{kind=link}

The Bank of England will be completing its meeting on monetary policy on Thursday, with its rate decision and meeting minutes scheduled for release at 1100 GMT. In the meantime, Brexit is again in the spotlight, having policy implications and thus the capacity to move the British currency.

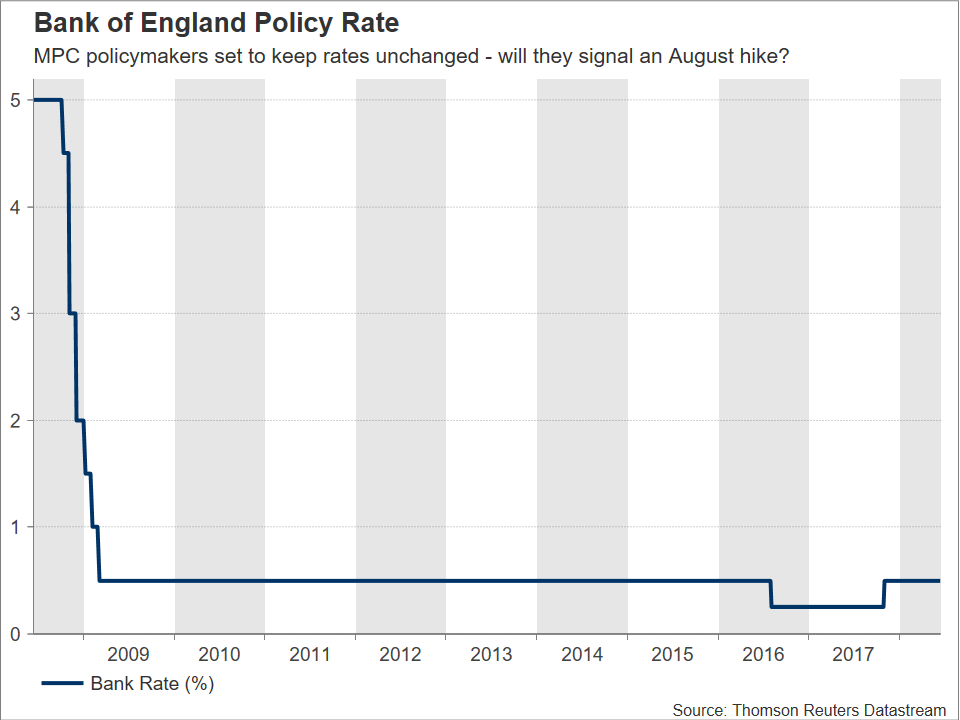

The BoE is widely anticipated to hold its policy rate unchanged at 0.5% upon conclusion of this week’s meeting on monetary policy. The upcoming meeting does not feature a press conference by Governor Carney or updated growth and inflation forecasts. Thus, the Monetary Policy Committee (MPC) members’ language in the meeting’s minutes accompanying the rate decision is expected to drive positioning on sterling pairs.

Market expectations are for two out of nine MPC members – Ian McCafferty and Michael Saunders – the “usual suspects” – to vote in support of a hike during Thursday’s meeting, with the remaining voting for rates to be kept unchanged. The question is what to expect from the August meeting? Market participants are assigning a 37% probability for a 25bps interest rate rise during that meeting according to UK overnight index swaps. The odds for such an outcome though, will be highly dependent on signaling by BoE policymakers as reflected in the upcoming meeting’s minutes.

