UK Prime Minister Theresa May is set to meet opposition Labour leader Jeremy Corbyn later today to find the much needed common ground to get a Brexit deal through the parliament. But so far, it seems no one is optimistic about the meeting.

Ahead of that, May said there are areas she could agree on with Corbyn, including leaving EU with a deal, jobs and ending free movements. Minister for Wales and government whip Nigel Adams resigned on May’s decision and she is increasing the risk of the “calamity of a Corbyn government.” Brexit Minister Steven Barlcay said May is not handling a “blank check” to Corbyn and there is no precondition for the discussions with Labour.

Corbyn emphasized that anything agreed with May need to be put into law so that it is guaranteed for the parliament. pro-EU Labour lawmaker, Ben Bradshaw, warned that “it is clearly a trap designed to try to get May’s terrible deal through, which some people have fallen for, but Labour mustn’t.”

Scottish First Minister Nicola Sturgeon poured cold water and said the meeting would produce “an option that it won’t take too long for people to realize satisfies nobody, makes the country poorer and potentially could be unpicked by a new prime minister such as Boris Johnson.”

On the EU side, European Council President Donald Tusk said it was not certain how European leaders would view another request of delay from May. EU’s Economic Affairs and Tax Commissioner Pierre Moscovici said “If there is a no-deal scenario, new customs controls would have to be introduced… That does not mean we would systematically check every single… lorry… We would be controlling goods on the basis of risk analysis.”

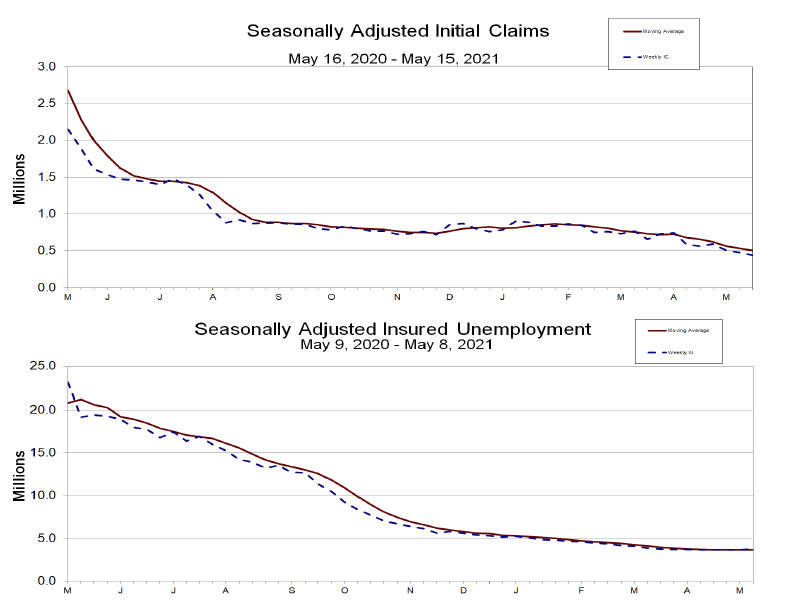

Fed Evans comfortable with inflation at 2.5% for averaging

Chicago Fed President Charles Evans said the new average inflation targeting was “consistent with the type of outcome-based forward guidance that I advocated and that the Committee used to speed the recovery after the Great Financial Crisis.”

“I expect that articulating outcome-based forward guidance for the rate path and asset purchases could be beneficial in the not-too-distant future” he added. He’d be “comfortable” with inflation going up to 2.5% “as long as we were trying to average off very low inflation rates”.

Evans also said, “even with steady progress in controlling the virus and additional fiscal support, I expect it will be some time before the economy recovers from the hit it took”. He expects the unemployment rate would still be somewhere in the range of 5% to 5.5% at the end of 2022.

Separately, Atlanta Fed President Raphael Bostic said, “as long as we see the trajectory moving in ways that suggest that we are not spiraling too far away from our target, I’m comfortable just letting the economy run and letting it play out”.