Australia PMI Manufacturing fell from 50.2 to 49.8 in January, a 32-month low. PMI Services rose from 47.3 to 48.3. PMI Composite rose from 47.5 to 48.2.

Warren Hogan, Chief Economic Advisor at Judo Bank said:

“Following eight consecutive rate hikes in 2022, the RBA Board will be meeting for the first time on 7 February. The latest PMI readings may raise the concern that the economy is not slowing sufficiently to bring inflation back to target in a timely manner…

“Inflation pressures may abate somewhat but the risk for the RBA is that inflation remains stubbornly high well into 2023. This could maintain upward pressure on inflation expectations and wages growth. On this basis it seems premature for the RBA to pause the current tightening cycle….

“We expect the RBA to hike the cash rate by 25bp in each of February and March before an extended pause. Further rate hikes may be required later in 2023 if the economy and inflation prove more resilient than current consensus forecasts suggest.”

Fed Chair Jerome Powell said at a conference today, “We’ve come a long way in policy tightening and the stance of policy is restrictive.”

Also, “We face uncertainty about the lagged effects of our tightening so far and about the extent of credit tightening from recent banking stresses.”

The Fed Chair suggested that the central bank now has room to scrutinize the economic data and evolving outlook more closely, and make measured assessments. “Having come this far, we can afford to look at the data and the evolving outlook to make careful assessments,” he added.

Interestingly, Powell emphasized the influence of the banking sector on the current financial landscape. He said, “While the financial stability tools helped to calm conditions in the banking sector, developments there on the other hand are contributing to tighter credit conditions and are likely to weigh on economic growth, hiring and inflation.”

“As a result, our policy rate may not need to rise as much as it would have otherwise to achieve our goals. Of course, the extent of that is highly uncertain,” Powell concluded.

In a speech delivered at the European Parliament overnight, ECB President Christine Lagarde emphasized the significant role of wage pressures. According to Lagarde, wage pressures “remain strong” across the region, anticipated to be an “increasingly important driver of inflation dynamics” in the coming quarters.

This shift towards wage-driven inflation comes as the contribution of profits, previously a significant factor in domestic cost pressures, begins to wane. Importantly, Lagarde pointed out that labor cost increases are being “partly buffered by profits”, preventing a full pass-through to consumer prices.

Lagarde also touched on the risks associated with second-round effects, a concern for economies dealing with inflation. She reassured that ECB’s current restrictive monetary policy, combined with a notable decline in headline inflation and well-anchored longer-term inflation expectations, serves as a “safeguard against a sustained wage-price spiral”.

Looking ahead, Lagarde expects continued deceleration in inflation rates as the effects of previous shocks diminish and tighter financing conditions exert downward pressure.

US 10-year yield dropped sharply overnight, by -0.061 to close at 1.370, hitting the lowest level since February. Some analysts noted that the move reflected believes that inflation in the US, and even the strong growth, were transitory only. The move also came in tandem with notable pull back in major stock indexes. Focuses will now turn to FOMC minutes for more guidance.

The speed of the fall in TNX was a surprise, even though the direction isn’t. Prior rejection by 55 day EMA already hinted that corrective pattern from 1.765 would more likely extend lower than not. For the moment, we’d expect strong support 38.2% retracement of 0.504 to 1.765 at 1.283 to contain downside and bring rebound. In other words, there is room for further decline in the near term, but downside is relatively limited.

Fed Vice Chair Richard Clarida gave a speech at a symposium in France today. There he noted that the US economy’s integration with the rest of the word has risk substantially over the past 60 years. That heightened US exposures to external shocks through channels of direct trade links, foreign exchange markets and contagion in financial markets.

Clarida added recently, US and other financial markets are “attuned to a number of prominent downside global risks”, including Brexit, a sharp slowdown in growth and trade tensions. He noted that Fed policymakers can “hardly ignore these risks”. Indeed, he pointed out three of the most recent FOMC statements have highlighted concerns about global economic and financial developments.

He also reiterated Fed’s stance that “in the presence of these risks and with inflation pressures muted, we can afford to be patient and data dependent as we assess in future meetings what adjustments in our policy rate might be necessary to sustain growth, employment, and price stability in the U.S. economy.”

