{kind=link}

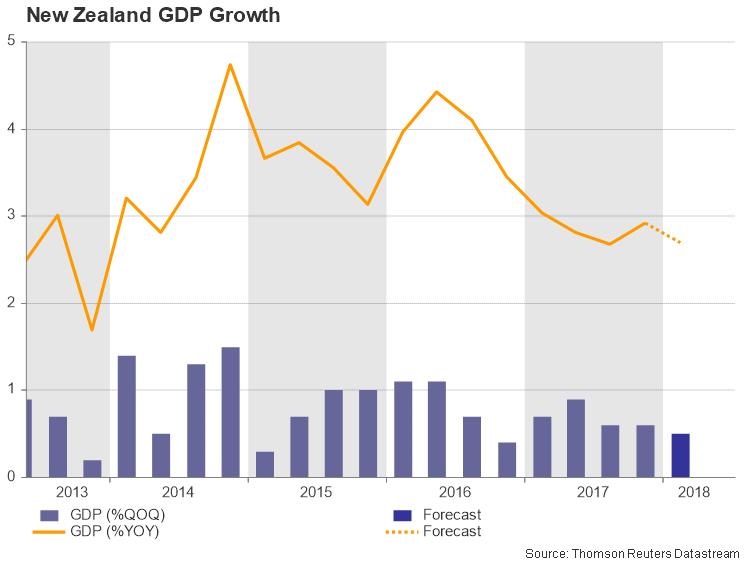

New Zealand will publish GDP figures on Thursday (Wednesday 2245 GMT) for the first quarter. Investors will be cautious for any clues as to whether the Reserve Bank of New Zealand (RBNZ) will raise or decrease interest rates. Economic growth is expected to have slowed down further in the first quarter of 2018.

Analysts are estimating New Zealand’s economy grew by just 0.5% in the three months to the end of March, easing slightly from the previous two quarters of 0.6%. On an annual basis, GDP is expected to have expanded by 2.7% versus 2.9% in the preceding period. The data are unlikely to change the RBNZ’s view and a more disappointing release would endorse the scenario for another cut in rates rather than an increase for the near future.

Turning to monetary policy, the central bank kept its official cash rate unchanged at a record low of 1.75% on May 10, as widely expected. The last change in key rate was in November 2016. Policymakers highlighted that inflation remains below the 2% mid-point of the target due to recent low food and import price inflation, as well as subdued wage pressures. Meanwhile, inflation advanced by 1.1% y/y in the first three months of this year versus a 1.6% y/y increase in the previous quarter, matching market expectations. This figure was the slowest since the third quarter of 2016. It is worth mentioning that the unemployment rate ticked lower to 4.4% in Q1 from 4.5% before. This was the fifth consecutive quarter the unemployment rate has fallen and was the lowest number since the last quarter of 2008.

On the political front, US President Donald Trump’s trade war could have a negative effect on New Zealand and its currency. Trump has put a hefty tariff on Chinese imports and China has retaliated by imposing tariffs of their own. The country is already seeing impacts from the steel and aluminum exports, where tariffs were brought in earlier in 2018. The New Zealand dollar is moving sharply lower and could fall even more in case of worse-than-expected data.

From the technical point of view, kiwi/dollar has slipped more than 2% since last week, recording a fresh three-week low of 0.6883. The strong sell-off rally started after the pullback on the 0.7050 resistance level, while the moving averages are following the bearish structure in the short-term.

If GDP numbers surpass the consensus then the expectation is a run until the 20-SMA near 0.6940 at the time of writing. A break above the aforementioned obstacle could open the door towards the next barrier of 0.6955 taken from the significant top on June 18.

A worse-than-expected figure could continue the downward pressure for the pair and would retest the latest low of 0.6881. Further losses could drive kiwi/dollar until the 0.6870 support before being able to re-challenge the 0.6850 region. In case of steeper decreases, the next support to have in mind is the 0.6820 barrier, taken from December 8 low.