{kind=link}

Chinese trade numbers for the month of May are scheduled for release on Friday, with the figures perhaps attracting more interest in light of trade discussions between the US and China. Also of importance out of the world’s second largest economy, will be producer and consumer price inflation data due on Saturday.

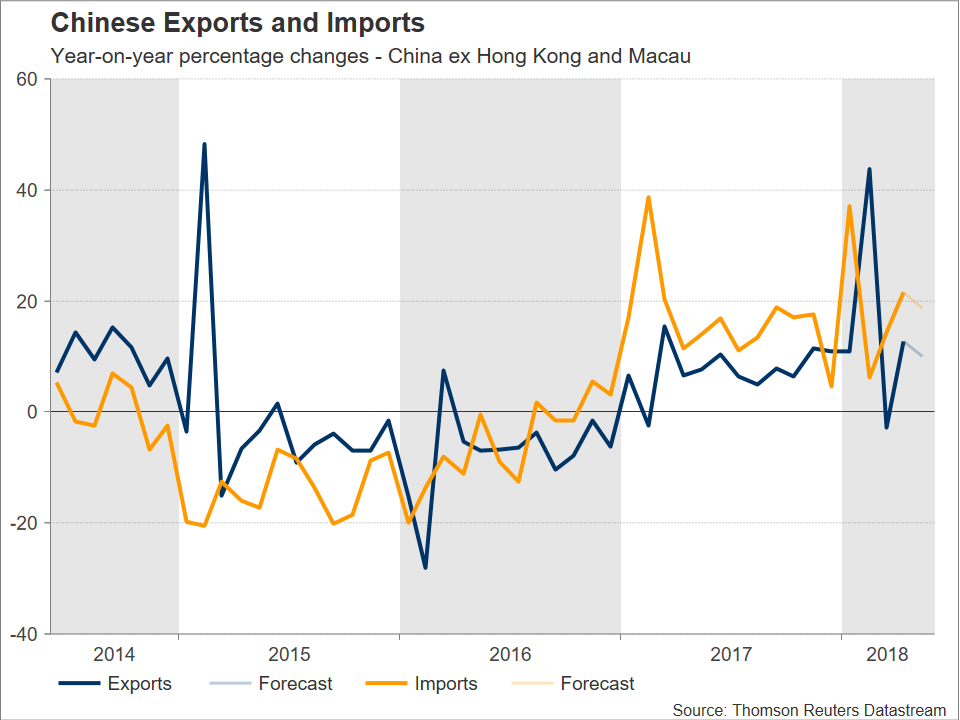

Friday’s figures are anticipated to show both exports and imports growing solidly on an annual basis, albeit at a slower pace relative to the previously recorded month. Specifically, exports and imports are projected to rise by 10.0% and 18.7% y/y respectively in May, down from April’s corresponding readings of 12.7% and 21.5%. Meanwhile, the trade surplus (measured in USD) is forecast to expand to $31.90 billion, up from April’s $28.38bn. It should be kept in mind that the figures lack a specific time of release.

Despite economic momentum appearing to ease in certain economies – such as the euro area –, still global growth is anticipated to record a relatively robust year in 2018 according to analysts. Chinese exports are expected to benefit in such an environment; China is the world’s largest exporter. Posing risks to the outlook for Chinese exports, however, is the prospect of protectionist policies by the Trump administration, including the levy of tariffs on goods imported by China. In this respect, talks between China and the US have failed to provide a constructive outcome so far, with risks to global trade remaining in the background.

Regarding the outlook for imports, strong consumer spending, in conjunction with last week’s announcement that China plans to cut tariffs on approximately 1.5k consumer products, are supportive of higher prints moving forward. A factor that might negatively affect imports are government efforts to limit debt availability on the back of worries of a potential credit crisis; this though is expected to benefit the Chinese economy in the longer term.

For the record, US data released on Wednesday showed China’s bilateral trade surplus with the US standing at $28.0bn in April, having risen by 8.1% relative to March. However, the country’s (US) overall trade deficit fell to a seven-month low of $46.2bn, as exports touched a record high.