Nikkei rose 2.21%, or 609.31 pts, to close at 29388.50 today, highest level in 30 years. The up trend from 16358.19 has just resumed. The index was contained well above rising 55 day EMA in the prior pull back, suggesting that some upside acceleration could be seen. Focus will be on whether daily MACD could break through the trend line resistance in next move, as well as the reaction to medium term channel resistance.

But in any case, outlook will stay bullish for now as long as 27619.80 support holds. 30k psychological level is the next target. But real obstacle is 100% projection of 6994.89 to 24129.34 from 16358.19.

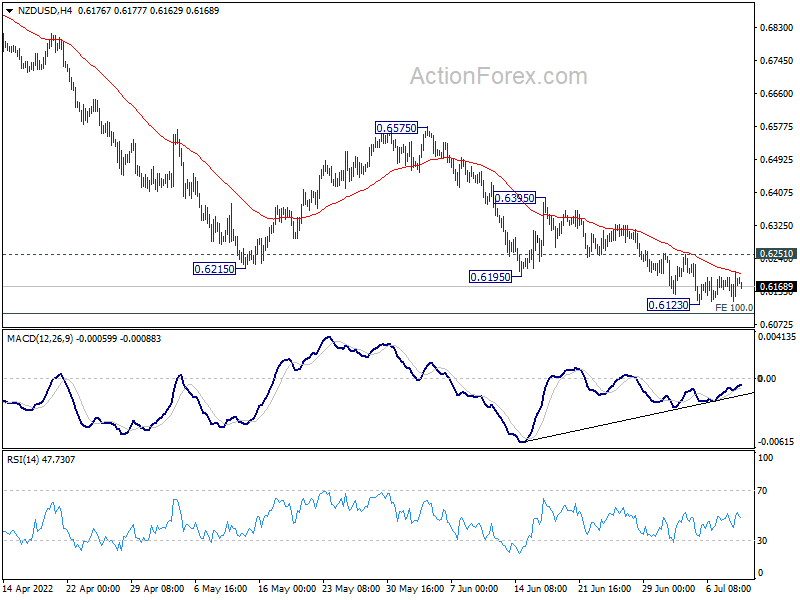

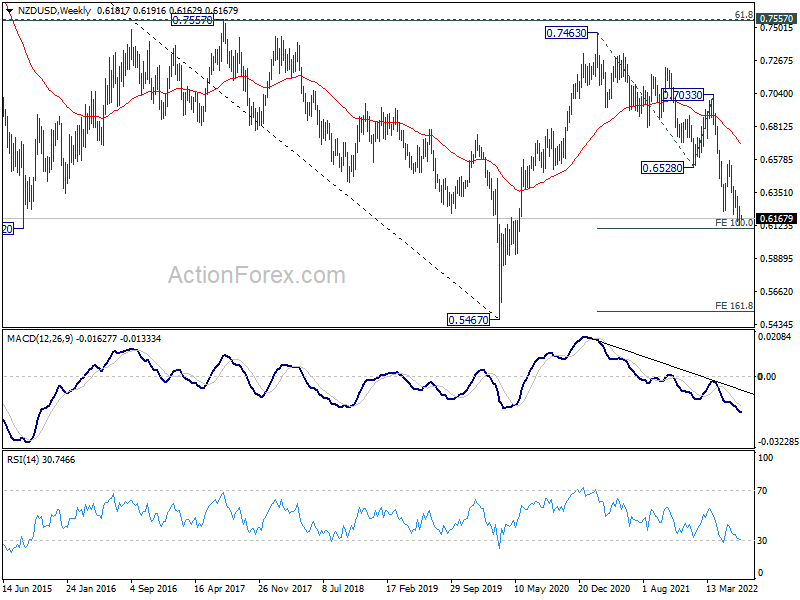

NZD/USD is staying in tight range above 0.6123 temporary low, looking forward to RBNZ rate hike later in the week. There is prospect of a rebound from medium term projection level at 0.6098 (100% projection of 0.7463 to 0.6528 from 0.7033). But break of 0.6251 minor resistance is needed to be the first sign of bottoming, while firm break of 0.6395 resistance is needed to confirm. However, sustained break of 0.6098 would risk more downside acceleration to 161.% projection at 0.5520, which is close to 0.5467 (2020 low).

Fed Vice Chair Lael Brainard said in a speech, “monetary policy will be restrictive for some time to ensure that inflation moves back to target over time.”

