Canadian Foreign Affairs Minister Chrystia Freeland returned to the table with US Trade Representative Robert Lighthizer yesterday. She said the talks were constructive and they’re “making good progress”. She added that “we continue to get a deeper and deeper understanding of the concerns on both sides.” But Freeland declined to comment on how close the two sides were. The negotiation is still work in progress as Freeland’s team have sent the US “a number of issues to work on and they will report back to us in the morning (Thursday), and we will then continue our negotiations.”

Trump continued his bluff as he told reporters that if the talk doesn’t work out, “that’s going to be fine for the country, for our country.” However, “It won’t be fine for Canada”. He also reiterated that the US has a “very strong position” in the negotiation. At the same time, Canada and other countries “have been taking advantage of the United States for many years.”

Canadian Prime Minister Justin Trudeau reiterated his firm stance on the Chapter 19 dispute resolution mechanism, that was seen as a “red line” Trump. Trudeau emphasized that “We need to keep the Chapter 19 dispute resolution because that ensures that the rules are actually followed. And we know we have a president who doesn’t always follow the rules as they’re laid out.”

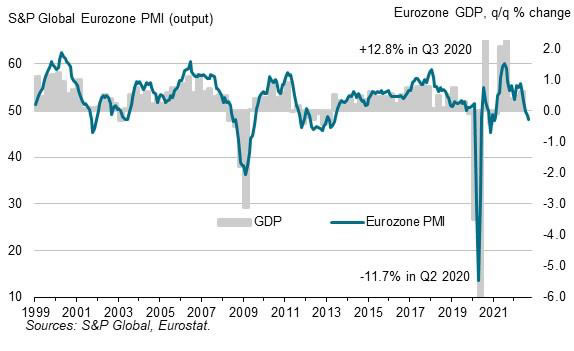

Eurozone PMI manufacturing down o 38-mth low, PMI services at 6-mth low

Eurozone’s economic outlook appears increasingly gloomy as latest PMI readings for manufacturing and services sectors disappoint, suggesting further contraction may lie ahead. Manufacturing PMI declined to 42.7 in July from 43.4, a 38-month low and below expectations of 43.5. Simultaneously, Services PMI dropped to a 6-month low of 51.1, short of the projected 51.5, and down from 52.0. Composite PMI, reflecting both sectors, sank to an 8-month low of 48.9, down from 49.9.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, expressed his concern, stating, “Manufacturing continues to be the Achilles heel of the eurozone. Producers have cut their output again at an accelerated pace in July, while the services sector’s activity is still expanding, though at a much slower rate than earlier in the year.” He further warned, “The eurozone economy will likely move further into contraction territory in the months ahead, as the services sector keeps losing steam.”

This less than encouraging data will surely unsettle ECB, as cost pressures in the private sector remain persistent, particularly in the substantial services sector. “The latest PMI reading is not going to please ECB officials…Thus, ECB president Christine Lagarde will certainly stick to her guns and hike interest rates by 25 bp at the next monetary meeting at the end of July,” de la Rubia explained.

Meanwhile, France’s manufacturing PMI slid to a 38-month low at 44.5, down from 46.0, while its services PMI fell to 47.4, a 29-month low, from 48.0. The composite PMI followed suit, dropping to a 32-month low at 46.6, dowm from 47.2.

Germany’s manufacturing PMI took a dive from 40.6 to 38.8, also a 38-month low. Services declined to a 5-month low at 52.0 from 54.1, and the composite PMI fell to an 8-month low of 48.3, down from 50.6.

Full Eurozone PMI release here.