{kind=link}

Here are the latest developments in global markets:

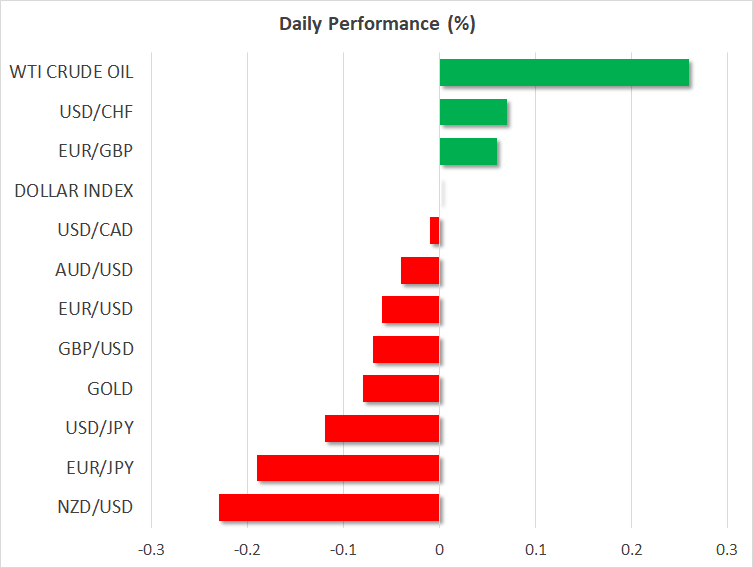

FOREX: The US dollar index – which tracks the greenback’s performance against a basket of six major currencies – is practically unchanged on Tuesday, after posting losses in the previous session. Meanwhile, the Japanese yen continued to enjoy some haven demand as trade frictions remained front and center.

STOCKS:Trade concerns triggered another selloff in US stocks on Monday. The Nasdaq Composite led the way lower (-2.09%), while the S&P 500 (-1.37%) and the Dow Jones (-1.33%) followed in its footsteps. US Treasury Secretary Mnuchin hinted that the upcoming investment restrictions against China may be applied to other countries as well, while Harley Davidson (-5.97%) said it would move some production overseas to avoid retaliatory EU tariffs. Asian equities, on the other hand, were mixed. Japan’s Nikkei 225 and Topix indices rose by 0.02% and 0.16% respectively. In Hong Kong, the Hang Seng was nearly unchanged (-0.01%), while in China, the CSI 300 fell 0.83%. In Europe, futures tracking all the major benchmarks are pointing to a positive open today. The same applies for US equity futures; the Dow, S&P, and Nasdaq are expected to open a little higher.

COMMODITIES: Oil prices are higher on Tuesday, recovering some of the losses from the previous session. WTI and Brent crude are higher by 0.3% and 0.2% respectively today, buoyed by supply disruptions in Canada and Libya. On the other hand, though, the escalating trade conflict between the US and China was casting a shadow on the robust forecasts for oil demand over the coming years, dragging prices lower yesterday. In precious metals, gold is down by nearly 0.1%, currently trading just above $1,264. The yellow metal continued to decline yesterday even despite the risk-off sentiment seen in other assets and a pullback in the US dollar; two factors that typically support gold.

Major movers: Risk aversion dominates as trade fears linger

Concerns regarding global trade remained the dominant market theme on Monday, diverting money flows away from riskier assets such as stocks and into perceived safe-havens, like the Japanese yen and US bonds. Major US stock indices closed the day notably lower, while dollar/yen touched a fresh two-week low of 109.35 and longer-term US Treasury yields declined somewhat.

The moves followed some conflicting signals from the White House. First came US Treasury Secretary Mnuchin, who ignited the first wave of risk aversion after saying via a tweet that any investment restrictions into the US will not be specific to China, but would apply to all countries “trying to steal our technology”. However, White House trade advisor Navarro soon told CNBC that there are “no plans to impose investment restrictions on any countries” and that “all we’re doing…is trying to defend our technology when it may be threatened”. He also characterized the negative market reaction as a “large overreaction”. Navarro’s remarks triggered a rebound in risk-sentiment, helping dollar/yen and US stock indices to spike higher on the news, though his optimism was not enough to calm investors as the recovery quickly faded and markets resumed their slide.

The negative sentiment was likely amplified by reports that trade fears are already starting to disrupt supply chains, after Harley Davidson said it would move production for European customers overseas to evade retaliatory tariffs on its products from the EU. Moving forward, trade developments could continue to dictate market action in the coming days. The next major announcement is likely to come on June 30, when the US is due to announce the specifics of its investment restrictions against China. Of utmost importance will be the extent of these restrictions, as well as how China chooses to respond.

Sterling/dollar was down by nearly 0.1%, while euro/sterling was up by roughly the same percentage, ahead of a crucial EU summit on Brexit that commences Thursday.

Elsewhere, the commodity-linked currencies reacted as one would expect amid boiling trade tensions; by moving lower. Kiwi/dollar is down by 0.2% and aussie/dollar by 0.05%, both extending losses from yesterday.

Day ahead: Trade and politics in focus; CaseShiller house price data and consumer confidence figures due out of the US

Tuesday’s economic calendar does not feature much in terms of releases, with some data on house prices and consumer confidence being due out of the US. It appears that developments on the trade front, as well as political deliberations in Germany, have greater potential to move the markets rather than any of today’s releases.

The CaseShiller indices gauging house prices in the US during the month of April will be made public at 1300 GMT, while the Conference Board will be releasing data on June’s consumer confidence at 1400 GMT. Consumer sentiment as measured by the relevant index is anticipated to stand at 128.0, remaining unchanged relative to May’s print.