“It will take time for the cumulative effect of tighter monetary policy to work through the economy broadly and to bring inflation down.”

“In light of elevated global economic and financial uncertainty, moving forward deliberately and in a data-dependent manner will enable us to learn how economic activity, employment, and inflation are adjusting to cumulative tightening in order to inform our assessments of the path of the policy rate.” She said.

In March, UK CPI was unchanged at 1.9% yoy, below expectation of 2.0% yoy. Core CPI was also unchanged at 1.8% yoy, below expectation of 1.9% yoy. RPI slowed to 2.4% yoy, down from 2.5% yoy and miss expectation of 2.6% yoy.

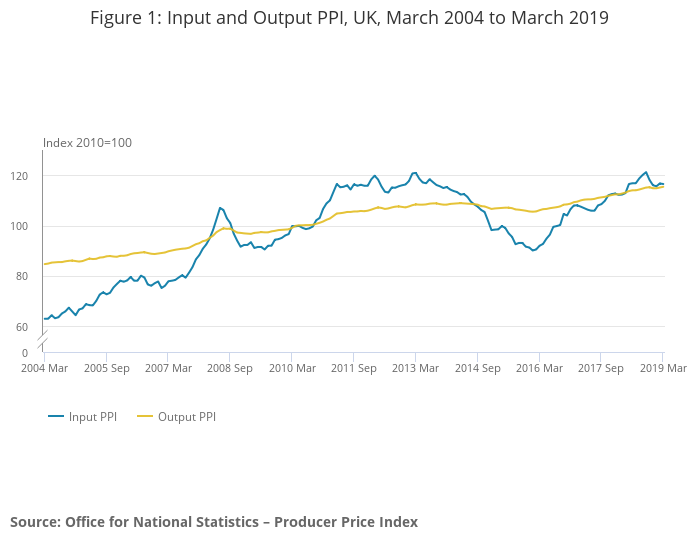

PPI input dropped -0.2% mom, rose 3.7% yoy, below expectation of 0.3% mom, 3.9% yoy. PPI output rose 0.3% mom, 2.4% yoy, versus expectation of 0.2% mom, 2.1% yoy. PPI output core rose 0.02% mom, 2.2% yoy versus expectation o f0.1% mom, 2.2% yoy..

House price index rose 0.6% yoy in February, well below expectation of 1.3% yoy.

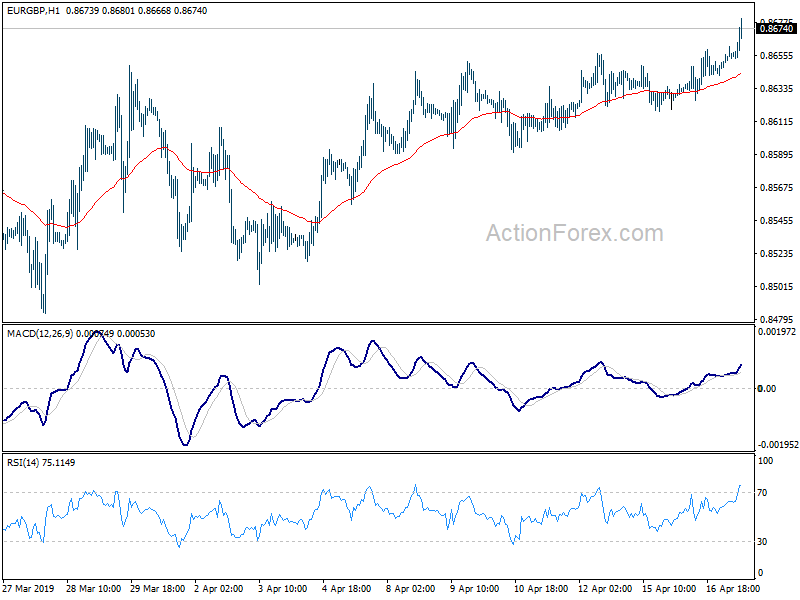

EUR/GBP rises mildly today mainly due to Euro’s strength. Sterling’s reaction to the data set elsewhere is muted.

Japan PMI Manufacturing was finalized at 49.4 in July, revised down from 49.6, just fractionally above June’s 49.3.

Joe Hayes, Economist at IHS Markit, said:

“Latest manufacturing PMI data did little to suggest that the worst has passed for the global goods-producing sector. Japanese manufacturers cut output for the seventh consecutive month amid soft demand from domestic and overseas clients.