In the currency markets, Australia’s close economic ties with China have rendered the aussie dollar a liquid proxy for China’s economy. In this respect, besides the yuan, the Australian currency will also be closely watched as the trade data go public; a strong Chinese economy is seen as aussie-positive.

However, it could be argued that developments relating to trade negotiations between Beijing and Washington can much more profoundly affect the aussie, rather than Friday’s release. The rationale behind the aforementioned is that such developments can affect Australia’s economic outlook; barriers to trade are expected to act to the detriment of global growth, with the hit on the Australian economy being amplified given that it heavily relies on commodity exports. That said, the recent exchange of “tough talk” between the US and China did not weigh much on the aussie, with market participants seemingly getting used to the rhetoric. Conclusive punitive actions between the world’s two largest economies though, are most likely to result to positioning in the markets.

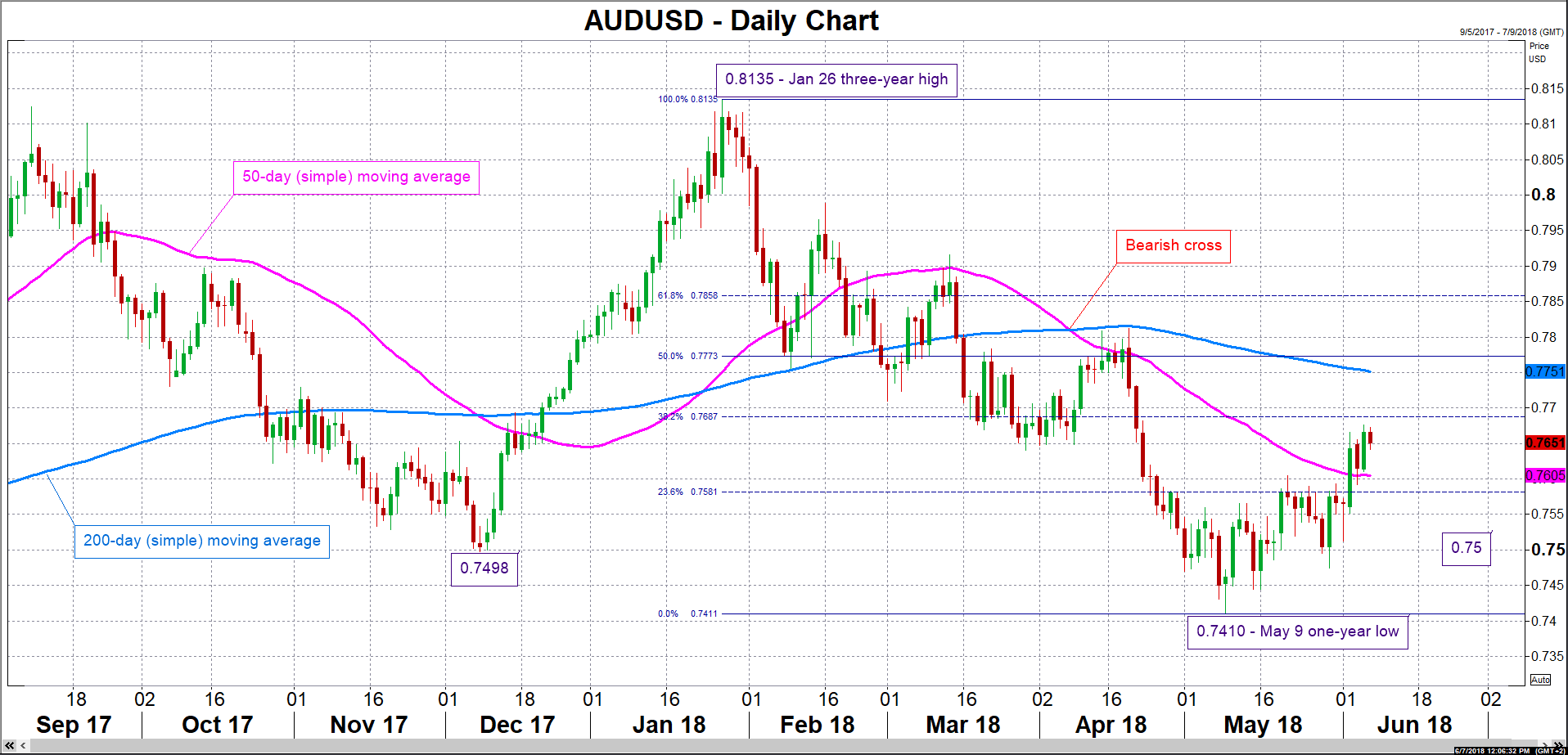

In terms of reaction in the FX markets and focusing on aussie/dollar, abating trade risks are likely to spur buying interest for the pair. Resistance to advances might come around the 38.2% Fibonacci retracement level of the January 26 to May 9 downleg at 0.7687. Notice