{kind=link}

Here are the latest developments in global markets:

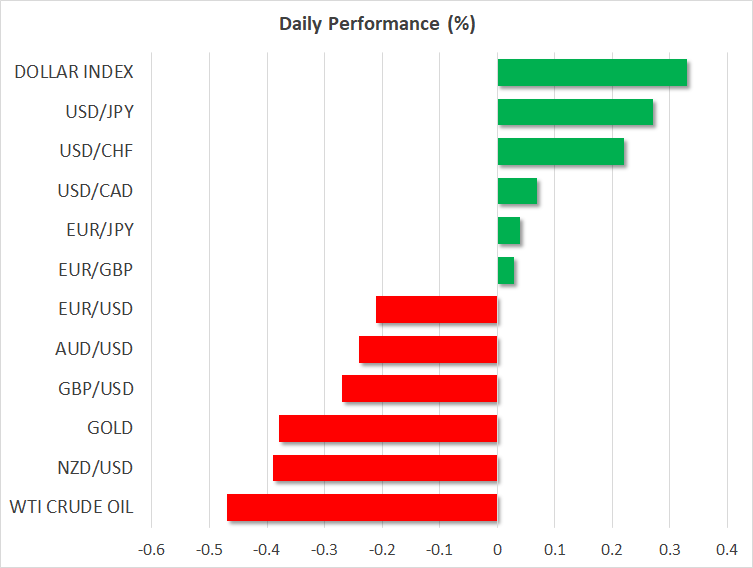

FOREX: The US dollar index is 0.3% higher on Thursday, touching a fresh high for 2018. Safe-haven currencies such as the yen and the Swiss franc are on the back foot, down by nearly 0.3% and 0.2% respectively against the greenback as trade concerns have moved to the background for now. Commodity-linked currencies like the loonie, aussie, kiwi, are also on the retreat, with the first two trading at one-year lows versus the dollar.

STOCKS:US markets closed mixed on Wednesday. The Nasdaq Composite rose 0.72%, bringing the tech-heavy index to a fresh all-time high, propelled higher by the likes of Facebook (+2.3%) and Netflix (+2.9%). Meanwhile, the S&P 500 managed to gain 0.17%, but the Dow Jones fell by the same percentage. Futures tracking the Dow, S&P, and Nasdaq 100 are also pointing to a higher open today. Markets in Asia, though, were mostly in the red. Japan was mixed, as the Nikkei 225 climbed by 0.61% while the Topix fell 0.12%. In Hong Kong, the Hang Seng dropped by 1.23%. Finally in Europe, futures suggest that all but one of the major indices are set to open higher today. The only exception is the German DAX 30.

COMMODITIES: Oil prices are lower on Thursday, amid signals that the ‘resistance’ to raise OPEC production this week is fading. WTI is down by almost 0.5% and Brent by 0.9%, following comments from Iran’s oil minister on Wednesday that his nation could compromise and agree to a small increase in OPEC output – something he had ruled out in previous days. So the conversation now appears to have shifted from whether or not there will be an increase, to how much that increase will be, weighing on prices. In precious metals, gold is down by 0.4% on Thursday, touching fresh lows for 2018 as a stronger US dollar is exerting downward pressure on the dollar-denominated metal. The fact that even the increasingly realistic risk of an ‘all out’ US-China trade war was unable to lift gold suggests that buyers are in short supply right now, and unless tensions escalate much further or the US dollar reverses course, the current pattern may continue.

Major movers: Dollar touches fresh highs; safe-havens on the defensive

The US dollar index reached an 11-month high during the Asian trading session Thursday, drawing strength from an uptick in longer-term US Treasury yields, as well as a broad tumble in commodity-linked and safe-haven currencies.

In euro land, the common currency came under renewed pressure yesterday, after ECB Governing Council member Ewald Nowotny said that the divergence between ECB and Fed policy will probably have an impact on the exchange rate. His remarks were perceived as a soft ‘jawboning’ of the euro.

Meanwhile, media reports suggest the ECB is ‘growing increasingly concerned that a looming trade war could derail the euro zone’s recovery’. Although to a lesser extent, a similar sentiment was echoed yesterday by the heads of the Fed, ECB, and BoJ at the ECB’s conference in Sintra, Portugal. All three noted that boiling trade tensions could have implications for monetary policy, implicitly suggesting such risks could slow their respective paths towards normalization.

Staying on trade, the ‘trade war’ narrative appears to have moved to the background for now, as markets remained in recovery-mode yesterday. US stock markets closed mostly higher, while havens like the yen and the franc retreated alongside gold. A similar pattern appears to be in the works on Thursday, as the yen is already down by nearly 0.3% against the dollar, while US stock futures are pointing to a higher open.

The exception to this modest recovery have been the commodity-linked currencies – the loonie, aussie, and kiwi. The loonie touched fresh one-year lows versus the dollar even despite relatively stable oil prices and optimistic comments from US Commerce Secretary Ross that he expects NAFTA to be renegotiated soon. The tide may turn with tomorrow’s CPI data out of Canada. A strong set of prints could lead investors to fully factor in a BoC rate hike in July, currently priced in with a 66% probability, and thereby help the loonie to rebound.

