{kind=link}

Here are the latest developments in global markets:

FOREX: The dollar index, which gauges the greenback against six major currencies, was little changed on Tuesday. Meanwhile, the aussie recorded some losses after some RBA comments on the outlook for inflation which are supportive of lower rates for longer. Nevertheless, the currency managed to largely recover its earlier losses.

STOCKS: Major US indices finished in the green yesterday, with the Dow and the Nasdaq Composite adding 0.7% and the S&P 500 rising by 0.45%. The tech-heavy Nasdaq also finished at an all-time high, with tech behemoths Apple, Amazon and Microsoft all achieving the safe feat. During Tuesday’s Asian session, the Japanese Nikkei 225 added 0.15%, while the broader Topix index was roughly flat. Hong Kong’s Hang Seng was up by 0.45%. Futures tracking major European indices were trading lower, with the same holding true for contracts on major Wall Street indices; though those on US benchmarks were only slightly lower. Electric vehicle-maker Tesla will be attracting interest today as it will be holding its annual shareholders meeting.

COMMODITIES: WTI and Brent crude were up by 0.6% and 0.25% at $65.12 and $75.51 per barrel respectively. Despite the rise, the benchmarks remain in correction mode overall, having posted considerable losses in previous days, including yesterday. Worries on rising supply are seen as a reason behind the fall – it can be argued that some recent comments by an OPEC committee have supported such concerns. The API weekly report on US crude stocks due at 2030 GMT might offer some short-term direction to prices. Gold was higher, though by less than 0.1%, at $1.292.51 an ounce.

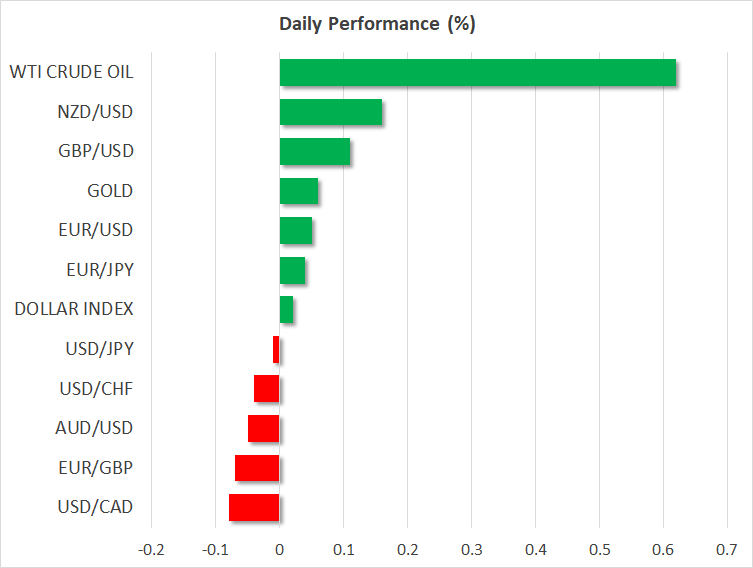

Major movers: Dollar posts 2-week high versus the yen with trade risks still a consideration; aussie hurt by RBA

The dollar’s index against a basket of currencies was not much changed at 0658 GMT. Dollar/yen was more or less flat, having earlier touched the 110 level to record a near two-week high. Market bets for a more aggressive Fed tightening cycle remaining elevated after Friday’s largely strong US jobs report was seen as a factor contributing to the rise in the pair in recent days. However, the greenback seems susceptible to “Trump risk”, with key US allies getting more alienated as a result of the US administration’s actions on the trade front. In this respect, a G7 meeting in Canada later in the week will be interesting to watch.