that the area around this mark was relatively congested between mid-March and early-April, while it also includes the 0.77 round figure that may hold psychological significance. More bullish movement would turn the attention to the region around the 200-day moving average line at 0.7751. On the other hand, a fallout in US-China discussions that considerably raises the chances for a trade war is expected to exert selling pressure in AUDUSD. A first-line of support could take place around the 50-day MA at 0.7605, including the 0.76 handle. The 23.6% Fibonacci level lies not far below at 0.7581, while steeper losses would increasingly bring into focus the 0.75 handle, which may also hold psychological importance, for additional support.

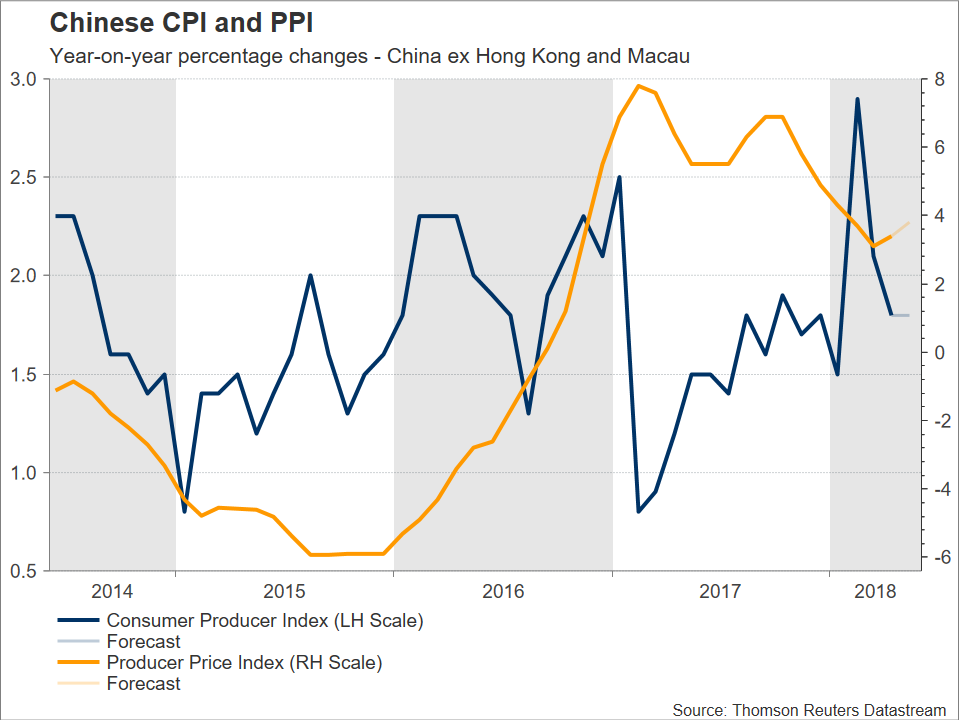

Other notable releases out of China during the current week are Saturday’s (0130 GMT) producer price index (PPI) and consumer price index (CPI), both for the month of May. Factory prices, as gauged by the PPI, are forecast to maintain positive momentum, expanding at a faster pace – 3.8% y/y – for the second straight month, after easing to 3.1% in March, the lowest reading since late 2016. This is encouraging news in an environment of increased efforts to curb pollution and limit lending by so-called “shadow” banking vehicles. In terms of CPI, it is anticipated to remain steady at 1.8% y/y in May.