“While slowing global growth in key export markets such as China and spillover effects from global trade spats remain a principal concern to companies, the risk now of Japan-South Korea relations deteriorating further merely adds to the already-strong headwinds.

“Forward-looking survey indicators suggest that manufacturers in Japan are set for another difficult quarter, as firms scaled down stocks and input purchasing to keep a lid on costs.

“Furthermore, more signs that the manufacturing downturn has now become deeply rooted was apparent in prices data, as output charges were reduced at the fastest pace in nearly three years amid increasing efforts to stimulate sluggish demand.”

ECB Governing Council member, Lithuania’s central bank governor Vitas Vasiliauskas said today that the foreward guidance suggested rate hike could come around autumn of 2019.

He noted, “we said ‘through the summer’, but as traditionally there is no meeting in August, it is obvious that we could talk about September-October.”

In the post meeting press conference, BoE Governor Andrew Bailey said, “overall a faster pace of policy tightening at this meeting will help to bring inflation back to the 2% target sustainably in the medium term,” he said.

“Looking ahead, that does not mean we’re now moving to a predetermined path of raising bank rate by 50 basis points per meeting, or indeed any other number for that matter.”

“Policy is not on a preset path. And what we do this time does not tell you what we’re going to do next time. All options are on the table for our September meeting, and beyond that.”

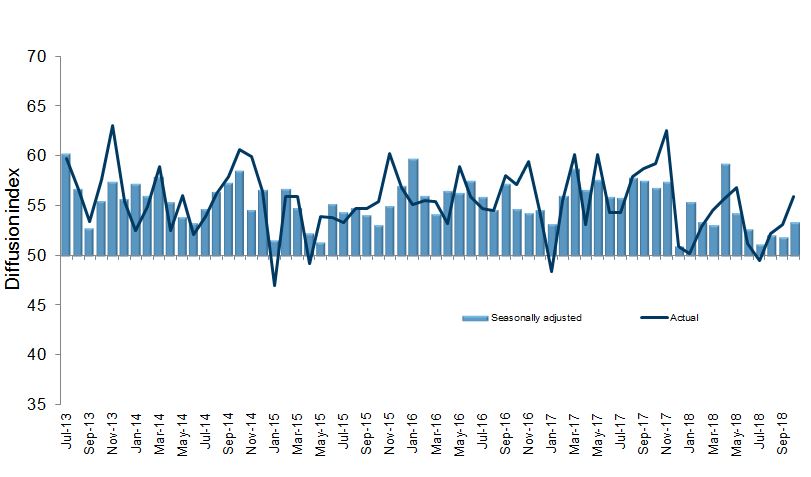

New Zealand BusinessNZ Performance of Manufacturing Index rose 1.6 to 53.3 in October, indicating faster expansion rate. That’s also the highest level since May. BusinessNZ noted “the October result was a welcome change from where the survey has sat for the previous four months.” And, while “the improvement in the PMI is not large, but we see it as important to the broader economic narrative”.

Looking at the details, the key sub-indicators of production (52.8) and new orders (56.7) both improved with their highest results since May and April respectively. Also, after dipping into contraction during various times in 2018, employment (52.4) improved for a second consecutive month. The proportion of positive comments (58.3%) also increased, with demand for products from offshore customers noted throughout.