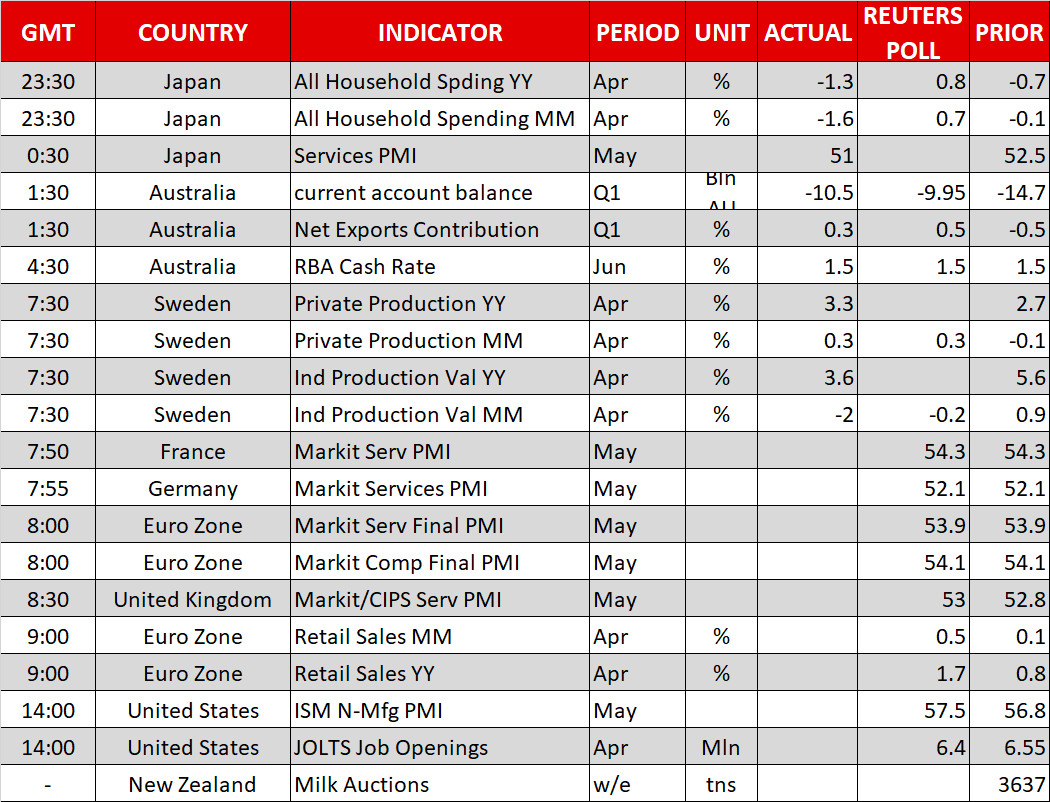

On the data front, Japan saw the release of household spending figures which surprised to the downside. Nevertheless, market reaction to the numbers was limited.

The euro was slightly higher versus the dollar, standing at a distance relative to last week’s 10-month low of 1.1506. Euro/dollar was up by less than 0.1% and marginally above the 1.17 handle. Fading political uncertainty in Spain and more importantly Italy acted as catalysts for the common currency’s recovery of some sorts in previous sessions; yesterday euro/dollar recorded a near two-week high of 1.7744, while the euro’s rebounnd versus the safe-haven perceived yen is also notable.

Sterling was 0.1% higher against the greenback at 1.3326 ahead of the PMI release for the all-important for the UK economy services sector. The prints for the manufacturing and construction sectors, which were made public in previous days, managed to positively surprise.

The aussie, a big gainer on Monday on the back of stronger-than-anticipated data releases, lost some ground today, though it later recovered on a significant part of its losses. Contributing to the decline were a wider than projected current account deficit in Q1, as well as the RBA saying inflation will likely remain subdued for some time; the Bank kept rates unchanged at the historic low of 1.5% yet again upon completion of its meeting. Aussie/dollar was down by 0.05% at 0.7640; still this was not far below yesterday’s six-week high 0.7666. Meanwhile, kiwi/dollar was up by 0.2% at 0.7042, relatively close to one-month high levels.

Day ahead: Eurozone retail sales, UK services PMI and US ISM non-manufacturing PMI in focus; trade risks remain in the background

PMI readings and retail sales data will dominate the economic calendar on Tuesday, though attention will remain on the trade front, as investors fear that tit-for-tat retaliatory actions might take place. Brexit uncertainties are also back in the surface.

At 0800 GMT, the Eurozone will see the release of final Markit Services and Composite PMI figures for the month of May and forecasts are for the measures to stand at 53.9 and 54.1 respectively, as they were initially estimated. While the marks are the lowest since early 2017, they are above the threshold of 50 which separates growth from contraction. However, the impact on the euro might be moderate since preliminary data tend to be more market-sensitive. Therefore, the focus for the currency will turn to eurozone’s retail sales due at 0900 GMT. In this case, analysts forecast an annual expansion of 1.7% in April, compared to a growth of 0.8% in the previous month, while month-on-month projections are for a rise of 0.5% compared to 0.1% seen in the previously recorded month. As political conditions in Italy have somewhat stabilized, with the focus turning back to the calendar, an upward surprise in the data could support the common currency.

In the UK, the Markit/CIPS Services PMI is expected to inch up to 53.0 in May from 52.8 in the previous month. Note that there are no initial estimates for the gauge; this is the first and only release. Yet, any news around Brexit are likely to have a greater impact on the pound as investors wait for the exit bill to return to the House of Commons on June 12 according to the Times newspaper on Monday. After a defeat in the House of Lords, House lawmakers are said to hold votes on the bill and propose changes in key areas, such as the customs union and the Irish border.

Meanwhile in the US, the Institute for Supply Management (ISM) is scheduled to deliver its non-manufacturing PMI print at 1400 GMT and analysts believe that the gauge has gained 0.7 points in May, rising to 57.5. At the same time, the Bureau of Labor Statistics will be issuing its JOLTS job openings report, with the number of positions expected to have eased to 6.4 million in April from a record high of 6.55m in March.

Elsewhere, the Global Dairy trade auction will take place today at a tentative time, with the results expected to move the kiwi, as dairy products hold the largest share of exports in New Zealand.

Trade developments will continue to be under the spotlight ahead of a G7 meeting in Quebec on Friday, where the EU and Canada are expected to express their anger on the Trump administration’s decision to impose import tariffs on steel and aluminum coming from their respective countries. In the meantime, US trade tensions with China have also intensified after talks in Beijing did not lead to a breakthrough. Instead, China, in response to the recent tariff warnings by the US, said that the agreements reached in the latest negotiations in Washington will not take effect if the US pushes ahead with tariffs.

