{kind=link}

For the 24 hours to 23:00 GMT, the EUR declined 0.28% against the USD and closed at 1.1589.

On the economic front, Euro-zone’s seasonally adjusted current account surplus narrowed more than expected to €28.4 billion in April, compared to a surplus of €32.0 billion in the prior month and marking its lowest level since June 2017. Markets were expecting trade surplus to narrow to £30.3 billion. Meanwhile, the region’s seasonally adjusted construction output unexpectedly rose 1.8% on a monthly basis in April, after recording a revised fall of 0.2% in the previous month.

Macroeconomic data released in the US indicated that housing starts jumped 5.0% on a monthly basis, to an annual rate of 1350.0K in May, hitting a 11-year high level and more than market consensus for a rise to a level of 1311.0K. Housing starts had recorded a revised reading of 1286.0K in the previous month. Also, the nation’s building permits fell by 4.6% on a monthly basis, to an annual rate of 1301.0K in May, compared to a revised reading of 1364.0 K in the prior month and marking its lowest level since September 2017. Market anticipation was for building permits to fall to a level of 1350.0 K.

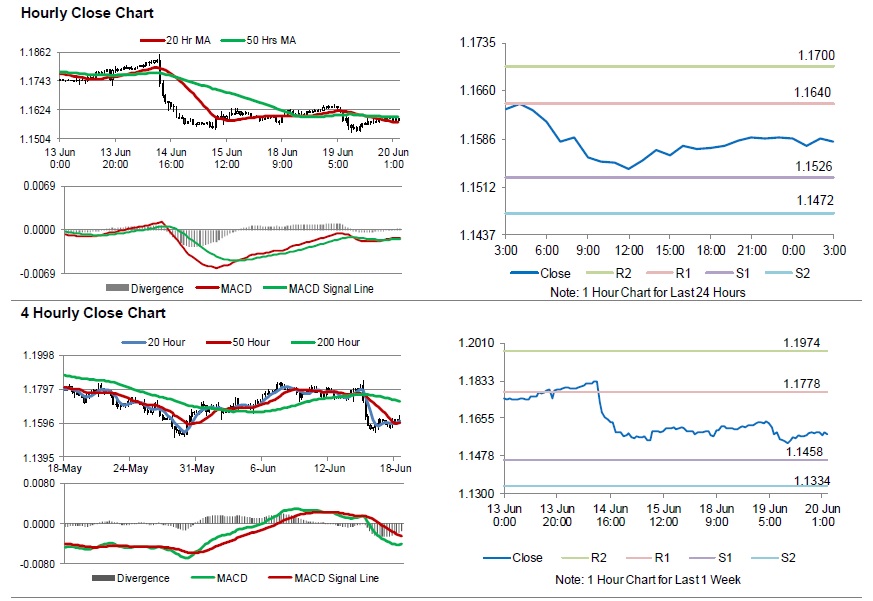

In the Asian session, at GMT0300, the pair is trading at 1.1581, with the EUR trading 0.07% lower against the USD from yesterday’s close.

The pair is expected to find support at 1.1526, and a fall through could take it to the next support level of 1.1472. The pair is expected to find its first resistance at 1.1640, and a rise through could take it to the next resistance level of 1.1700.

Moving ahead, investors would look forward to Germany’s producer price index for May scheduled to release in a few hours. Moreover, the US MBA mortgage applications followed by existing homes sales data for May, set to release later in the day, will be on investors’ radar. The currency pair is trading above its 20 Hr and showing convergence with its 50 Hr moving average.