on Wednesday and the all-important nonfarm payrolls employment report on Friday. The numbers released at 1400 GMT are projected to show that the business index has lost 0.6 points to touch 58.1 in June. If the ISM manufacturing PMI beats forecasts, highlighting the strength of the US business community even in the face of trade woes, the dollar could pare today’s losses.

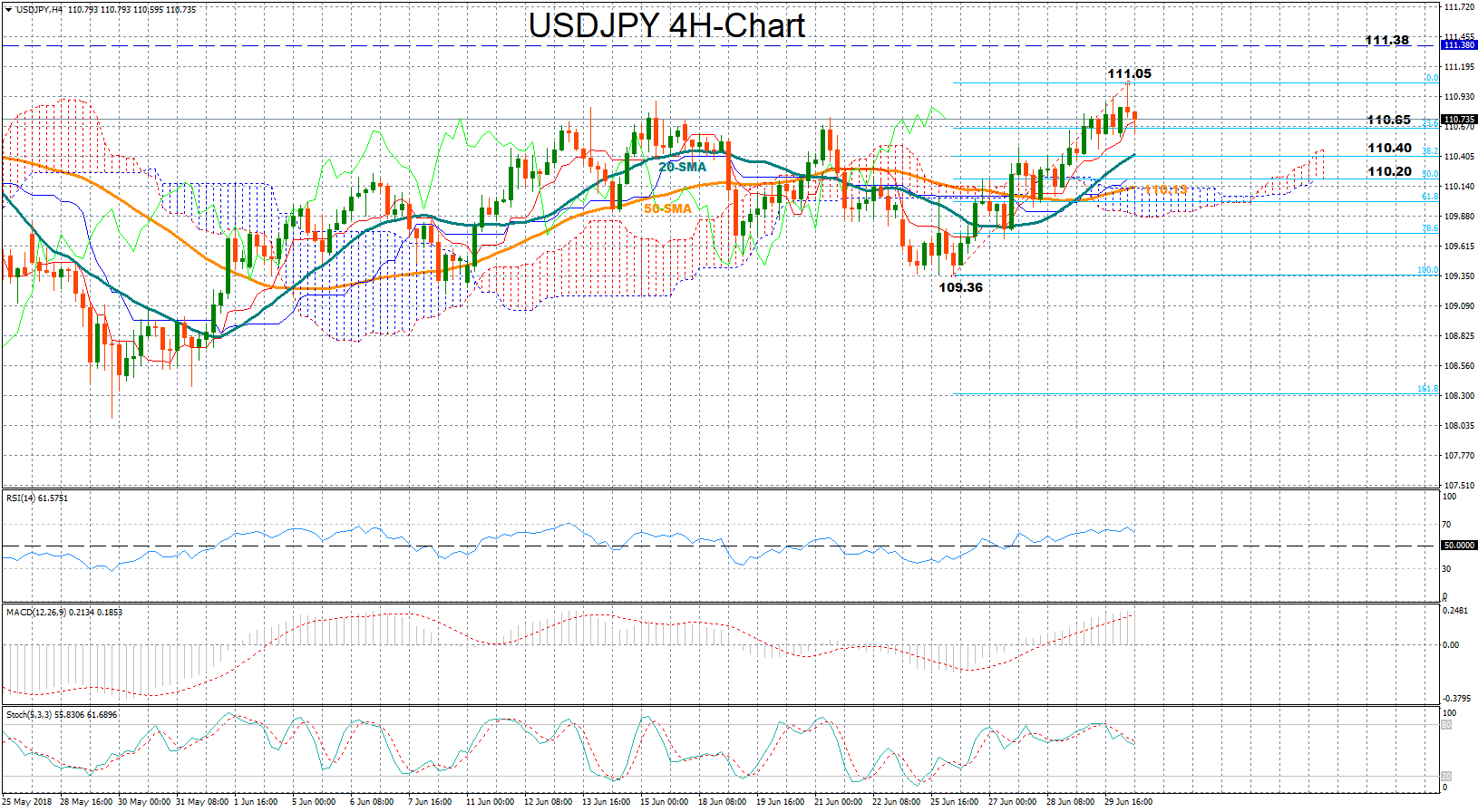

Technical Analysis: USDJPY hits six-week highs; momentum indicators lose steam

USDJPY managed to peak slightly above the 111-key level today to touch six-week highs, though the gains were not sustainable, and the pair returned down to the 110 handle as the RSI and the Stochastics signaled overbought in the four-hour chart. While the market continues to trade in an uptrend since June 26, momentum indicators suggest that the price might pause its uptrend in the short-term as the RSI and the MACD have slowed down, while the red Tenkan-sen line has also flattened above the blue Kijun-sen line.

Should the US ISM Manufacturing PMI or trade news disappoint, the market could move lower to meet the 23.6% Fibonacci of 110.65 of the upleg from 109.36 to 111.05. Even lower the 38.2% Fibonacci of 110.40, which overlaps with the 20-period simple moving average at the moment, could also act as a barrier given that the area caped upside movements last week. However, if this level fails to hold as well, then the focus could turn to the area between the 50% Fibonacci of 110.20 and the 50-period SMA at 110.13.

Alternatively, encouraging news out of the US could send the price back above the 111 key-level, with the bulls potentially aiming for a retest of May’s peak at 111.38.