Trade tensions continue to rank high in terms of investor focus, with market participants turning their attention to the Trump administration’s trade and investment restrictions, as well as any retaliatory actions by trading partners of the US that could further escalate the situation, triggering a flight to safety at the expense of riskier assets such as stocks. Among others, a US Treasury release relating to technology investment restrictions will be closely watched.

Meanwhile, German Chancellor Angela Merkel will be holding talks with the leaders of the other parties in her coalition government, touching on euro-area reforms and immigration policy; the latter is seen as posing threats to her government.

Among policymakers making appearances on Tuesday are Dallas Fed President Robert Kaplan (1745 GMT – non-voting FOMC member in 2018), Atlanta Fed President Raphael Bostic (1715 GMT – voting FOMC member in 2018) and ECB Vice President Luis de Guindos (1200 GMT).

In energy markets, weekly API data on crude oil stocks are due at 2030 GMT.

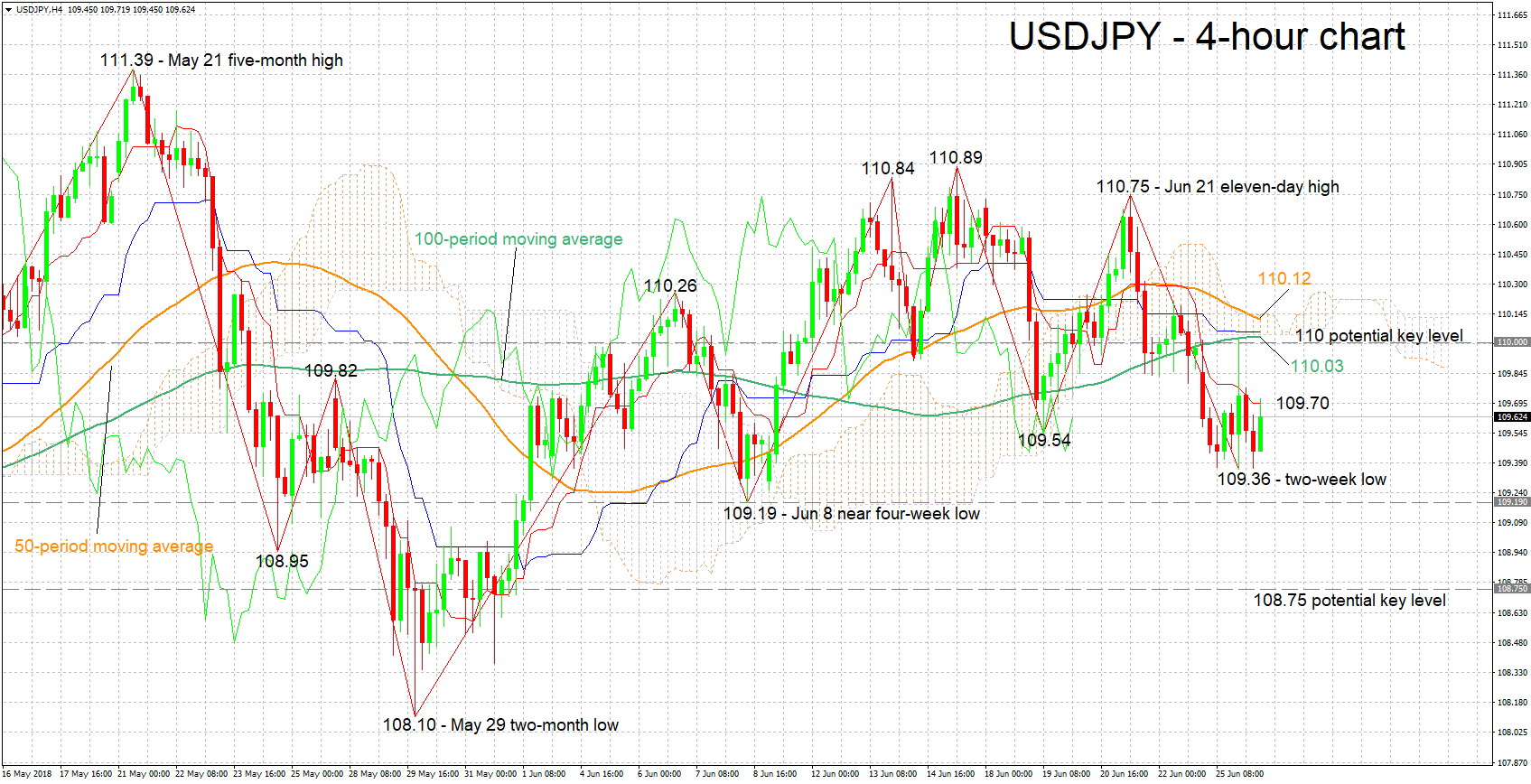

Technical Analysis: USDJPY bearish bias eases

USDJPY has gained some ground after reaching a two-week low of 109.36 during Monday’s trading. The bias remains to the downside as indicated by the negatively-aligned Tenkan- and Kijun-sen lines, though bearish momentum appears to have eased – this is also signaled by the flat Kijun-sen.

Intensifying trade tensions are likely to see the yen attracting safe-haven flows, thus weighing on USDJPY. Yesterday’s two week low of 109.36 may provide support to declines, with the near four-week low of 109.19 from June 8 lying not far below. Sharper declines will turn the attention to the region around 108.75 which experienced some congestion between late May and early June.

Easing tensions on the other hand are likely to boost USDJPY. Immediate resistance seems to be taking place around the current level of the Tenkan-sen at 109.70, with the focus next turning to the zone around the 110 round figure, which includes the current levels of the 50- and 100- period moving average lines (at 110. 12 and 110.03 respectively), as well as the Kijun-sen (110.06), and the Ichimoku cloud bottom (110.04) and top (110.14).

Consumer confidence data due out of the US can also lead to positioning on the pair.