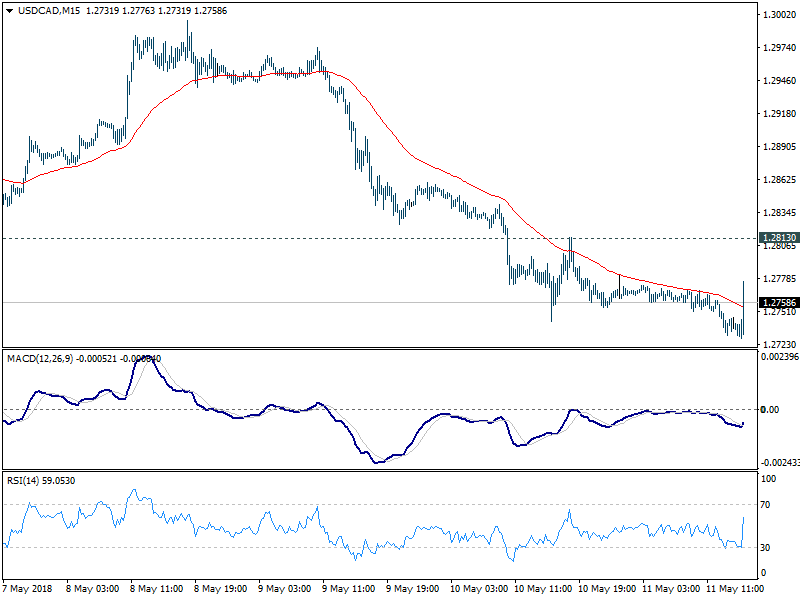

Canadian employment market contracted -1.1k in April, much worse than expectation of 20.5k. Unemployment rate was unchanged at 5.8%, in line with consensus.

From US, import price index rose 0.3% mom in April, below expectation of 0.50%.

USD/CAD recovers in reaction to the release, but there is no follow through buying yet. It has to overcome a minor support at 1.2813 before forming a temporary bottom. For now, further decline is still expected in the pair before the weekly close.

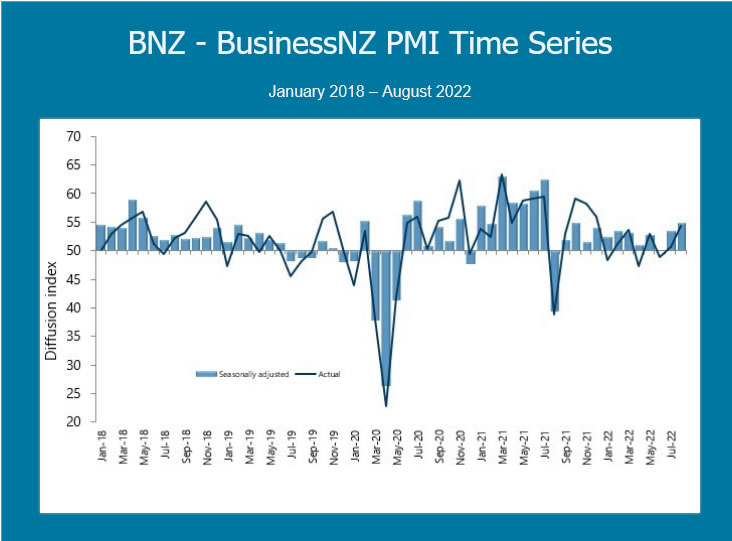

New Zealand BusinessNZ Performance of Manufacturing Index rose slightly from 53.5 to 54.9 in August. Production rose from 50.8 to 54.6. Employment rose from 52.9 to 53.6. New orders rose from 50.8 to 59.2. Finished stocks rose from 48.7 to 50.8. Deliveries rose from 50.1 to 53.7.

BNZ Senior Economist, Craig Ebert stated ” that manufacturing production, in general, was holding its own in Q2, rather than drooping, was portrayed in the PMI readings for April May and June. And in July and August the PMI has moved on to suggest an improving tone around underlying growth.”