In the UK, PM Theresa May scored a ‘victory’ yesterday, as the bill that would have given Parliament a meaningful vote on the final Brexit deal was defeated via a 319-303 vote. Cable jumped on the outcome, but quickly came back down to touch fresh lows for the year amid broad dollar-demand. Focus now turns to the BoE policy decision today.

Day ahead: Bank of England decides; SNB and Norges Bank also on the agenda; US jobless claims and eurozone consumer confidence due

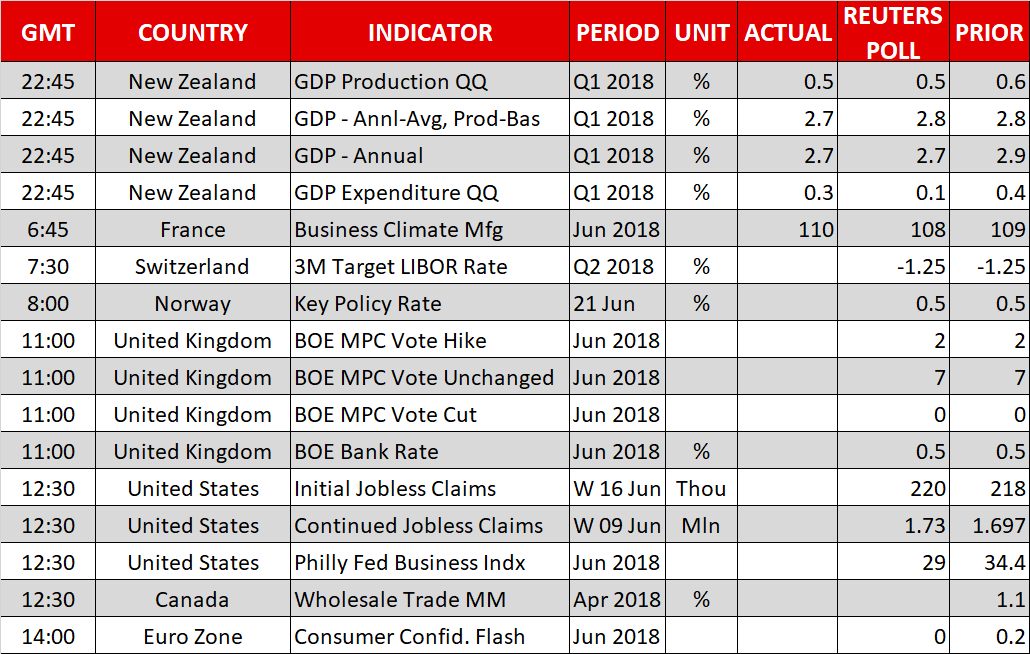

The highlight out of Thursday’s calendar is the Bank of England (BoE) rate decision. Beyond this and in terms of releases, jobless claims figures are on the agenda out of the US, while the eurozone will be on the receiving end of data on consumer sentiment. Meanwhile, the Swiss National Bank (SNB) and Norges Bank will also be completing their respective meetings on monetary policy.

The Bank of England’s rate decision and meeting minutes are scheduled for release at 1100 GMT, with the Bank widely expected to hold its policy rate unchanged at 0.5%. Given that the current meeting does not feature a press conference by Governor Carney or updated growth and inflation forecasts, the Monetary Policy Committee (MPC) members’ language in the meeting’s minutes is likely to drive positioning on sterling pairs. Specifically, the attention will fall on what the Bank’s policymakers will signal regarding upcoming meetings and in particular the one in August. Market participants are assigning a 31% probability for a 25bps interest rate rise during that meeting according to UK overnight index swaps. Should policymakers stoke the odds for such an outcome, then the British pound is expected to post some gains relative to other currencies; the opposite holds true as well.

Overall, the risk may be tilted to the downside for the pound, as the recent largely soft patch of data, in conjunction with uncertainties over Brexit, may cause MPC members to strike a cautious tone in their assessment of the economy.

Meanwhile, the SNB (0730 GMT) and the Norges Bank (0800 GMT) will also be deciding on monetary policy today. Similar to the BoE, they’re projected to maintain to hold their policies unchanged. News conferences will follow after the decisions of the two central banks are made public.

US weekly jobless claims data are due at 1230 GMT, with June’s Philly Fed Business Index scheduled for release at the same time.

Also at 1230 GMT, Canadian wholesale trade data for April will be hitting the markets.

Out of the eurozone, the European Commission’s Directorate General for Economic and Financial Affairs will release its flash consumer confidence figure for June at 1400 GMT; consumer morale in the euro area as gauged by the indicator is anticipated to fall to zero from 0.2 in May.

UK Finance Minister Philip Hammond and BoE Governor Carney will be making their Mansion House speeches on Thursday; the latter will be giving a speech at 2015 GMT. Some remarks on monetary policy by Bundesbank chief Jens Weidmann at 0945 GMT will also be attracting interest.

