{kind=link}

As Fed policymakers kick off their two-day policy meeting on Tuesday, the US will also release its inflation readings for May, at 1230 GMT. Forecasts point to a further acceleration in price pressures, something that could amplify speculation for a more hawkish set of rate-path projections by policymakers and thereby, enhance the dollar’s appeal ahead of the actual rate decision.

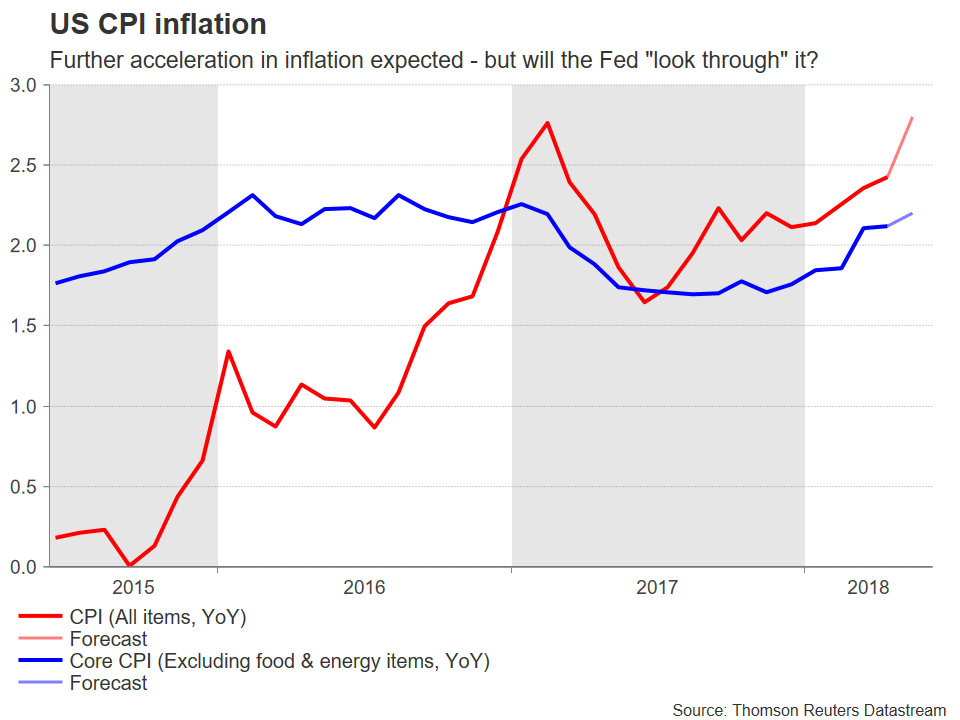

US inflation has been steadily picking up speed over past months, fueled by robust gains in the labor market, one-off effects that pulled inflation down last year filtering out of the yearly calculation now, and the latest surge in energy prices. Both the headline and core CPI inflation readings now stand above the Fed’s 2% goal, while the central bank’s preferred measure – the core PCE price index – rests just below, at 1.8%.

Forecasts suggest this trend is likely to continue in May. The headline CPI rate is projected to climb to 2.8% in yearly terms from 2.5% in April, something that would bring it to its highest point since 2012. The core figure, which excludes volatile food and energy items, is anticipated to reach 2.2% from 2.1% previously. Adding credence to these forecasts are the nation’s Markit manufacturing and services PMIs for May. The former showed that although selling price inflation eased slightly, it was still the second-fastest since June 2011, while the latter found prices charged by service firms rising at the quickest pace in three months.

Should the actual prints meet the forecasts, then the key question for dollar traders becomes whether a further speed-up in inflation will cause the Fed to adopt a more hawkish stance and hint at faster rate hikes moving forward. Recall that policymakers recently signaled they are comfortable allowing price pressures to overshoot 2% for a while, so it’s questionable whether even an upside surprise in inflation will nudge them towards further action. Especially so if such an upturn is fueled mostly by energy-related effects, which are considered transitory. Against this backdrop, a strong beat in the core rate is likely needed to amplify expectations for a more aggressive Fed.

Back in March, the individual rate projections of FOMC officials – the so-called “dots” – pointed to a total of three 25bps rate hikes being delivered this year. Crucially though, it was a very close call. If just one more member raises her/his “dot” to four hikes at the upcoming meeting, then the median “dot” would move higher to signal four hikes in total for 2018. It’s probably going to be a close call once again, and a strong set of inflation data would increase the odds of such a hawkish revision taking place, thereby enhancing the dollar’s allure ahead of the rate decision.