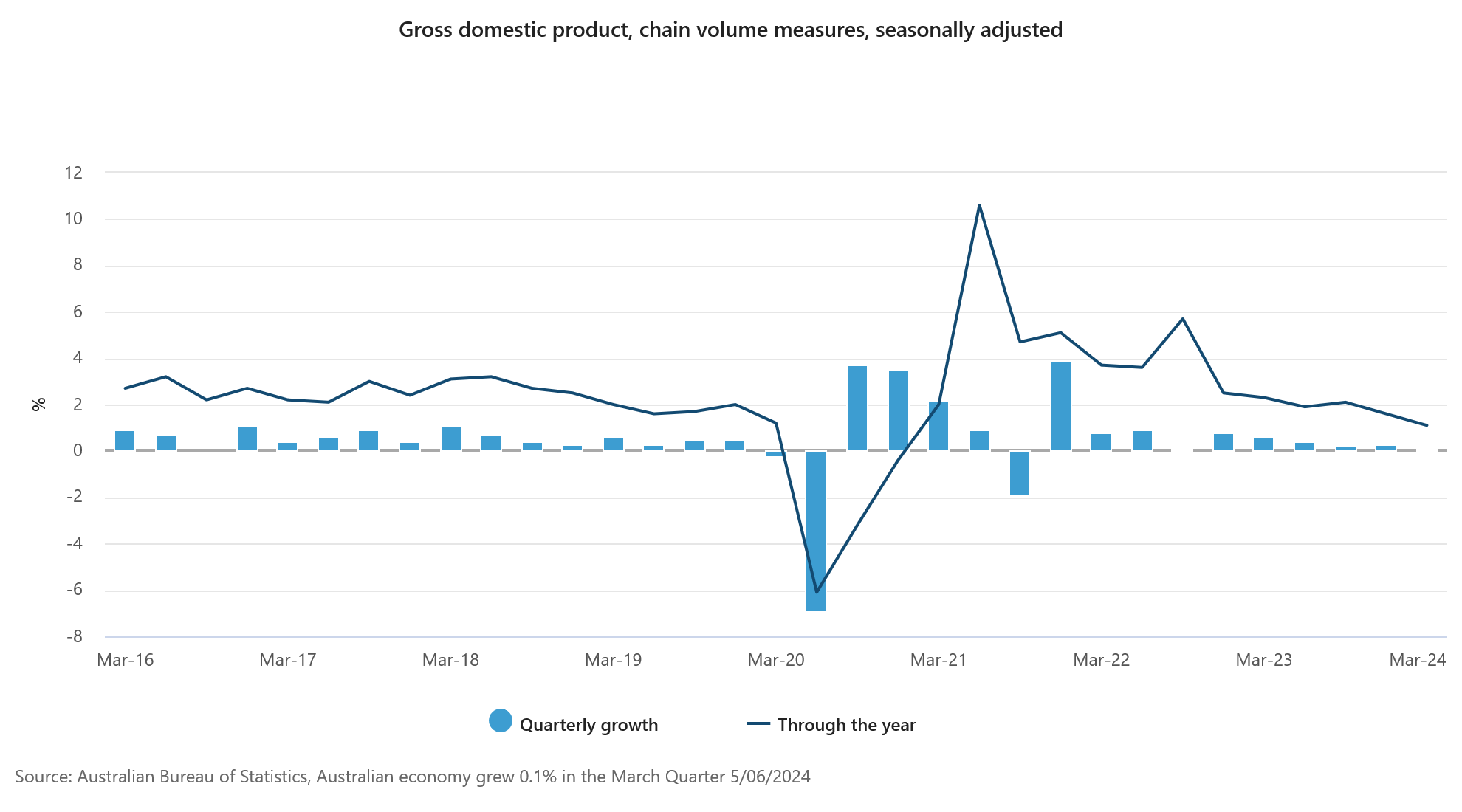

Australia’s GDP grew by 0.1% qoq in Q1, below the anticipated 0.2% growth. On a year-over-year basis, GDP increased by 1.1%.

Katherine Keenan, head of national accounts at ABS, remarked that GDP growth was weak in March, marking the lowest annual growth rate since December 2020. She also highlighted that GDP per capita fell for the fifth consecutive quarter, declining by -0.4% in March and -1.3% over the past year.

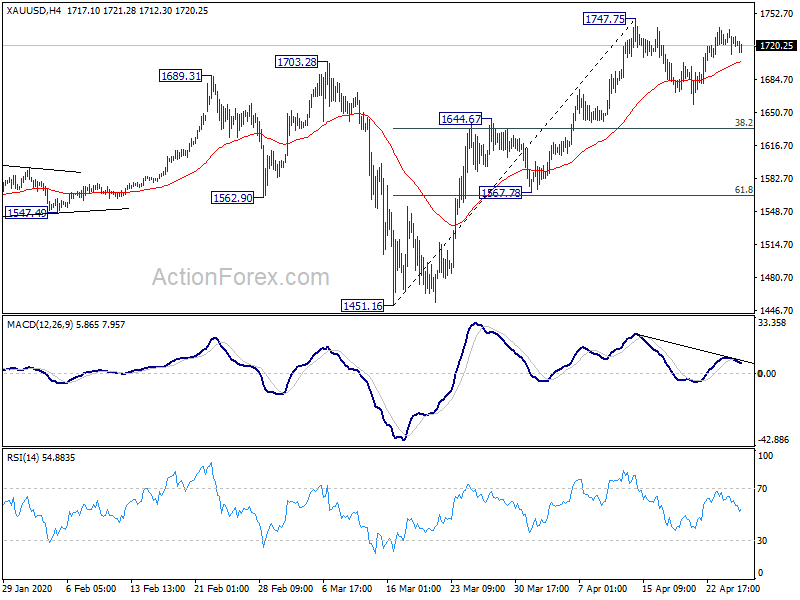

While Dollar is under broad based pressure today, Gold hasn’t been performing very well neither. There’s strong resistance from 1747.75 short term top to limit upside for the moment, as gold retreated. Short term focus is on 4 hour 55 EMA.