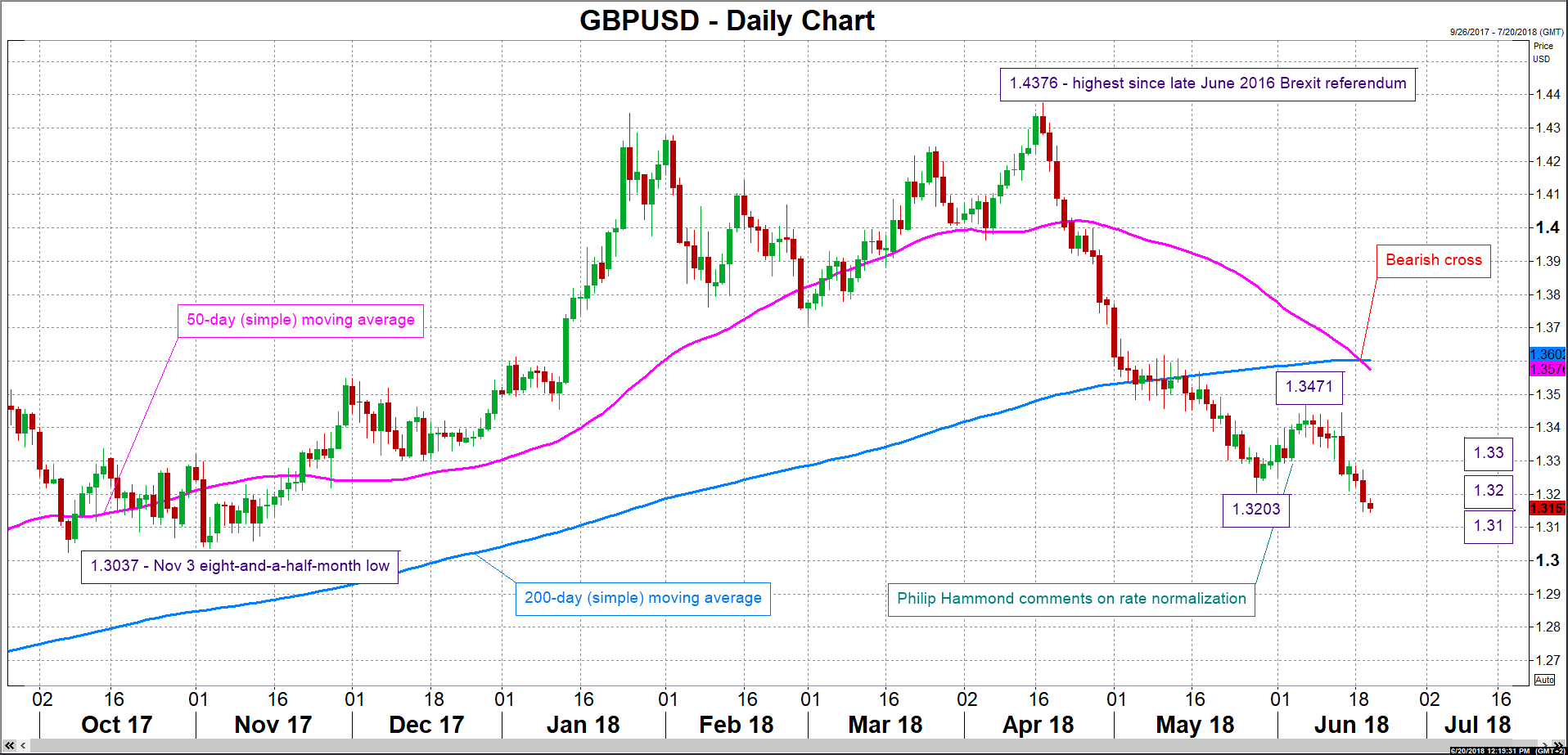

Should policymakers appear confident about the economy, indicating an August rate increase, then a stronger British pound relative to other currencies is likely to emerge. Focusing on GBPUSD, an appreciating pair could meet resistance around the 1.32 and 1.33 round figures. Conversely, a cautious BoE that pushes rate normalization projections further away into the future, is expected to exert selling pressure in the pound/dollar pair. Initial support to declines might come around the 1.31 handle which constituted an area of congestion in late 2017. Steeper losses would shift the focus to 1.3037, this being an eight-and-a-half-month low recorded in early November.

Overall, the risk may be tilted to the downside for the pound, as the recent largely soft patch of data may cause MPC members to strike a cautious tone in their assessment of the economy. Indicatively, last week’s industrial production data showed output contracting by 0.8% on a monthly basis in April, this constituting the largest fall since December and coming in far worse than analysts had forecast. A bright spot were May’s retail sales, but the boost in sales is likely to prove transitory, as it is seen as partially coming on the back of the “wedding effect” – a spending spree fueled by Prince Harry’s wedding to Meghan Markle.

On top of the aforementioned, uncertainty over Brexit and the government’s future is further complicating the situation for the BoE and perhaps lends credence to a cautious stance. In this respect, a crucial vote will take place in the House of Commons later on Wednesday that has the potential to derail PM Theresa May’s Brexit plans and cast fresh doubts on her leadership, adding an additional layer of uncertainty over the UK’s outlook. Market anxiety is perhaps also evidenced by sterling’s recent losses, with GBPUSD touching a seven-month low of 1.3246 earlier on Wednesday.

Still, even if the BoE indeed appears on the cautious side of the spectrum, it may also opt to keep its options open as regards a hike in August. If this turns out to be the case, then such an action may prove as damage control of some sorts for sterling.

Meanwhile, UK Finance Minister Philip Hammond and Governor Carney will be making their Mansion House speeches on Thursday. It is worth noting that the former noted in early June that “there is clearly scope for the Bank of England gradually and carefully to normalize interest rates over time”. His comments were pound-positive (see GBPUSD chart).