{kind=link}

Here are the latest developments in global markets:

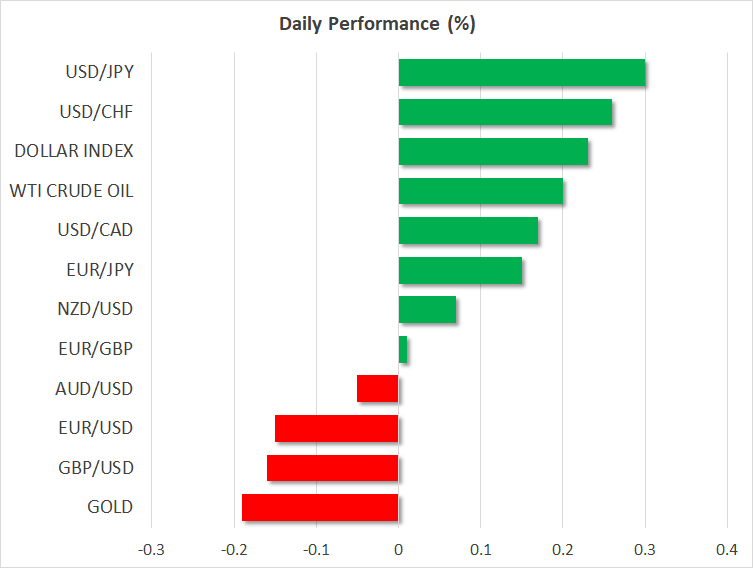

FOREX: The US dollar index is 0.2% higher on Tuesday, ahead of the release of the US inflation data for May and as the Fed kicks off its two-day policy gathering. Meanwhile, the yen is on the back foot as the encouraging outcome in the Donald Trump – Kim Jong-un meeting is supporting risk appetite and diverting flows out of haven assets.

STOCKS: Wall Street indices closed higher on Monday, though the gains were short of impressive. The Nasdaq Composite climbed by 0.19% while the S&P 500 rose by 0.11%. Even the Dow Jones managed to eke out a 0.02% gain. Futures tracking the Dow, S&P, and Nasdaq 100 are all currently pointing to a higher open today as well, something likely owed to the upbeat outcome of the Trump – Kim meeting. In Japan, both the Nikkei 225 and the Topix gained 0.33% on the back of a softer Japanese yen, while in Hong Kong, the Hang Seng rose by 0.44%. In South Korea though, the Kospi 200 was down by 0.12% even despite constructive signals on the geopolitical front. Meanwhile in Europe, futures tracking the major benchmarks are signaling a notably higher open for these indices today, with the only exception being the British FTSE 100.

COMMODITIES: In energy markets, oil prices traded higher on Tuesday, extending gains from the previous session. WTI crude is up by 0.2% and Brent by 0.3%, supported by the broader risk-on sentiment in financial markets. The main event for the oil market remains the OPEC meeting next week and whether – and to what extent – major producers will raise their supply. Judging from how previous OPEC gatherings have played out, prices are likely to start moving well ahead of the actual event on any comments from various energy ministers – most notably Saudi Arabia’s and Russia’s. In precious metals, gold prices are 0.2% lower today, currently trading near the $1,298 per ounce mark. The yellow metal is under pressure amid optimistic developments in the North Korean saga, but it should be noted that the magnitude of the decline is quite small, and gold continues to trade in the very narrow range it has established in recent weeks.

Major movers: Yen loses more ground amid Trump-Kim summit; sterling under fire

The dominant theme of the day was the meeting between Donald Trump and Kim Jong-un in Singapore. In a moment for the history books, the two met during the Asian trading session Tuesday and signed an agreement that reportedly says North Korea is committed to “work towards” complete denuclearization. The US also agreed to provide security guarantees to North Korea, while the two will “join efforts to build lasting and stable peace”.

The market response at the time of the agreement was relatively muted, perhaps due to most of the ‘good news’ already being priced in ahead of the meeting; recall markets were in a risk-on mood since yesterday. Safe-haven currencies like the Japanese yen and Swiss franc extended their losses today as the meeting was underway, declining by 0.3% and 0.25% respectively against the dollar. Gold is on the retreat as well, while US equity futures suggest a higher open today.

In the big picture, while this is without a doubt an encouraging development in the North Korea saga and is likely to reduce geopolitical premium on South Korean and other risk assets for a while, caution is still warranted until – and if – talk turns to action. Positive gestures, albeit of smaller magnitude, have occurred in the past as well but amounted to little in the end. Until more details are known, such as what kind of guarantees the US will provide, the North’s vow to “complete denuclearization” appears to be more of a symbolic gesture aimed at getting talks started, rather than an unwavering commitment.

Elsewhere, the British pound experienced another selloff yesterday following a significant disappointment in UK industrial production data for April. The poor data set likely cast doubt on the narrative that the UK economy’s lackluster performance in Q1 was only “transitory” and that the BoE may raise rates again as early as in August, something markets currently assign a 45% probability to.