Break there would extend the consolidation from 1747.75 with another fall towards 1644.67 resistance turned support. But in that case, we’d expect strong support from 38.2% retracement of 1451.16 to 1747.75 at 1634.45 to contain downside and bring rebound.

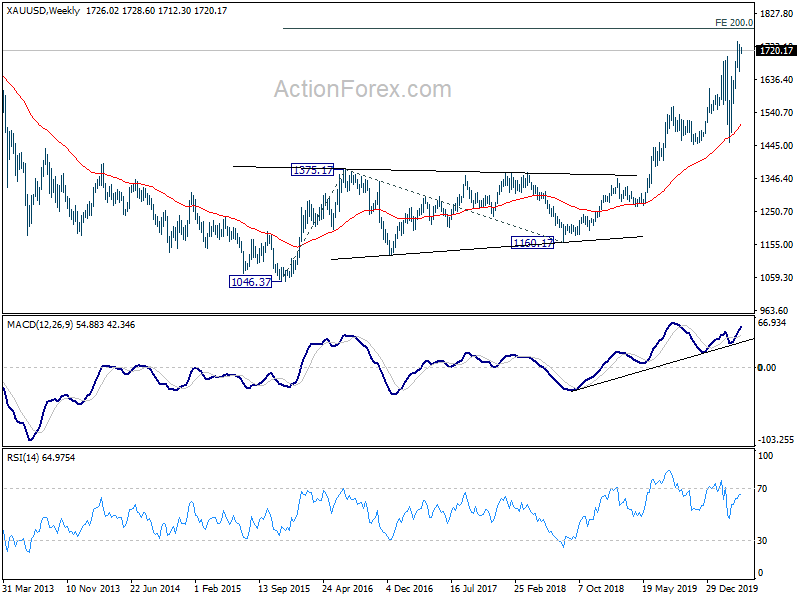

Meanwhile, break of 1747.75 will extend larger up trend to 200% projection of 1046.37 to 1375.17 from 1160.17 at 1817.77 next.

In the minutes from Fed’s September 19-20 meeting, while “a majority of participants” believed another rate increase might be in order, a contrasting view was held by “some” who deemed no further hikes necessary.

A unanimous consensus was evident among all attendees that the existing policy stance needs to “remain restrictive for some time”. The chief rationale behind this unified sentiment is to ensure that inflation trends downwards in a sustained manner to Fed’s target.

An interesting shift in communication strategy was proposed by “several participants”. They emphasized that discussions and subsequent messaging should transition from deliberating the potential height of rate hikes to determining the duration for which rates should be maintained at these elevated, restrictive levels.

In terms of gauging risks, participants “generally judged” that challenges to fulfilling the Fed’s mandates had become “more two sided”. However, a lingering concern persists. Despite this balanced view of risks, “most participants” continued to see upside risks to inflation.

Euro’s selloff accelerates further as German 10 year bund yield breaks 0.4 handle, reaching as low as 0.389 so far.

