{kind=link}

The US dollar is mixed against major pairs. Safe havens like the Swiss franc, Japanese yen and the euro have gained against the greenback, while the Canadian and New Zealand dollars along with the pound are lower. Strong data in Europe boosted the single currency but the rally was short lived after the Trump administration announced a review of US-EU trade that could result in a 20 percent tariff on European car imports. Oil prices surged after the Organization of the Petroleum Exporting Countries (OPEC) and other major producers agreed to increase supply at the end of their collective meeting in Vienna. The Canadian dollar became the worst performer against the US dollar as inflation and retail sales disappointed on Friday.

- US consumer confidence forecasted to slow down

- BOE Carney to announce bank stress test results

- BOC to publish its quarterly business outlook survey

EUR Higher After Strong PMIs Held Back by Trade Concerns

The EUR/USD rose 0.32 percent on Friday. The single currency is trading at 1.1640 after scoring early gains versus the USD with the release of flash PMI data in Europe. German and French service Purchasing Manager’s Indices (PMIs) were higher than expected, but manufacturing indicators suffered slight setbacks. The European data reflected those moves with a 55 Services PMI and a slight decrease on manufacturing with a 55 reading.

The news of a potential 20 percent tariff on European cars was announced by US President Donald Trump on Friday. The EUR responded to the news by moving lower, but still close to the 1.1630 price level. The US will start a probe on auto tariffs on July 19. European stock markets were in positive territory as the tariffs are subject to a review but slowed down the momentum the EUR rally ahead of the weekend.

The European calendar will feature the German Ifo business climate on Monday, German inflation data on Thursday and closing the week with German retail sales and EU inflation estimates. In North America the calendar will have the release of the consumer confidence survey by the Conference Board on Tuesday, US durable goods on Wednesday, US final GDP and unemployment goods on Thursday. Canadian data will be in the spotlight on Friday with the release of the monthly GDP and the business outlook survey from the Bank of Canada (BoC).

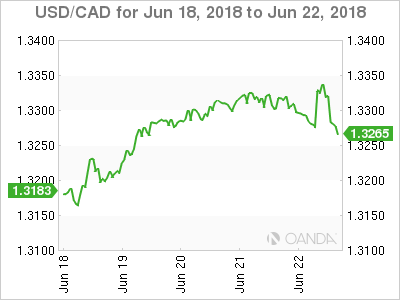

Loonie Hits 1 year Low vs Dollar

The USD/CAD was higher on Tuesday. The pair climbed 0.19 percent trading at 1.3337 after the release of Canadian inflation and retail sales. The consumer price index (CPI) disappointed with a 0.1 percent gain, while retail sales contracted by 0.1 percent. Both indicators had more optimistic forecasts. The loonie is struggling to advance versus the USD as the uncertainty surrounding NAFTA and softer economic indicators have put the currency on the back foot. The Bank of Canada (BoC) could hike rates to a void a decline of the currency, but the central bank has to balance the potential impact of higher interest rates on households that are holding record debt levels.

A rate hike in July decreased in probabilities with the inflation miss. The chances were higher given the Canadian central bank tries to keep the gap between the Fed funds rate and its own benchmark from getting too wide. The 25 basis points earlier this month by the U.S. Federal Reserve put some pressure on the BoC with investors anticipating a move in July.

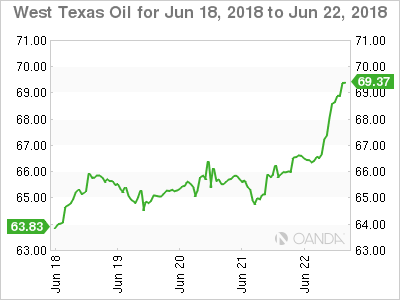

Oil Rises as Output Deal Lower Than Expected

Saudi Arabia was able to broker a deal with the other Organization of the Petroleum Exporting Countries (OPEC) members and major producers to increase daily oil production by 1 million barrels per day. The move was praised by US President Donald Trump who tweeted for more increases as it will keep the price of crude down. Iran was not backing the move into higher supply limits, but backed off from blocking the deal during the meeting in Vienna. The majority of the increase will come from OPEC members, at around 70 percent with Russia and others adding the rest. Despite higher supply levels the market took the news of the agreed increase as a positive for oil prices.

The deal to increase production was lower than expected after the OPEC and major producer agreement to limit production has been one of the major factors in the stability of crude prices. The fact that the organization remained united was a positive for oil prices despite higher supply. Demand is showing some signs of recovery, and the disruptions in Iran, Venezuela and Libya will keep the black stuff bid.

Market events to watch this week:

Tuesday, June 26

- 10:00am USD CB Consumer Confidence

- 9:00pm NZD ANZ Business Confidence

Wednesday, June 27

- 4:30am GBP BOE Gov Carney Speaks

- 8:30am USD Core Durable Goods Orders m/m

- 10:30am USD Crude Oil Inventories

- 3:00pm CAD BOC Gov Poloz Speaks

- 5:00pm NZD Official Cash Rate

- 5:00pm NZD RBNZ Rate Statement

Thursday, June 28

- 8:30am USD Final GDP q/q

Friday, June 29

- 4:30am GBP Current Account

- 8:30am CAD GDP m/m

- 10:30am CAD BOC Business Outlook Survey

*All times EDT