{kind=link}

OPEC, JMMC meetings are taking place today in Vienna with agreement on production levels high on the agenda. This can impact on prices in Oil markets.

Eurogroup meeting are also taking place today in Brussels increasing headline risk in the EUR crosses.

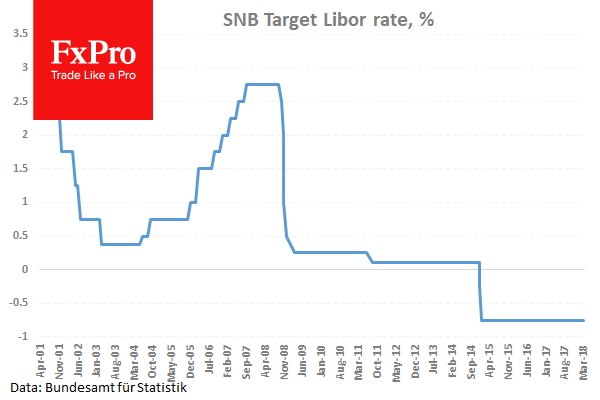

At 07:30 GMT, SNB Interest Rate Decision and Monetary Policy Assessment are due to be released. The Interest is expected to be left unchanged at -0.75%. This event will set the tone for subsequent moves in CHF crosses as the markets interpret the Banks policy for the future. A press conference will follow at 08:30 GMT.

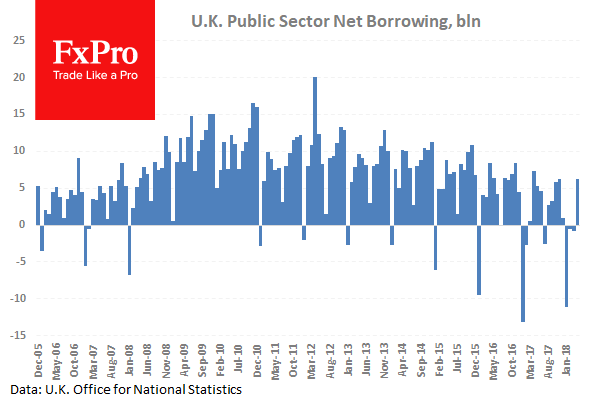

At 08:30 GMT, UK Public Sector Net Borrowing (May) is expected to be £5.000B against a previous £6.23B. This is expected to show a smaller deficit than the previous month. GBP crosses may react to this data release.

At 09:45 GMT, German Buba President Weidmann is due to speak about monetary policy challenges for the euro, at a jointly held conference by the Bank of France and Bundesbank, in Paris. EUR crosses may be moved by any comments made in relation to Central Bank policy.

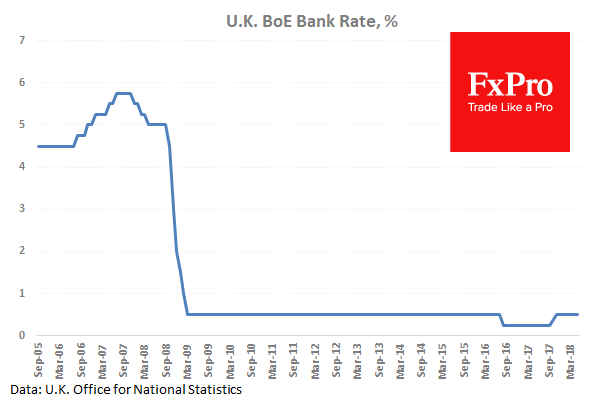

At 11:00 GMT, Bank of England Interest Rate Decision is expected to be left unchanged at 0.5%. The BOE Minutes, BOE Quarterly Inflation Report and the Monetary Policy Statement will be released at the same time. BOE Asset Purchase Facility is expected to come in at £435B, unchanged from £435B previously. While no change in rate is expected the tone and language used will be examined for hints that the Bank is gearing up to increase rates in future, with the market focusing on an August Rate Hike. GBP crosses can see spikes in volatility during this event.

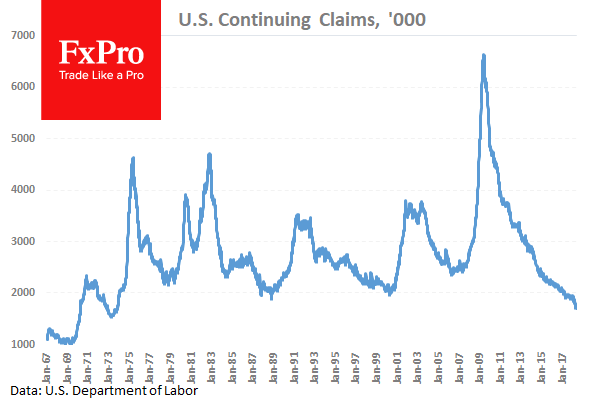

At 12:30 GMT, US Continuing Jobless Claims (Jun 8) is expected to be 1.730M against 1.7697M previously. Initial Jobless Claims (June 15) is expected to come in at 220K against 218K previously. This data is showing that the number of new claims is stable but continuing claims is continuing to fall as workers are recruited to jobs.

Philadelphia FED Manufacturing Survey (Jun) is expected to be 29.0 against 34.4 previously. This data surprised to the upside last month beating the expected 21.1. USD crosses can see an increase in volatility from this data release.

At 13:00 GMT, US House Price Index (MoM) (Apr) is expected at 0.3% from 0.1% previously. This data is expected to increase from last month’s reading after declining strong reading in January of 0.8%. A fall under 0.0% would be of concern since the data has remained above that level since 2011.

At 20:15 GMT, UK BOE Governor Mark Carney is due to speak at the Mansion House dinner, in London. GBP volatility can increase during this event.