A eurozone finance ministers meeting (1500 GMT) that is to decide, among others, on possible new debt relief measures for Greece might generate attention.

Lastly, it should be stressed that trade developments remain in the background and could spur volatility in case of any updates.

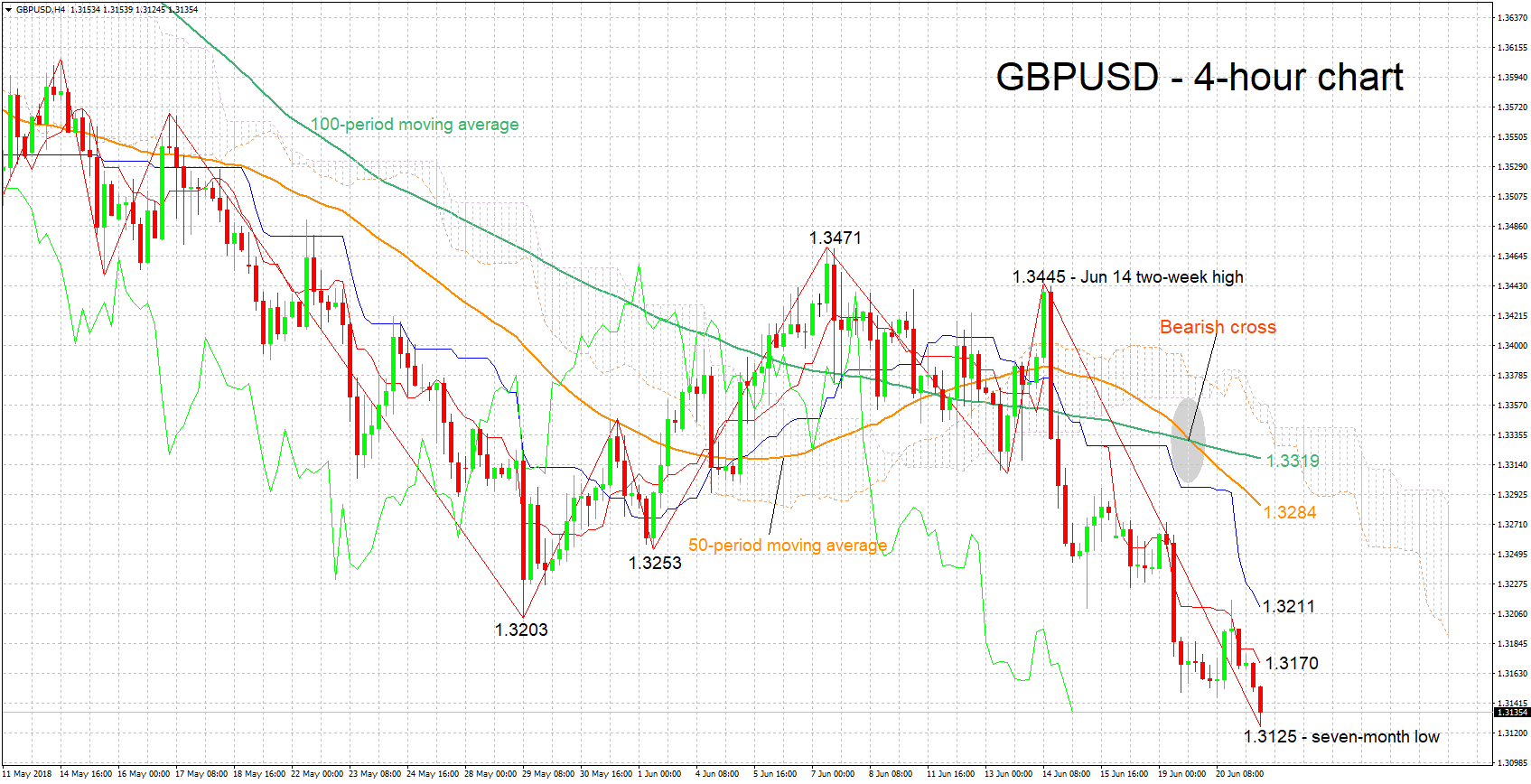

Technical Analysis: GBPUSD bearish at 7-month low; possibly oversold

GBPUSD has declined considerably after hitting a two-week high of 1.3445 around mid-June. Earlier on Thursday, it recorded a fresh seven-month low of 1.3125. The short-term picture is bearish as also evidenced by the negatively-aligned Tenkan- and Kijun-sen lines. The Chikou Span, however, may be pointing to an oversold market; a reversal in the near-term should not be ruled out.

A hawkish Bank of England later on Thursday is expected to boost the pair. Resistance to gains could come around the current levels of the Tenkan- and Kijun-sen lines at 1.3170 and 1.3211 respectively; the region around the latter also encapsulates the 1.32 round figure, as well as a bottom from late May at 1.3203.

On the downside and in case of a cautious BoE that exerts selling pressure on GBPUSD, support could be met around 1.31 and subsequently – and in case of sharper losses – the 1.30 handle.