In oil markets, investors will be paying attention to the API weekly report on US crude oil inventories at 2030 GMT.

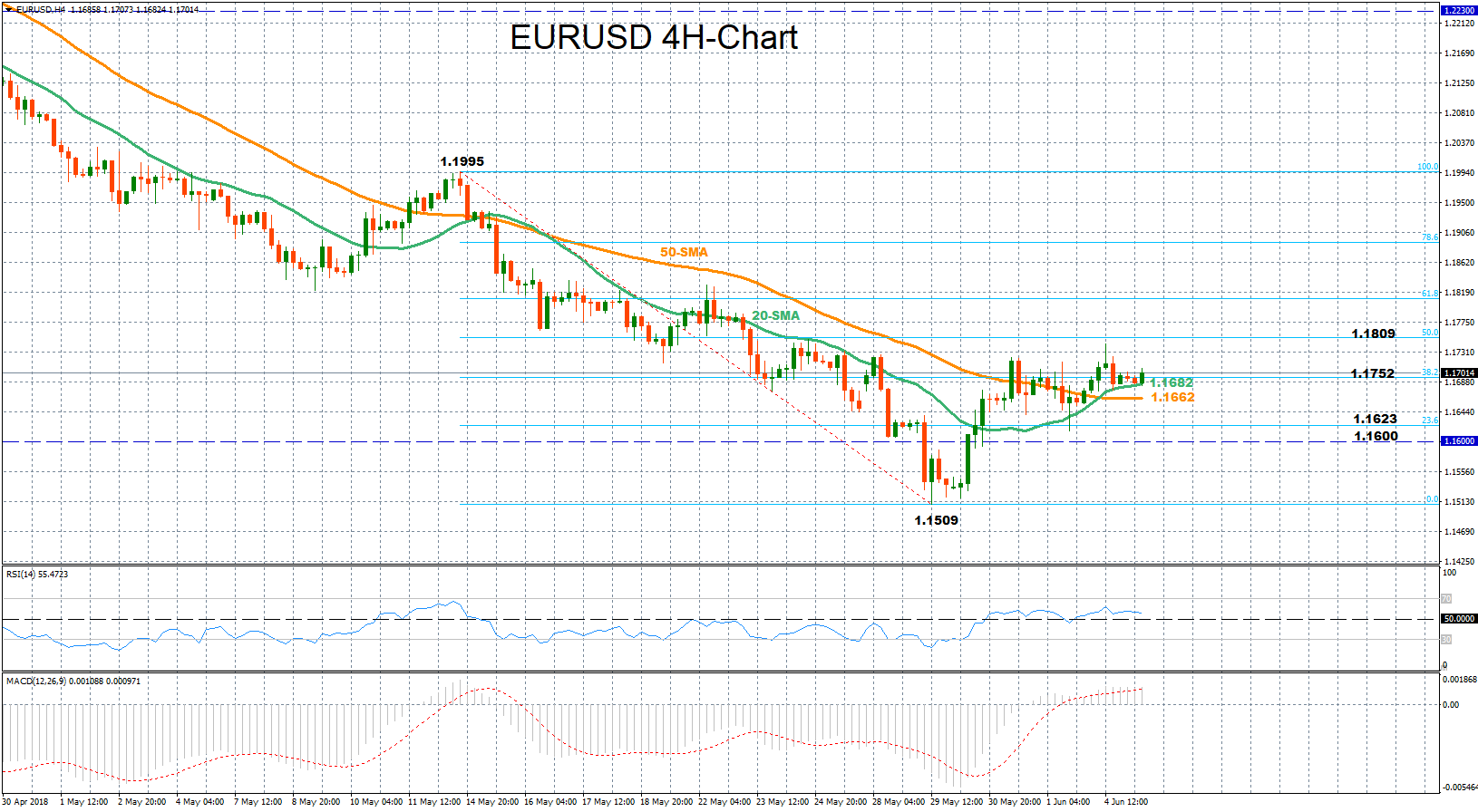

Technical Analysis: EURUSD looking mostly neutral in short-term

EURUSD is moving sideways after its rebound off 10-month lows on May 29. The RSI is also largely moving sideways in the four-hour chart in support of a neutral picture in the short-term. The MACD has also slowed down and is now on track to meet its red signal line. Trend signals, though, remain positive as the pair continues to hold above its moving averages.

If today’s data releases out of the eurozone beat expectations, the pair could benefit, probably bouncing up towards yesterday’s near two-week high of 1.1744 which is marginally below the 50% Fibonacci of 1.1752 of the downleg from 1.1995 to 1.1509. A break above from here could then spur further buying interest, driving the price up to the 61.8% Fibonacci of 1.1809.

Conversely, disappointing prints could pressure the market down to the 50-period (simple) moving average currently at 1.1662 (immediate support seems to be taking place at the 20-period SMA at 1.1682), while steeper declines could also reach the 23.6% Fibonacci of 1.1623 before the focus turns to the 1.1600 round level.

It should be kept in mind that US releases can also move the pair.