{kind=link}

The US dollar is higher against major currencies on Tuesday after American inflation came in better than expected ahead of the eagerly anticipated Federal Open Market Committee (FOMC) two day meeting. A 25 basis points rate hike has been priced in for months with the CME FedWatch showing a 96.3 percent probability of a lift on Wednesday. Fed Chair Jerome Powell will face the financial press at 2:30 pm EDT. There will be plenty of questions aimed at Powell with international trade top of mind, but also his views on inflation and the growth of the economy. The market forecasts at least another rate hike in 2018 with the fate of a fourth lift in interest rates up in the air.

- US central bank expected to hike rates on Wednesday

- Fed Chair Powell could discuss having a press conference after every FOMC

- US oil inventories expected to shrink by 1.4M barrels

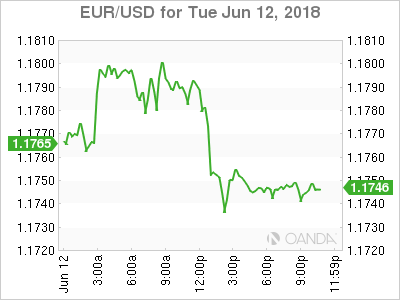

US Dollar Steady Ahead of Fed Statement

The EUR/USD lost 0.35 percent in the last 24 hours. The single pair is trading at 1.1740 with the Fed anticipated to hike the cost of borrowing higher up to the 175–200 basis points range. US fundamentals have recovered form the rocky start to 2018, but geopolitical headwinds remain. US President Trump scored a huge international policy win by meeting with North Korean Leader Kim that ended in bilateral promises to end US military exercises in exchange for denuclearization of NK’s arsenal.

The trade front is another story with the recently ended G7 meeting in Canada ending in the US standing apart from other members with a looming trade war in the horizon. The ECB could tighten monetary policy on Thursday following the actions from the U.S. Federal Reserve. The rate lift by the US central bank has already been priced in which is why it won’t drive the USD higher.

The ECB in contrast has been less clear with its monetary policy intentions. EUR/USD flows indicate a belief that with the Fed tightening on Wednesday it can offer a further monetary policy signal and make a clear indication it will end its QE program this year opening the possibility of an European rate hike in 2019. The European central bank does have some time to ponder the decision as it will meet again in July.

The Fed and the ECB could collectively make a statement on their confidence on the strength of their respective economies. While the central banks might be on the same page things are different on the political arena. US President Donald Trump was again on the trade offensive ahead of the G7 meetings. The US risks being isolated from other major economies if the tone continues to be so combative. The US has opened various fronts which will tax its ability to deal effectively with so many concurrent negotiations on top of growing issues of national importance.

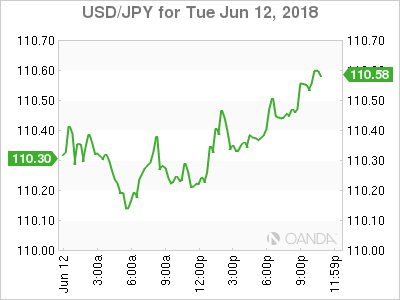

Yen Falls as Risk Aversion Subsides

The USD/JPY rose 0.38 percent on Tuesday. The currency pair is trading at 110.45 ahead of the rate decision announcement by the U.S. Federal Reserve on Wednesday. The dollar has gained as risk aversion has ebbed after a shaky G7 meeting in Canada. The meeting in Singapore between the US and North Korea while light on details was a win for diplomacy. Japanese fundamentals have been soft with inflationary once again underperforming despite the commitment from the Bank of Japan (BOJ).

The Japanese central bank is also scheduled to issue a statement this week, but there is no monetary policy changes anticipated. BOJ Governor Haruhiko Kuroda has already removed the end date of the massive quantitative easing program. The contraction of the Japanese economy in the first quarter of the year and the rise in trade war concerns will keep the central bank from tweaking its current plans. The good news is a rise in internal consumption and given the hard to read statements from the US, Japan has already started to look into other partnerships to offset the potential losses from American tariffs.

The JPY has been a favoured currency in times of turmoil. Its status as a safe haven remains high specially since the US has become a source of instability. With Trade spats and the Eurozone dealing with internal threats and Brexit, the yen has risen despite the efforts of the BoJ and is up more than 2.02 percent against the USD year to date.

Market events to watch this week:

Tuesday, June 12

10:00pm AUD RBA Gov Lowe Speaks

Wednesday, June 13

4:30am GBP CPI y/y

8:30am USD PPI m/m

10:30am USD Crude Oil Inventories

2:00pm USD FOMC Economic Projections

2:00pm USD FOMC Statement

2:00pm USD Federal Funds Rate

2:30pm USD FOMC Press Conference

9:30pm AUD Employment Change

Thursday, June 14

4:30am GBP Retail Sales m/m

7:45am EUR Main Refinancing Rate

8:30am EUR ECB Press Conference

8:30am USD Core Retail Sales m/m

8:30am USD Retail Sales m/m

Midnight JPY BOJ Policy Rate

Midnight JPY Monetary Policy Statement

Friday, June 15

Tentative JPY

BOJ Press Conference