Chart snapshot from MarketWatch

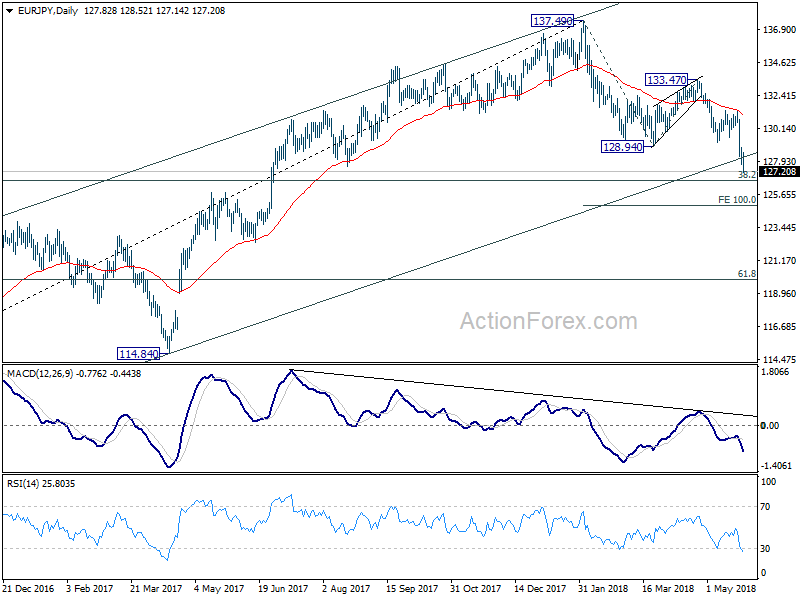

EUR/JPY reaches as low as 127.14 and moves further away from medium term channel support. Based on current momentum, there now a realistic threat of breaking 38.2% retracement of 109.03 to 137.49 at 126.61. That would carry rather bearish medium term implication. We’ll see how it goes.

New Zealand Dollar stays firm after RBNZ left OCR unchanged at 1.75% as widely expected. In the accompanying statement, RBNZ maintained the intention to keep OCR unchanged “through 2019 and into 2020”.

The language that the “the direction of our next OCR move could be up or down” was removed. Instead, RBNZ said “there are both upside and downside risks to our growth and inflation projections. As always, the timing and direction of any future OCR move remains data dependent.”. That at first glance looked like the central bank is moving away from the possibility of a cut. However, Governor Adrian Orr made it clear in the press conference that “it would be pointless to remove that option”, regarding a cut.

Orr also talked down the pick-up in GDP growth in the June quarter as “partly due to temporary factors”. Instead, he pointed to businesses surveys which “suggest growth will be soft in the near term”. While employment is “around its “maximum sustainable level”, core inflation remains below 2% target mid-point, “necessitating continued supportive monetary policy”.

Below are the press conference video and full statement.

By loading the video, you agree to YouTube’s privacy policy. Learn more

The Official Cash Rate (OCR) remains at 1.75 percent. We expect to keep the OCR at this level through 2019 and into 2020.

There are both upside and downside risks to our growth and inflation projections. As always, the timing and direction of any future OCR move remains data dependent.

The pick-up in GDP growth in the June quarter was partly due to temporary factors, and business surveys continue to suggest growth will be soft in the near term. Employment is around its maximum sustainable level. However, core consumer price inflation remains below our 2 percent target mid-point, necessitating continued supportive monetary policy.

GDP growth is expected to pick up over 2019. Monetary stimulus and population growth underpin household spending and business investment. Government spending on infrastructure and housing also supports domestic demand. The level of the New Zealand dollar exchange rate will support export earnings.

As capacity pressures build, core consumer price inflation is expected to rise to around the mid-point of our target range at 2 percent.

Downside risks to the growth outlook remain. Weak business sentiment could weigh on growth for longer. Trade tensions remain in some major economies, raising the risk that trade barriers increase and undermine global growth.

Upside risks to the inflation outlook also exist. Higher fuel prices are boosting near-term headline inflation. We will look through this volatility as appropriate. Our projection assumes firms have limited pass through of higher costs into generalised consumer prices, and that longer-term inflation expectations remain anchored at our target.

We will keep the OCR at an expansionary level for a considerable period to contribute to maximising sustainable employment, and maintaining low and stable inflation.

Australia PMI composite rose to 48.2, economy is not slowing sufficiently for RBA

Australia PMI Manufacturing fell from 50.2 to 49.8 in January, a 32-month low. PMI Services rose from 47.3 to 48.3. PMI Composite rose from 47.5 to 48.2.

Warren Hogan, Chief Economic Advisor at Judo Bank said:

“Following eight consecutive rate hikes in 2022, the RBA Board will be meeting for the first time on 7 February. The latest PMI readings may raise the concern that the economy is not slowing sufficiently to bring inflation back to target in a timely manner…

“Inflation pressures may abate somewhat but the risk for the RBA is that inflation remains stubbornly high well into 2023. This could maintain upward pressure on inflation expectations and wages growth. On this basis it seems premature for the RBA to pause the current tightening cycle….

“We expect the RBA to hike the cash rate by 25bp in each of February and March before an extended pause. Further rate hikes may be required later in 2023 if the economy and inflation prove more resilient than current consensus forecasts suggest.”

Full release here.