Day ahead: UK jobs data, German ZEW survey and US inflation due; Brexit developments in the spotlight

Tuesday’s calendar features important releases out of the UK and the US, while in the case of the former Brexit developments will also be in focus. Meanwhile, as the US-North Korea summit comes to an end, investors will be turning their attention to the document signed by Trump and Kim.

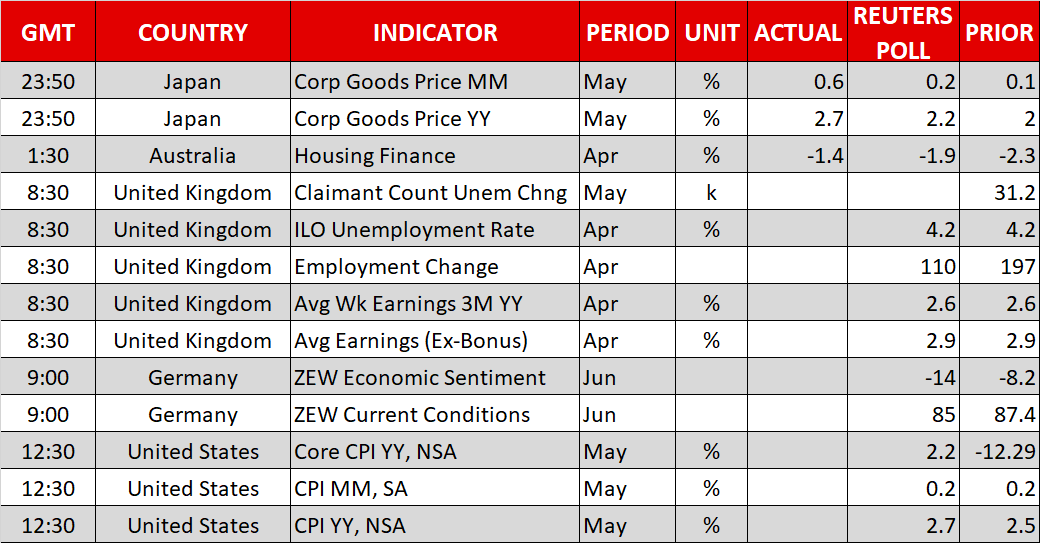

UK jobs data for April will be released at 0830 GMT. The unemployment rate is projected to remain at the multi-decade low of 4.2% for the third straight month, while employment is anticipated to rise by 110k in the three months to April, down from March’s robust figure of 197k, but still hold at relatively healthy levels. Most attention though, might fall on wage growth numbers, which despite being on the rise overall during the last few months, they still remain subdued given that the unemployment rate is standing at its lowest in 42 years. In this respect, the three-month average of weekly earnings is forecast to grow by 2.6% y/y, the same as in March. Excluding bonuses, average earnings are anticipated to grow by 2.9%, again the same pace as in March. Lastly, the number of unemployment claimants during May will be made public at 0830 GMT as well.

Besides data releases, Brexit developments are also likely to act as a driver for sterling pairs during today’s trading, as PM Theresa May will be facing a vote in Parliament that could effectively derail her plans for an exit from the EU and promote a softer Brexit instead. In relation to this, it is interesting that whenever a soft Brexit gains traction, sterling tends to gain. But that is also likely to be associated with a weaker May, and political uncertainty of this sort has in the past weighed on the British currency.

At 0900 GMT, June’s ZEW business surveys gauging economic sentiment and current conditions will hit the markets. Both are forecast to show further deterioration in business morale in June; specifically, the economic sentiment index is expected at its lowest since late 2012.

Out of the US, May’s inflation data as gauged by the consumer price index (CPI) are slated for release at 1230 GMT. Month-on-month, headline CPI is expected to grow at the same 0.2% pace as in April, while it is projected to accelerate to 2.7% on a yearly basis from 2.5% in April, matching a multi-year high from February last year. Core CPI that strips volatile items out of its calculations is also anticipated to grow at a faster pace year-on-year in May (2.2% vs 2.1%). The numbers do not pertain to the Fed’s preferred inflation gauge – that being the core PCE price index – but they’re still of importance; a beat could lead market participants to price in a more aggressive Fed tightening cycle, consequently supporting the dollar.

In the meantime, the Fed will today commence its two-day meeting on monetary policy at the end of which it is widely expected to deliver its second 25bps rate hike of the year.

In terms of the Trump-Kim meeting, both leaders expressed optimism, with the focus now shifting on follow-through actions to achieve what was outlined in the document signed by the two leaders – among others, a denuclearized Korean peninsula.

In energy markets, API weekly data on crude stocks are due at 2030 GMT, while OPEC’s monthly report discussing oil demand and supply is due at 1120 GMT.

The US Senate Banking Committee will be voting on the nominations of Richard Clarida for Federal Reserve vice chairman and Michelle Bowman for member of the Federal Reserve Board of Governors at 1400 GMT.

