{kind=link}

Here are the latest developments in global markets:

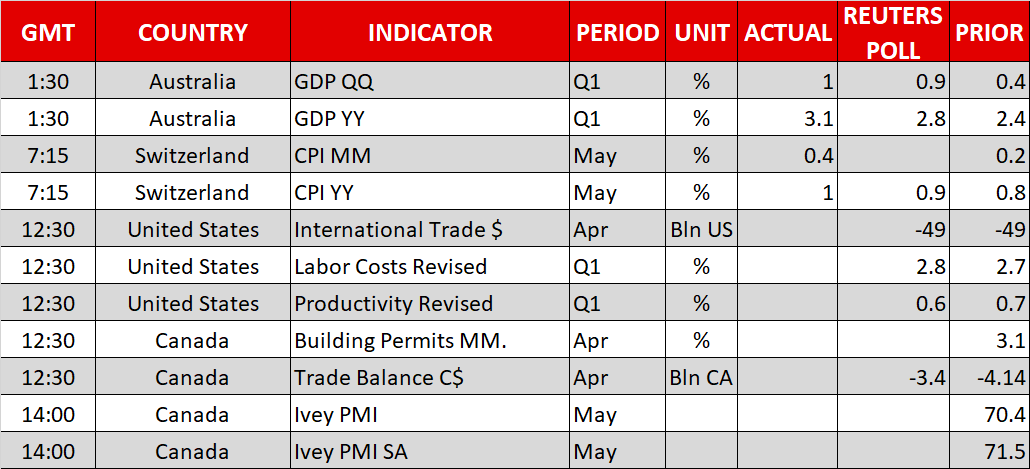

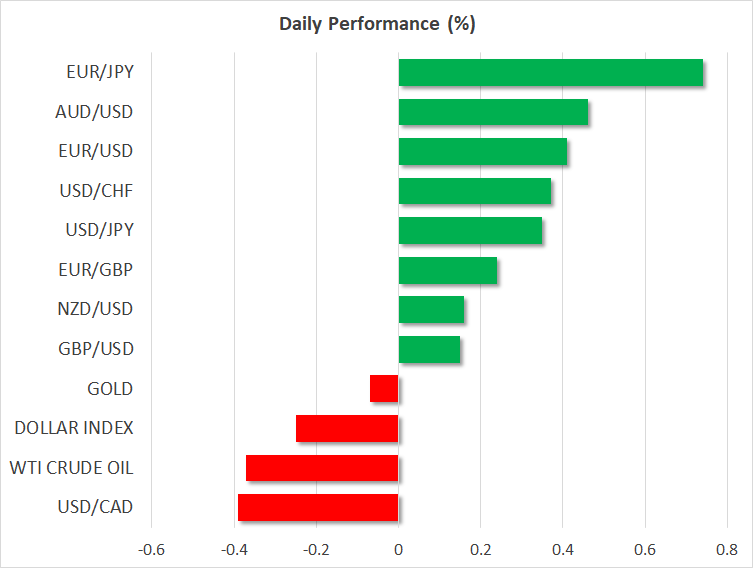

FOREX: The dollar unlocked a fresh two-week high of 110.16 (+0.34%) against the Japanese yen early in the European afternoon as another round of data released yesterday enhanced once again optimism on the US economy despite trade risks hanging in the background. The dollar index, though, which gauges the strength of the dollar versus six major currencies was down on the day at 93.65 (-0.27%) thanks to the rising euro and pound. Euro/dollar was in bullish mode for the third consecutive day, peaking at a fresh two-week high of 1.1773 today. Buying interest for the euro widened further after the head of Germany’s central bank, Jens Weidmann, and the ECB chief economist, Peter Praet send a message on Wednesday that end to the QE program could be possible by December, a decision probably taken at next week’s ECB policy meeting. The former also expressed confidence that inflation would return to the target. Meanwhile on the trade front, the European Commission announced that countermeasures against the US protectionism would come into effect in July. Pound/dollar was also enjoying gains today, trading at a two-week high of 1.3432 (+0.26%) as recent figures indicated that the economic slowdown in Q1 could be temporary. However, Brexit uncertainties were keeping investors cautious. Euro/pound changed hands higher as well at 0.8760 (+0.14%). In antipodean currencies, upbeat Q1 GDP growth readings in Australia kept aussie/dollar on the upside, with the pair last seen at 0.7649 (+0.49%). Kiwi/dollar was in the green too, trading at 0.7035 (+0.19%). Loonie/dollar declined further to 1.2920 (-0.39%) following after sources said yesterday that the US Treasury Secretary Mnuchin had asked Trump to exempt Canada from the recent metal tariffs. Moreover, other headlines stated that Canada is against of bilateral trade relations with the US, while is willing to continue negotiations on NAFTA.

STOCKS: European stocks were mostly in the green at 1100 GMT except the Italian FTSE MIB 100 which dipped by 0.16%, after the Italian new Prime Minister showed little willingness at his first speech in Parliament that he would scale back from the populist agenda. The pan-European STOXX 600 inched up by 0.09% with basic materials, energy, and technology sectors driving the index up, while the blue-chip Euro STOXX 50 was marginally down by 0.07%. The German DAX 30 rose 0.41%, extending gains since May 31, the French CAC 40 climbed by 0.06% and the Spanish IBEX 35 went up by 0.82%. UK’s FTSE 100 head up by 0.30%, while futures tracking US stock indices were pointing to a positive open.

COMMODITIES: Oil prices were weighing concerns on rising supply and hopes of lower exports in Venezuela, with WTI crude and Brent being down by 0.66% and 0.09% at $65.09/barrel and $75.32/barrel respectively. Particularly worries were based on news that OPEC could raise its output at its two-day policy meeting on June 23-24 in an attempt to slow down the recent rally in prices which was characterized as taken too far. Yesterday reports stating that the US is planning to ask OPEC for a 1 million output hike added further pressure to markets. However, today’s headlines announcing that Venezuela, a major energy supplier to the US and the biggest hub of reserves, considers halting its export production provided some support to the market. In precious metals, gold was moving sideways around $1,2950/ounce.

Day Ahead: US & Canadian trade data awaited

For the remainder of the day, the US will see the release of April’s trade balance at 1230 GMT which is forecasted to remain unchanged at -49.00bn. Also, the Unit Labor Costs index for Q1 is anticipated to inch up to 2.8% q/q from 2.7%.

At the same time, Canada will be publishing figures on trade balance as well, with forecasts being for trade deficit to narrow in April from 4.14bn to 3.40bn. Building permits and Ivey PMI out the country will be also available at 1230 GMT and 1500 GMT respectively, though trade stats will probably attract a greater attention amid rising trade uncertainties between the US and the rest of the world.

In energy markets, investors will look through the EIA report on US crude oil inventories. According to forecasts, crude stocks will drop by 1.824 million barrels in the week ending June 1 compared to a fall of 3.620 million in the preceding week. On the other hand, gasoline inventories and distillate stocks are anticipated to increase though not by much.

Investors are turning their attention to the Group of Seven meeting later this week that may give any clues on global trade tensions, as well as policy meetings from the European central bank and Federal Reserve next week month for any guidance for the next interest rates decisions.

In terms of public appearances, the ECB Members of the Supervisory Board Pentti Hakkarainen and Ignazio Angeloni will give speeches at 1330 GMT and 1710 GMT respectively. Meanwhile, Bank of England MPC member Ian McCafferty will be taking part in a Q&A session with listeners of LBC radio.