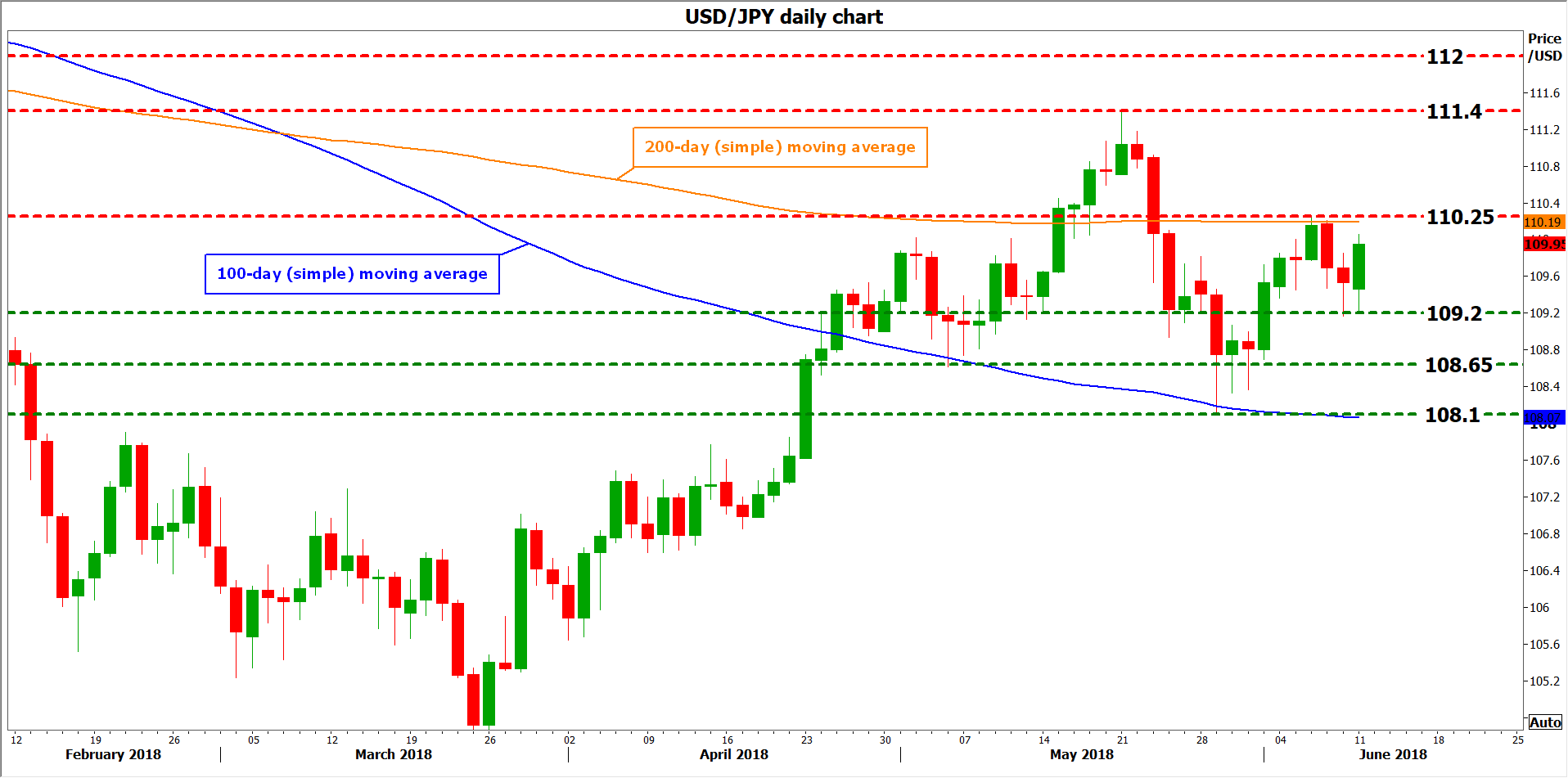

Technically, looking at dollar/yen, immediate resistance to advances could come at the 110.25 barrier, the high of June 6. The area around it also encapsulates the pair’s 200-day moving average, at 110.19. An upside break would shift attention to the 111.40 territory, which halted the pair’s climb on May 21. Even higher, the round figure of 112.00 would increasingly come into focus.

On the downside – and in case a disappointment in the CPI prints curbs speculation for a more aggressive Fed – then support may be found around 109.20, the low of June 8. Further below, declines may stall initially near the May 4 trough of 108.65, and subsequently at 108.10, the May 29 low – note that the 100-day day moving average lies just below, at 108.07.