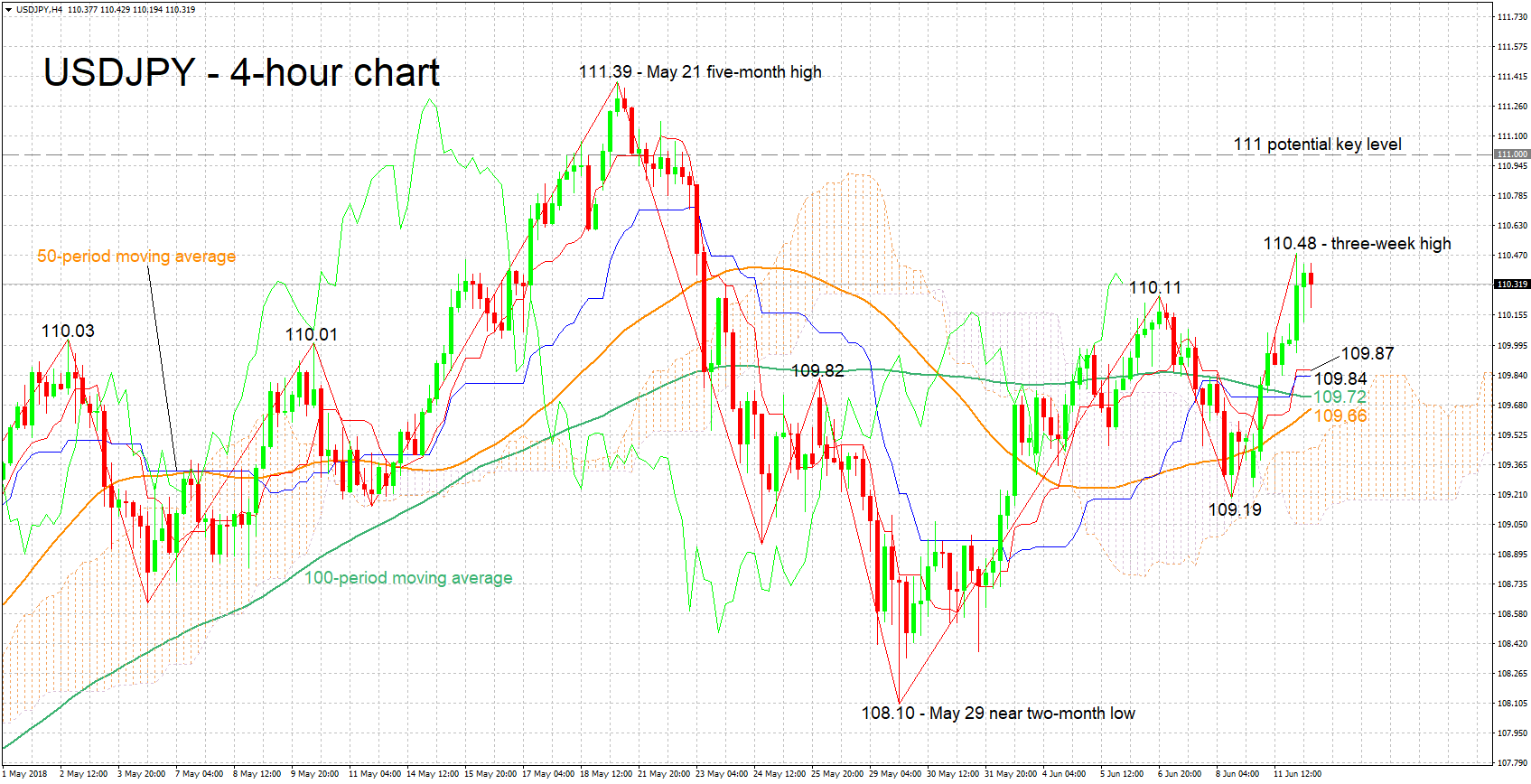

Technical Analysis: USDJPY hits 3-week high; positive momentum eases

USDJPY has gained more than 100 pips after last Friday’s 11-day low of 109.19, while earlier on Tuesday it touched a three-week high of 110.48. The Tenkan-sen has moved above the Kijun-sen in support of a bullish short-term picture, though the fact that the two have flatlined is an indication of easing momentum.

Stronger-than-expected US releases later on Tuesday are likely to boost the pair. Immediate resistance could come around the three-week high of 110.48 hit earlier in the day, while further above the 111 round figure would increasingly come into view.

On the downside and in case of poor data releases, support could come around 110.11, this being a previous peak with the area around it encapsulating the 110 handle, as well as a few other tops from the recent past. The Tenkan-sen (109.87), Kijun-sen (109.84), 100-period moving average line (109.72) and 50-period MA line (109.66) lie not far below and may provide support in case of steeper declines.

Further easing of geopolitical uncertainty (see Trump-Kim summit) is anticipated to push the pair higher and vice versa; the perceived safe-haven yen tends to gain in an environment of uncertainty and tensions.