{kind=link}

Yesterday’s trading session saw a rotation from the NASDAQ and Tech into the Dow Jones and Industrials. The European Indices have under preformed this week in part due to Euro strength and in part due to concern about trade/political stability in Italy and worsening economic data. China diverged from its Asian Equity counterparts this week and has led the Indices lower overnight. The G7 is meeting today and tomorrow with tensions between the US and the other participants at a high level over trade. Moves in FX are light today in anticipation of the meetings today which will dominate direction into next week and beyond.

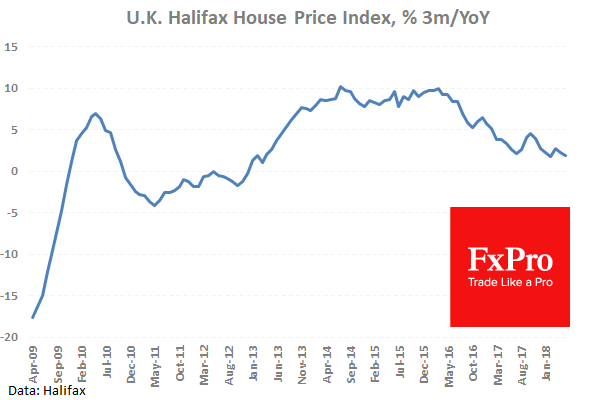

UK Halifax House Price Index (3m/YoY) (May) was 1.9% against an expected 1.9% from 2.2% previously. This data has been declining since hitting a high of 3.9% in June 2014 and is expected to rebound from a multi-year low last month. GBPUSD moved higher from 1.34533 to 1.34717 following this data release.

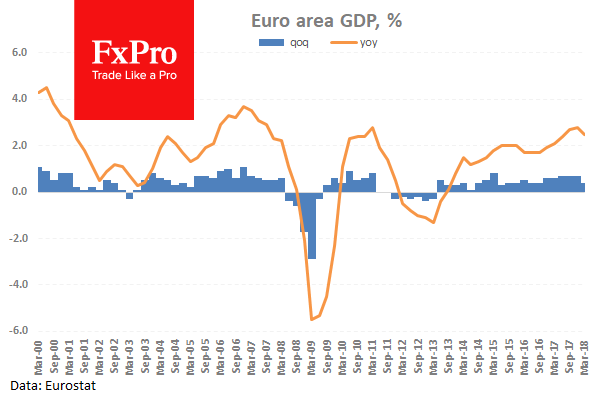

Eurozone Gross Domestic Product s.a. (Q1) was 0.4% QoQ and 2.5% YoY as previously reported. The QoQ number has been holding steady around 0.6% for 2017 but drop down to 0.4% showing a decline in growth across the Eurozone. The YoY number drop down to 2.5% after weakening Eurozone data. This data sent the EURGBP pair higher from 0.87781 to 0.88372 after this data release.

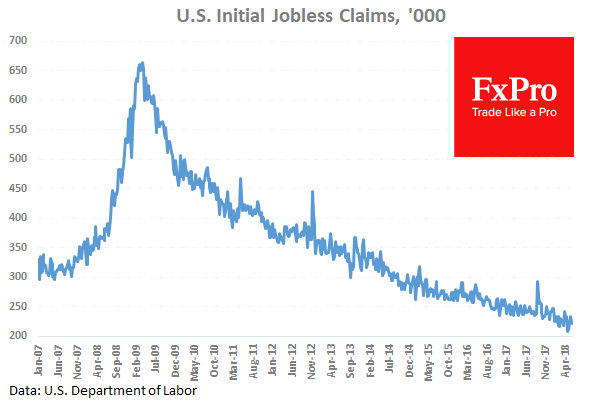

US Continuing Jobless Claims (May 25) were 1.741M against an expected 1.738M. Initial Jobless Claims (Jun 1) were 222K against an expected 225K. This data is showing an increase in the number of people who are jobless. USDJPY moved 110.000 to 109.642 in the time after this data release.

EURUSD is up 0.09% overnight, trading around 1.18091.

USDJPY is down -0.02% in the early session, trading at around 109.667

GBPUSD is up 0.03% this morning trading around 1.34256.

Gold is down -0.09% in early morning trading at around $1,295.96

WTI is down -0.26% this morning, trading around $65.75